Answered step by step

Verified Expert Solution

Question

1 Approved Answer

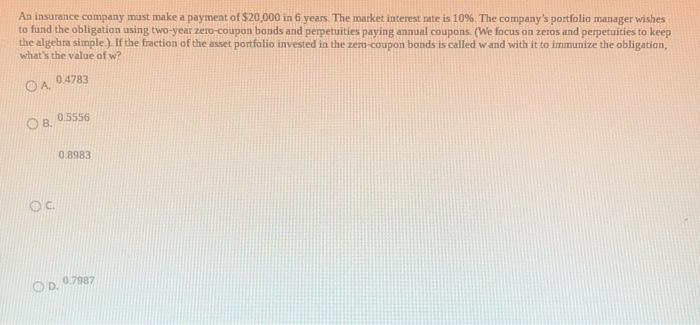

An insurance company must make a payment of $20,000 in 6 years. The market interest rate is 10%. The company's portfolio manager wishes to fund

An insurance company must make a payment of $20,000 in 6 years. The market interest rate is 10%. The company's portfolio manager wishes to fund the obligation using two-year zero-coupon bonds and perpetuities paying annual coupons (We focus on zeros and perpetuities to keep the algebra simple) If the fraction of the asset portfolio invested in the zeru-coupon bonds is called wand with it to immunize the obligation, what's the value of w? 0.4783 OA OB 0.5556 0.8983 OC OD.7987

An insurance company must make a payment of $20,000 in 6 years. The market interest rate is 10%. The company's portfolio manager wishes to fund the obligation using two-year zero-coupon bonds and perpetuities paying annual coupons (We focus on zeros and perpetuities to keep the algebra simple) If the fraction of the asset portfolio invested in the zeru-coupon bonds is called wand with it to immunize the obligation, what's the value of w? 0.4783 OA OB 0.5556 0.8983 OC OD.7987

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Your Financial Future How To Take Control Of Your Financial Future

Authors: Deloris Lutke

1st Edition

979-8388730831