Answered step by step

Verified Expert Solution

Question

1 Approved Answer

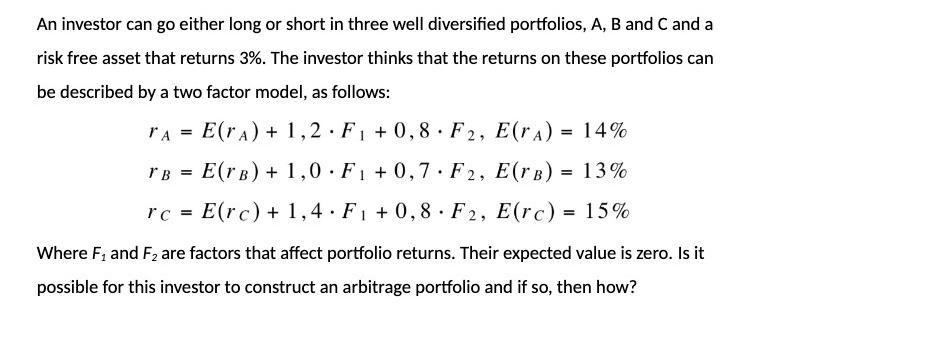

An investor can go either long or short in three well diversified portfolios, A, B and C and a risk free asset that returns

An investor can go either long or short in three well diversified portfolios, A, B and C and a risk free asset that returns 3%. The investor thinks that the returns on these portfolios can be described by a two factor model, as follows: TA = E(TA) + 1,2 F +0,8 F2, E(A) = 14% E(TB) + 1,0 F1+0,7 F2, E(TB) = 13% rc = E(rc) + 1,4 F +0,8 F2, E(rc) = 15% = . . . Where F, and F are factors that affect portfolio returns. Their expected value is zero. Is it possible for this investor to construct an arbitrage portfolio and if so, then how?

Step by Step Solution

★★★★★

3.35 Rating (142 Votes )

There are 3 Steps involved in it

Step: 1

To determine if the investor can construct an arbitrage portfolio we need to check for the existence of a portfolio that has a guaranteed positive ret...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Statistics For Business Decision Making And Analysis

Authors: Robert Stine, Dean Foster

2nd Edition

978-0321836519, 321836510, 978-0321890269