Answered step by step

Verified Expert Solution

Question

1 Approved Answer

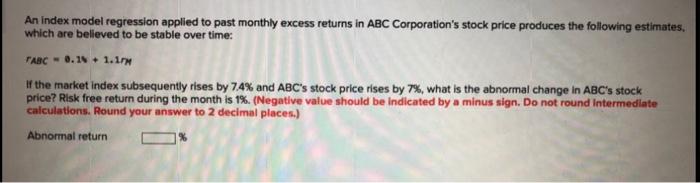

An index model regression applied to past monthly excess returns in ABC Corporation's stock price produces the following estimates, which are believed to be stable

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The ImpactAssets Handbook For Investors

Authors: Jed Emerson

1st Edition

1783087293, 978-1783087297