Answered step by step

Verified Expert Solution

Question

1 Approved Answer

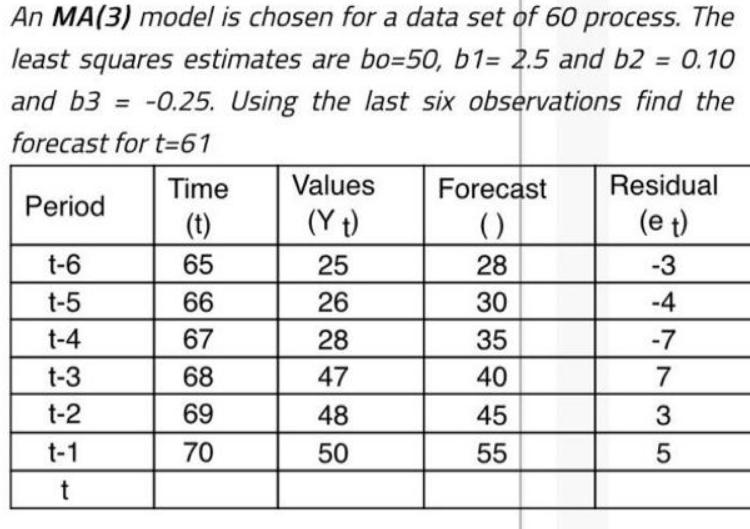

An MA(3) model is chosen for a data set of 60 process. The least squares estimates are bo=50, b1= 2.5 and b2 = 0.10

An MA(3) model is chosen for a data set of 60 process. The least squares estimates are bo=50, b1= 2.5 and b2 = 0.10 %3D and b3 = -0.25. Using the last six observations find the %3D forecast for t=61 Time Values Forecast Residual Period (t) (Y t) () (e t) t-6 65 25 28 -3 t-5 66 26 30 -4 t-4 67 28 35 -7 t-3 68 47 40 7 t-2 69 48 45 3 t-1 70 50 55

Step by Step Solution

★★★★★

3.50 Rating (153 Votes )

There are 3 Steps involved in it

Step: 1

CO 2112 20122 01001 is a bosu for c dim c3 now dimc t...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Cost Accounting A Managerial Emphasis

Authors: Charles T. Horngren, Srikant M.Dater, George Foster, Madhav

13th Edition

8120335643, 136126634, 978-0136126638