Answered step by step

Verified Expert Solution

Question

1 Approved Answer

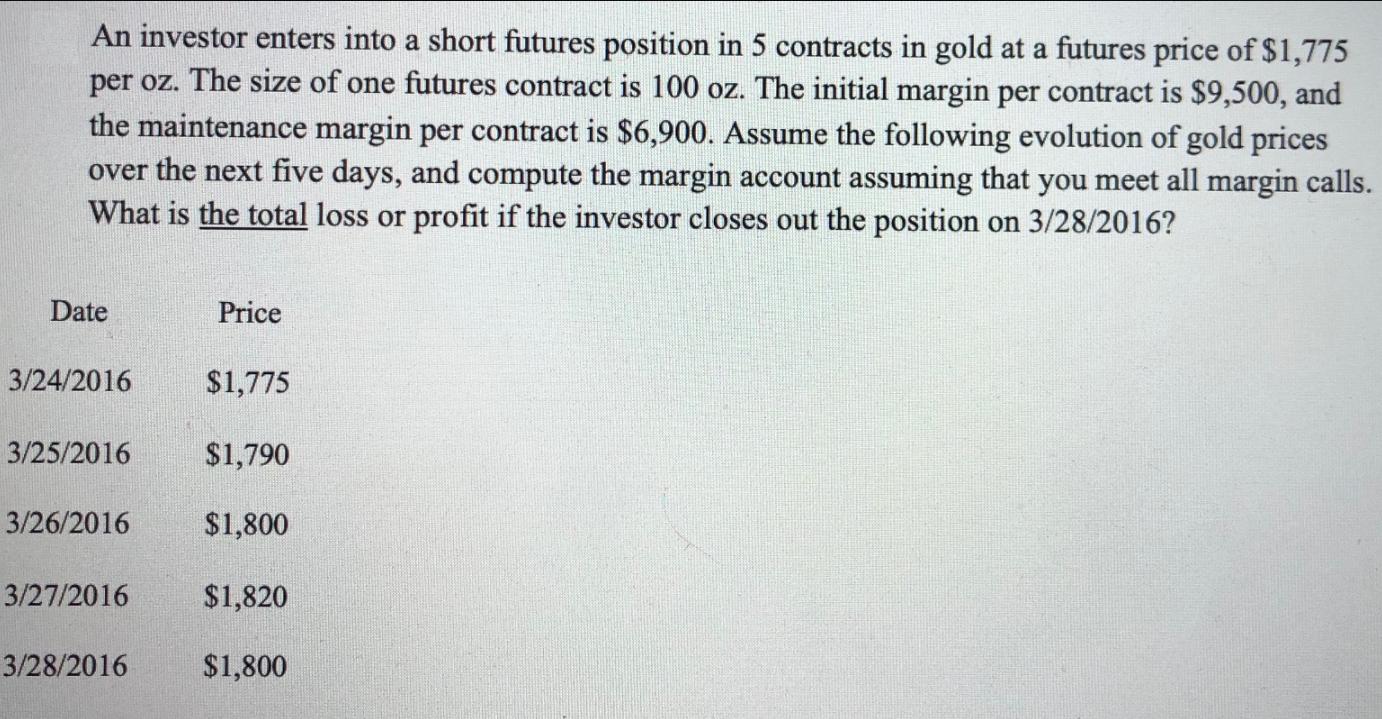

An investor enters into a short futures position in 5 contracts in gold at a futures price of $1,775 per oz. The size of

An investor enters into a short futures position in 5 contracts in gold at a futures price of $1,775 per oz. The size of one futures contract is 100 oz. The initial margin per contract is $9,500, and the maintenance margin per contract is $6,900. Assume the following evolution of gold prices over the next five days, and compute the margin account assuming that you meet all margin calls. What is the total loss or profit if the investor closes out the position on 3/28/2016? Date Price 3/24/2016 $1,775 3/25/2016 $1,790 3/26/2016 $1,800 3/27/2016 $1,820 3/28/2016 $1,800

Step by Step Solution

★★★★★

3.32 Rating (149 Votes )

There are 3 Steps involved in it

Step: 1

Answer Short position 5 gold contract futures Future price 1775 pe...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Risk Management and Financial Institutions

Authors: Hull John

4th edition

1118955943, 978-1118955949