Ambaji123

please answer all the questions. thank you.

1:

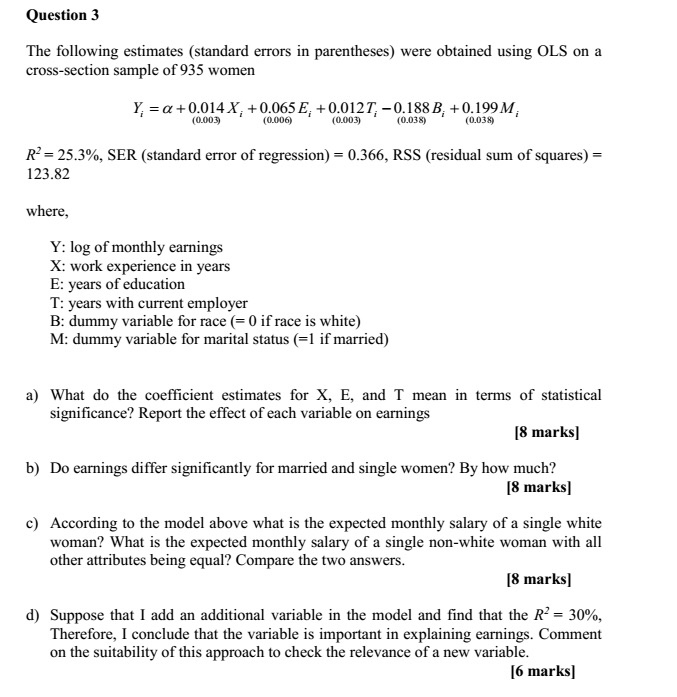

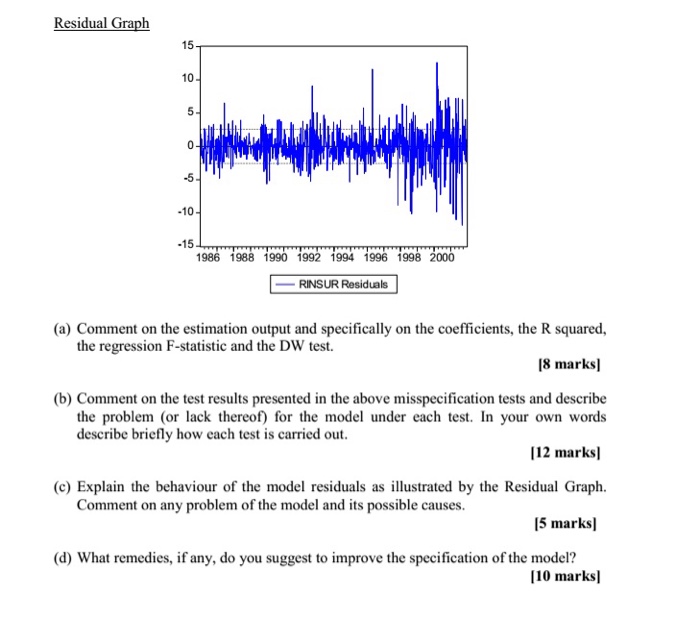

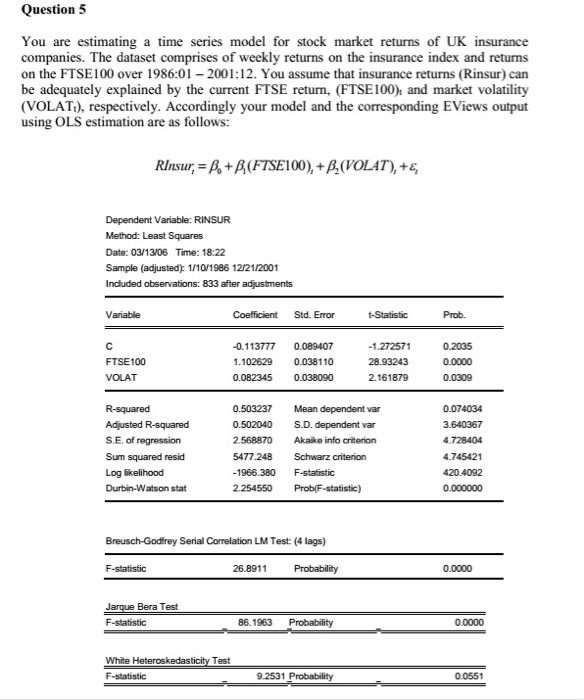

Measurements of pulmonary vascular resistance (PVR) in eight lambs were taken before and after infusion of the drug histamine. Of interest is whether histamine alters PVR. The PVR measurements are given below. Lamb H 2 3 4 5 6 7 8 Before 0.095 0.106 0.082 0.152 0.090 0.086 0.137 0.121 After 0.176 0.142 0.194 0.136 0.115 0.084 0.103 0.189 Source: P.V. Rao (1999), Statistical Research Methods in the Life Sciences, Duxbury. (a) Conduct the relevant test of hypothesis by following the five steps of hypothesis testing. [10 marks] (b) Verify the 95% confidence interval for the mean difference found in (a). Use t* = 2.365 and sa = 0.051. Show all calculations. (3 marks] (c) With reference to (a) and (b) write an informative conclusion. (3 marks]Question 3 The following estimates (standard errors in parentheses) were obtained using OLS on a cross-section sample of 935 women Y, = a+0.014 X, +0.065 E; + 0.0127, -0.188B; +0.199M; (0.003) (0.006) (0.003) (0.038) (0.038) R' = 25.3%, SER (standard error of regression) = 0.366, RSS (residual sum of squares) = 123.82 where, Y: log of monthly earnings X: work experience in years E: years of education T: years with current employer B: dummy variable for race (= 0 if race is white) M: dummy variable for marital status (=1 if married) a) What do the coefficient estimates for X, E, and T mean in terms of statistical significance? Report the effect of each variable on earnings [8 marks] b) Do earnings differ significantly for married and single women? By how much? [8 marks] c) According to the model above what is the expected monthly salary of a single white woman? What is the expected monthly salary of a single non-white woman with all other attributes being equal? Compare the two answers. [8 marks] d) Suppose that I add an additional variable in the model and find that the R' = 30%, Therefore, I conclude that the variable is important in explaining earnings. Comment on the suitability of this approach to check the relevance of a new variable. [6 marks]Residual Graph 15 10 5 O - -5. -10- -15. 1986 1988 1990 1992 1994 1996 1998 2000 - RINSUR Residuals (a) Comment on the estimation output and specifically on the coefficients, the R squared, the regression F-statistic and the DW test. [8 marks] (b) Comment on the test results presented in the above misspecification tests and describe the problem (or lack thereof) for the model under each test. In your own words describe briefly how each test is carried out. [12 marks] (c) Explain the behaviour of the model residuals as illustrated by the Residual Graph. Comment on any problem of the model and its possible causes. [5 marks] (d) What remedies, if any, do you suggest to improve the specification of the model? [10 marks]Question 5 You are estimating a time series model for stock market returns of UK insurance companies. The dataset comprises of weekly returns on the insurance index and returns on the FTSE100 over 1986:01 - 2001:12. You assume that insurance returns (Rinsur) can be adequately explained by the current FTSE return, (FTSE100), and market volatility (VOLAT:), respectively. Accordingly your model and the corresponding EViews output using OLS estimation are as follows: RInsur, = B. + B,(FTSE100), + B.(VOLAT), +6, Dependent Variable: RINSUR Method: Least Squares Date: 03/13/06 Time: 18:22 Sample (adjusted): 1/10/1986 12/21/2001 Included observations: 833 after adjustments Variable Coefficient Std. Error 1-Statistic Prob C -0.113777 0.089407 -1.272571 0.2035 FTSE100 1.102629 0.038110 28.93243 010000 VOLAT 0.082345 0.038090 2.161879 0.0309 R-squared 0.503237 Mean dependent var 0.074034 Adjusted R-squared 0.502040 S.D. dependent var 3.640367 S.E. of regression 2.568870 Akaike info criterion 4.728404 Sum squared resid 5477.248 Schwarz criterion 4.745421 Log likelihood -1966.380 F-statistic 420.4092 Durbin-Watson stat 2.254550 Prob(F-statistic] 0.000000 Breusch-Godfrey Serial Correlation LM Test: (4 lags) F-statistic 26.8911 Probability 0.0000 Jarque Bera Test F-clatistic 86.1963 Probability 0.0000 White Heteroskedasticity Test F-statistic 9.2531 Probability 010551