Question: analysis for the following case study Case 2-2: Mowerson Division The Mowerson Division of Brown Instruments manufactures testing equipment for the automobile industry. Mowerson's equipment

analysis for the following case study

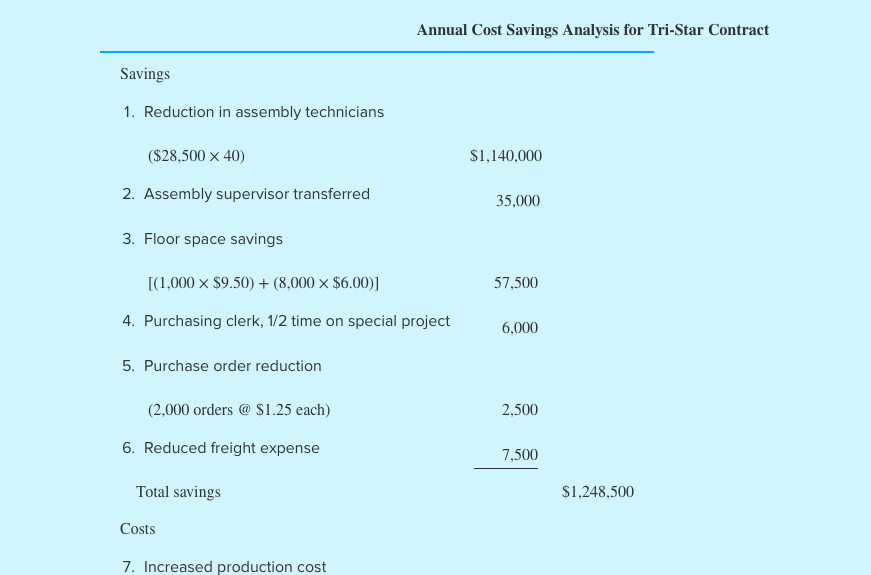

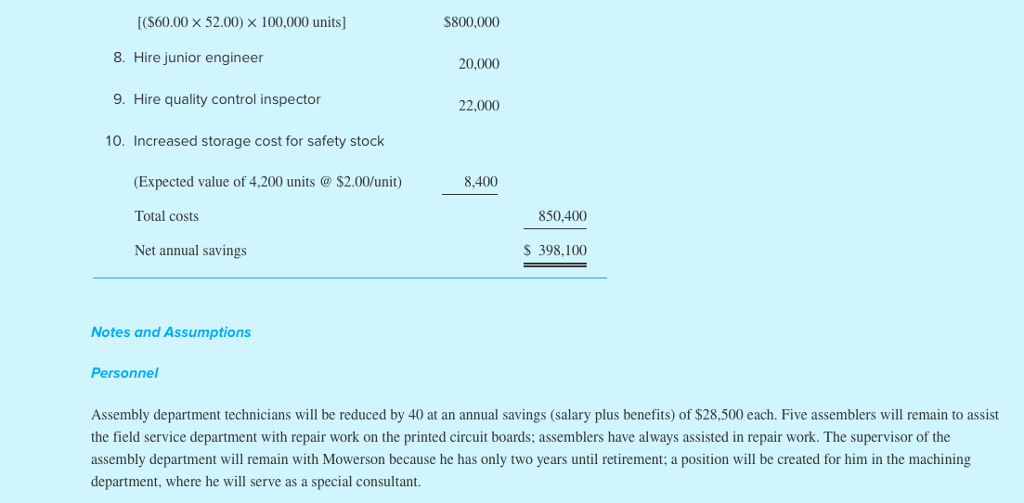

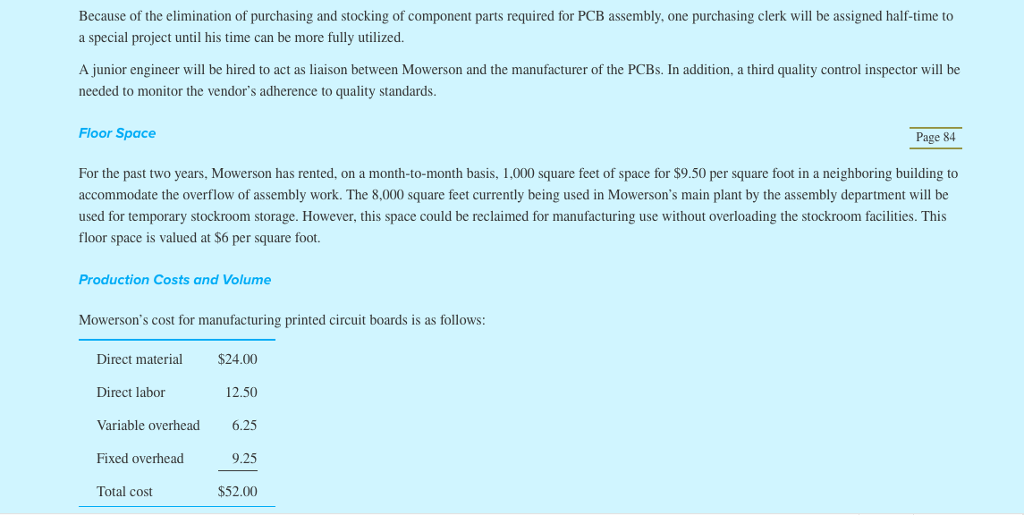

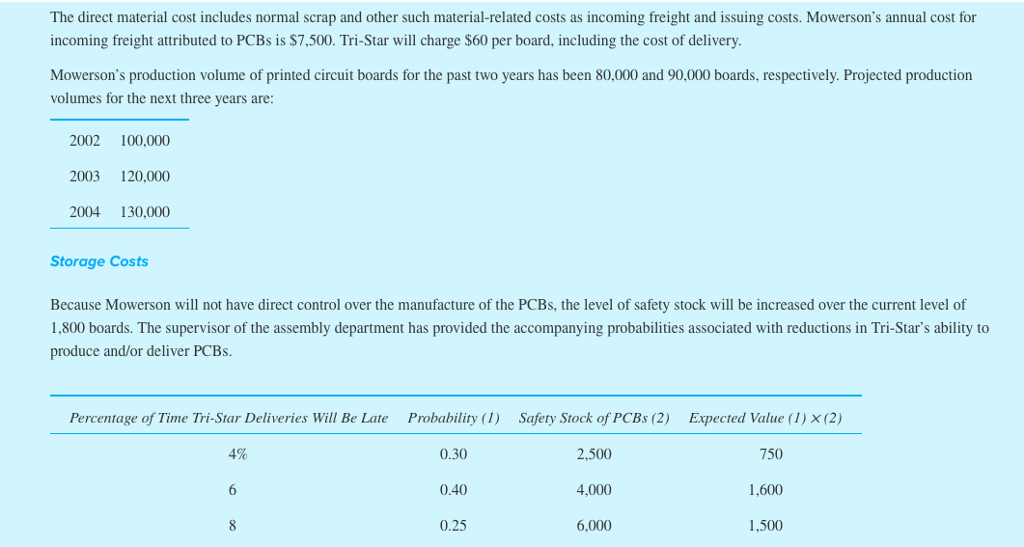

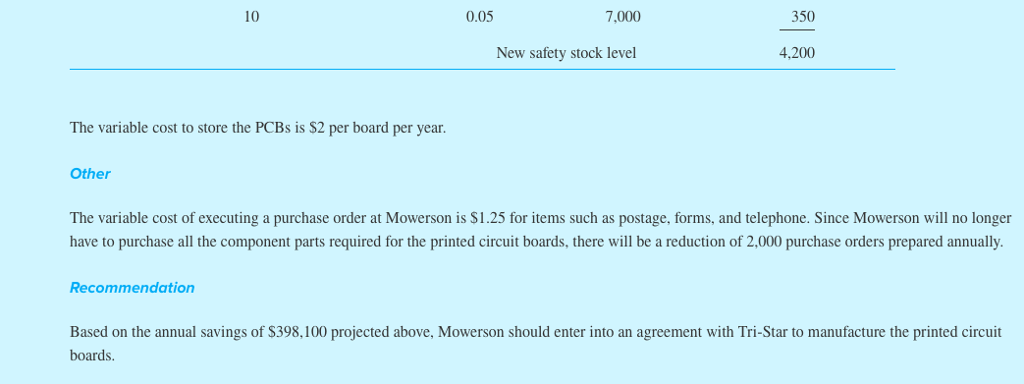

Case 2-2: Mowerson Division The Mowerson Division of Brown Instruments manufactures testing equipment for the automobile industry. Mowerson's equipment is installed in several places along an automobile assembly line for component testing and is also used for recording and measurement purposes during track and road tests. Mowerson's sales have grown steadily, and revenue will exceed $200 million for the first time in 2001 Mowerson designs and manufactures its own printed circuit boards (PCBs) for use in the test equipment. The PCBs are manually assembled in the Assembly Department, which employs 45 technicians. Because of a lack of plant capacity and a shortage of skilled labor, Mowerson is considering having the printed circuit boards manufactured by Tri-Star, a specialist in this field Quality control restrictions and vendor requirements dictate that all PCBs be either manufactured by Mowerson or contracted to an outside vendor. The per-board cost of outside manufacture is higher than the in-house cost; however, management thinks that savings could also be realized from this change Jim Wright, a recently hired cost analyst, has been asked to prepare a financial analysis of the outside manufacturing prop analysis, along with his recommendation. His financial analysis appears next, and his notes and assumptions follow the analysis osal. Wright's report includes the assumptions he used in his Required a. Discuss whether Jim Wright should have analyzed only the costs and savings that Mowerson will realize in 2002. b. For each of the 10 items listed in Wright's financial analysis, indicate whether (i) The item is appropriate or inappropriate for inclusion in the report. If the item is inappropriate, explain why it should not be included in the report. (ii) The amount is correct or incorrect. If the amount is incorrect, state what the correct amount is. c. What additional information about Tri-Star would be helpful to Mowerson in evaluating its manufacturing decision? Annual Cost Savings Analysis for Tri-Star Contract Savings 1. Reduction in assembly technicians ($28,500 x 40) 2. Assembly supervisor transferred 3. Floor space savings $1,140,000 35,000 (1,000 x S9.50) (8,000 x $6.00)] 57,500 4. Purchasing clerk, 1/2 time on special project 6,000 5. Purchase order reduction (2.000 orders@ $1.25 each) 2,500 6. Reduced freight expense 7,500 Total savings Costs 7. Increased production cost $1,248,500 (S60.00 x 52.00) x 100,000 units] 8. Hire junior engineer 9. Hire quality control inspector $800,000 20,000 22,000 10. Increased storage cost for safety stock (Expected value of 4,200 units$2.00/unit) Total costs Net annual savings 8,400 850.400 S 398,100 Notes and Assumptions Personnel Assembly department technicians will be reduced by 40 at an annual savings (salary plus benefits) of $28,500 each. Five assemblers will remain to assist the field service department with repair work on the printed circuit boards; assemblers have al ways assisted in repair work. The supervisor of the assembly department will remain with Mowerson because he has only two years until retirement; a position will be created for him in the machining department, where he will serve as a special consultant. Because of the elimination of purchasing and stocking of component parts required for PCB assembly, one purchasing clerk will be assigned half-time to a special project until his time can be more fully utilized. A junior engineer will be hired to act as liaison between Mowerson and the manufacturer of the PCBs. In addition, a third quality control inspector will be needed to monitor the vendor's adherence to quality standards. Floor Space Page 84 For the past two years, Mowerson has rented, on a month-to-month basis, 1,000 square feet of space for $9.50 per square foot in a neighboring building to accommodate the overflow of assembly work. The 8,000 square feet currently being used in Mowerson's main plant by the assembly department will be used for temporary stockroom storage. However, this space could be reclaimed for manufacturing use without overloading the stockroom facilities. This floor space is valued at S6 per square foot. Production Costs and Volume Mowerson's cost for manufacturing printed circuit boards is as follows: Direct material Direct labor Variable overhead Fixed overhead Total cost $24.00 12.50 6.25 9.25 $52.00 The direct material cost includes normal scrap and other such material-related costs as incoming freight and issuing costs. Mowerson's annual cost for incoming freight attributed to PCBs is S7,500. Tri-Star will charge $60 per board, including the cost of delivery. Mowerson's production volume of printed circuit boards for the past two years has been 80,000 and 90,000 boards, respectively. Projected production volumes for the next three years are: 2002 100,000 2003 120,000 2004 130,000 Storage Costs Because Mowerson will not have direct control over the manufacture of the PCBs, the level of safety stock will be increased over the current level of 1,800 boards. The supervisor of the assembly department has provided the accompanying probabilities associated with reductions in Tri-Star's ability to produce and/or deliver PCBs Percentage of Time Tri-Star Deliveries Will Be Late Probability (1) Safety Stock of PCBs (2) Expected Value () x (2) 0.30 0.40 0.25 2,500 4,000 6,000 750 1,600 1,500 4% 10 0.05 7,000 350 New safety stock level 4,200 The variable cost to store the PCBs is $2 per board per year. Other The variable cost of executing a purchase order at Mowerson is $1.25 for items such as postage, forms, and telephone. Since Mowerson will no longer have to purchase all the component parts required for the printed circuit boards, there will be a reduction of 2,000 purchase orders prepared annually. Recommendation Based on the annual savings of S398,100 projected above, Mowerson should enter into an agreement with Tri-Star to manufacture the printed circuit boards. Case 2-2: Mowerson Division The Mowerson Division of Brown Instruments manufactures testing equipment for the automobile industry. Mowerson's equipment is installed in several places along an automobile assembly line for component testing and is also used for recording and measurement purposes during track and road tests. Mowerson's sales have grown steadily, and revenue will exceed $200 million for the first time in 2001 Mowerson designs and manufactures its own printed circuit boards (PCBs) for use in the test equipment. The PCBs are manually assembled in the Assembly Department, which employs 45 technicians. Because of a lack of plant capacity and a shortage of skilled labor, Mowerson is considering having the printed circuit boards manufactured by Tri-Star, a specialist in this field Quality control restrictions and vendor requirements dictate that all PCBs be either manufactured by Mowerson or contracted to an outside vendor. The per-board cost of outside manufacture is higher than the in-house cost; however, management thinks that savings could also be realized from this change Jim Wright, a recently hired cost analyst, has been asked to prepare a financial analysis of the outside manufacturing prop analysis, along with his recommendation. His financial analysis appears next, and his notes and assumptions follow the analysis osal. Wright's report includes the assumptions he used in his Required a. Discuss whether Jim Wright should have analyzed only the costs and savings that Mowerson will realize in 2002. b. For each of the 10 items listed in Wright's financial analysis, indicate whether (i) The item is appropriate or inappropriate for inclusion in the report. If the item is inappropriate, explain why it should not be included in the report. (ii) The amount is correct or incorrect. If the amount is incorrect, state what the correct amount is. c. What additional information about Tri-Star would be helpful to Mowerson in evaluating its manufacturing decision? Annual Cost Savings Analysis for Tri-Star Contract Savings 1. Reduction in assembly technicians ($28,500 x 40) 2. Assembly supervisor transferred 3. Floor space savings $1,140,000 35,000 (1,000 x S9.50) (8,000 x $6.00)] 57,500 4. Purchasing clerk, 1/2 time on special project 6,000 5. Purchase order reduction (2.000 orders@ $1.25 each) 2,500 6. Reduced freight expense 7,500 Total savings Costs 7. Increased production cost $1,248,500 (S60.00 x 52.00) x 100,000 units] 8. Hire junior engineer 9. Hire quality control inspector $800,000 20,000 22,000 10. Increased storage cost for safety stock (Expected value of 4,200 units$2.00/unit) Total costs Net annual savings 8,400 850.400 S 398,100 Notes and Assumptions Personnel Assembly department technicians will be reduced by 40 at an annual savings (salary plus benefits) of $28,500 each. Five assemblers will remain to assist the field service department with repair work on the printed circuit boards; assemblers have al ways assisted in repair work. The supervisor of the assembly department will remain with Mowerson because he has only two years until retirement; a position will be created for him in the machining department, where he will serve as a special consultant. Because of the elimination of purchasing and stocking of component parts required for PCB assembly, one purchasing clerk will be assigned half-time to a special project until his time can be more fully utilized. A junior engineer will be hired to act as liaison between Mowerson and the manufacturer of the PCBs. In addition, a third quality control inspector will be needed to monitor the vendor's adherence to quality standards. Floor Space Page 84 For the past two years, Mowerson has rented, on a month-to-month basis, 1,000 square feet of space for $9.50 per square foot in a neighboring building to accommodate the overflow of assembly work. The 8,000 square feet currently being used in Mowerson's main plant by the assembly department will be used for temporary stockroom storage. However, this space could be reclaimed for manufacturing use without overloading the stockroom facilities. This floor space is valued at S6 per square foot. Production Costs and Volume Mowerson's cost for manufacturing printed circuit boards is as follows: Direct material Direct labor Variable overhead Fixed overhead Total cost $24.00 12.50 6.25 9.25 $52.00 The direct material cost includes normal scrap and other such material-related costs as incoming freight and issuing costs. Mowerson's annual cost for incoming freight attributed to PCBs is S7,500. Tri-Star will charge $60 per board, including the cost of delivery. Mowerson's production volume of printed circuit boards for the past two years has been 80,000 and 90,000 boards, respectively. Projected production volumes for the next three years are: 2002 100,000 2003 120,000 2004 130,000 Storage Costs Because Mowerson will not have direct control over the manufacture of the PCBs, the level of safety stock will be increased over the current level of 1,800 boards. The supervisor of the assembly department has provided the accompanying probabilities associated with reductions in Tri-Star's ability to produce and/or deliver PCBs Percentage of Time Tri-Star Deliveries Will Be Late Probability (1) Safety Stock of PCBs (2) Expected Value () x (2) 0.30 0.40 0.25 2,500 4,000 6,000 750 1,600 1,500 4% 10 0.05 7,000 350 New safety stock level 4,200 The variable cost to store the PCBs is $2 per board per year. Other The variable cost of executing a purchase order at Mowerson is $1.25 for items such as postage, forms, and telephone. Since Mowerson will no longer have to purchase all the component parts required for the printed circuit boards, there will be a reduction of 2,000 purchase orders prepared annually. Recommendation Based on the annual savings of S398,100 projected above, Mowerson should enter into an agreement with Tri-Star to manufacture the printed circuit boards

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts