Answered step by step

Verified Expert Solution

Question

1 Approved Answer

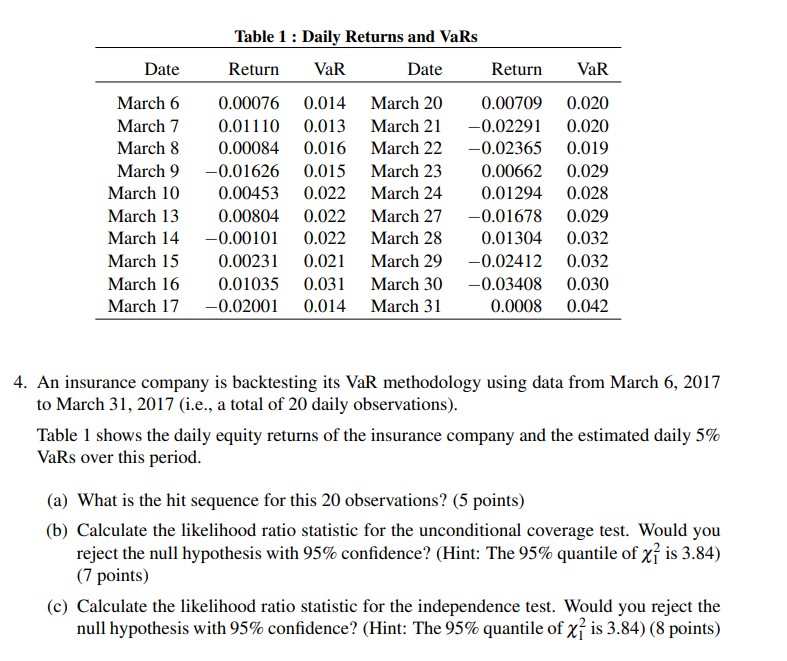

An insurance company is backtesting its VaR methodology using data from March 6, 2017 to March 31, 2017 (i.e., a total of 20 daily observations).

An insurance company is backtesting its VaR methodology using data from March 6, 2017 to March 31, 2017 (i.e., a total of 20 daily observations). Table 1 shows the daily equity returns of the insurance company and the estimated daily 5% VaRs over this period. (a) What is the hit sequence for this 20 observations? (5 points) (b) Calculate the likelihood ratio statistic for the unconditional coverage test. Would you reject the null hypothesis with 95% confidence? (Hint: The 95% quantile of 12 is 3.84 ) (7 points) (c) Calculate the likelihood ratio statistic for the independence test. Would you reject the null hypothesis with 95% confidence? (Hint: The 95% quantile of 12 is 3.84 ) (8 points)

An insurance company is backtesting its VaR methodology using data from March 6, 2017 to March 31, 2017 (i.e., a total of 20 daily observations). Table 1 shows the daily equity returns of the insurance company and the estimated daily 5% VaRs over this period. (a) What is the hit sequence for this 20 observations? (5 points) (b) Calculate the likelihood ratio statistic for the unconditional coverage test. Would you reject the null hypothesis with 95% confidence? (Hint: The 95% quantile of 12 is 3.84 ) (7 points) (c) Calculate the likelihood ratio statistic for the independence test. Would you reject the null hypothesis with 95% confidence? (Hint: The 95% quantile of 12 is 3.84 ) (8 points) Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Auditing Quality Management Systems Keeping Your Quality Management System Relevant

Authors: Herne European Consultancy, Ray Tricker

1st Edition

0992758521, 978-0992758523