Question

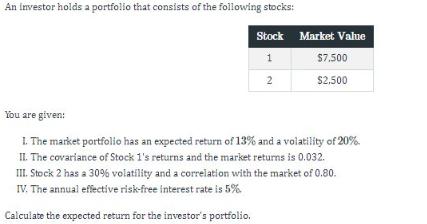

An investor holds a portfolio that consists of the following stocks: Stock 1 2 Market Value $7,500 $2,500 You are given: 1. The market

An investor holds a portfolio that consists of the following stocks: Stock 1 2 Market Value $7,500 $2,500 You are given: 1. The market portfolio has an expected return of 13% and a volatility of 20% II. The covariance of Stock 1's returns and the market returns is 0.032. III. Stock 2 has a 30% volatility and a correlation with the market of 0.80. IV. The annual effective risk-free interest rate is 5% Calculate the expected return for the investor's portfolio.

Step by Step Solution

3.37 Rating (153 Votes )

There are 3 Steps involved in it

Step: 1

To work out the normal return for the financial backers portfolio we really want to involve the loads of each stock in the portfolio and their compari...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Intermediate Financial Management

Authors: Eugene F. Brigham, Phillip R. Daves

11th edition

978-1111530266