Answered step by step

Verified Expert Solution

Question

1 Approved Answer

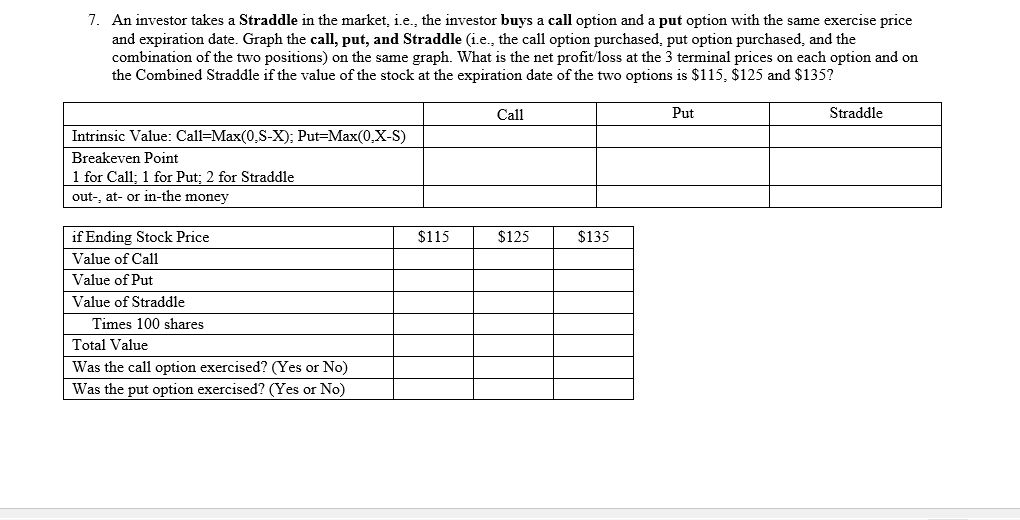

An investor takes a Straddle in the market, i . e . , the investor buys a call option and a put option with the

An investor takes a Straddle in the market, ie the investor buys a call option and a put option with the same exercise price

and expiration date. Graph the call, put, and Straddle ie the call option purchased, put option purchased, and the

combination of the two positions on the same graph. What is the net profitloss at the terminal prices on each option and on

the Combined Straddle if the value of the stock at the expiration date of the two options is $$ and $

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Currency Strategy The Practitioners Guide To Currency Investing Hedging And Forecasting

Authors: Callum Henderson

2nd Edition

0470027592, 978-0470027592