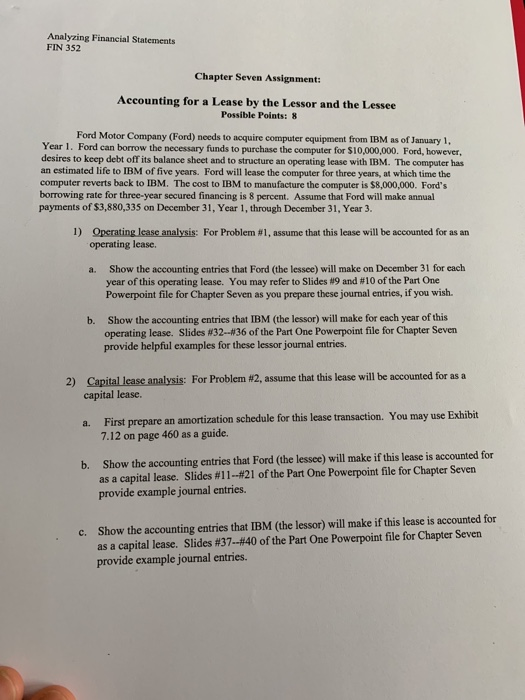

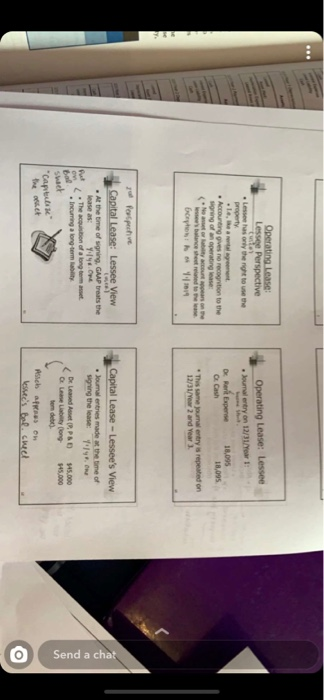

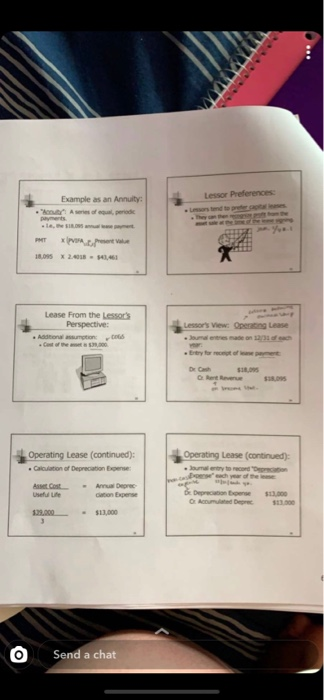

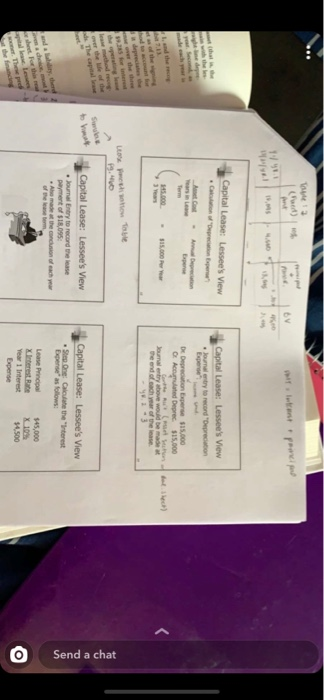

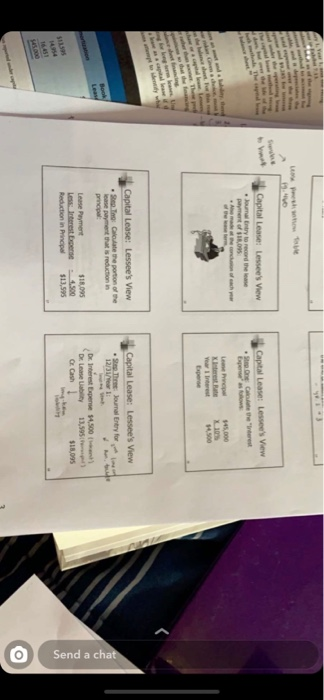

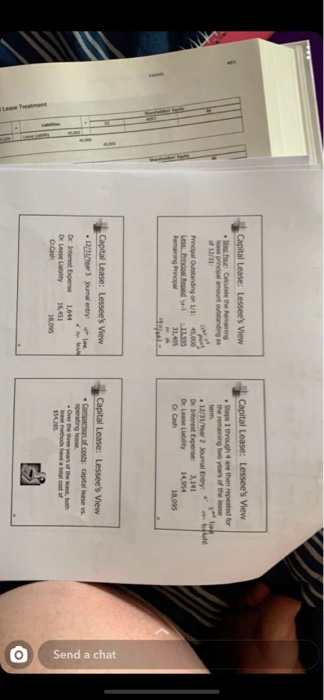

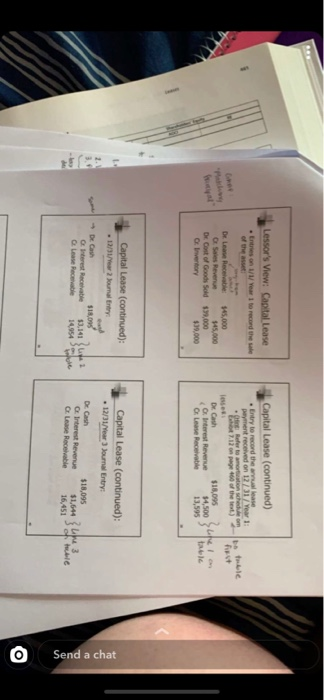

Analyzing Financial Statements FIN 352 Chapter Seven Assignment: Accounting for a Lease by the Lessor and the Lessee Possible Points: 8 Ford Motor Company (Ford) needs to acquire computer equipment from IBM as of January 1, Year 1. Ford can borrow the necessary funds to purchase the computer for $10,000,000. Ford, however, desires to keep debt off its balance sheet and to structure an operating lease with IBM. The computer has an estimated life to IBM of five years. Ford will lease the computer for three years, at which time the computer reverts back to IBM. The cost to IBM to manufacture the computer is $8,000,000. Ford's borrowing rate for three-year secured financing is 8 percent. Assume that Ford will make annual payments of $3,880,335 on December 31, Year 1, through December 31, Year 3. 1) Operating Icase analysis: For Problem #1, assume that this lease will be accounted for as an operating lease. a. Show the accounting entries that Ford (the lessee) will make on December 31 for each year of this operating lease. You may refer to Slides #9 and #10 of the Part One Powerpoint file for Chapter Seven as you prepare these journal entries, if you wish. b. Show the accounting entries that IBM (the lessor) will make for each year of this operating lease. Slides #32--#36 of the Part One Powerpoint file for Chapter Seven provide helpful examples for these lessor journal entries. 2) Capital lease analysis: For Problem #2, assume that this lease will be accounted for as a capital lease. a First prepare an amortization schedule for this lease transaction. You may use Exhibit 7.12 on page 460 as a guide. b. Show the accounting entries that Ford (the lessce) will make if this lease is accounted for as a capital lease. Slides #11 --#21 of the Part One Powerpoint file for Chapter Seven provide example journal entries. c. Show the accounting entries that IBM (the lessor) will make if this lease is accounted for as a capital lease. Slides #37--#40 of the Part One Powerpoint file for Chapter Seven provide example journal entries. Operating Lease: Lessee Perspective Lesses only the news the property Operating Lease: Lessee Journal entry on 12/31/Year 1: De Rere Expense 18,095 O Cash 18.095 Accounting oves no recognition to the gring of an operating ease Noorso This same journal entry 12/31/Year and Year repeated on Echo T jul for peche Capital Lease: Lessee View - At the time of signing, GAAP treats the lease as Y19. The action of a long term incurring a long term Capital Lease - Lessee's View Journal entries made the time of signing the lease 1 Send a chat "Capi Deleased A S D $45.000 Le long 945,000 som de Psich a n lessee's Bel. chel O Lessor Preferences Example as an Annuity: Aspedie . -le. ONS 18.095 X 2018 - 10.461 Lease From the lessor's Perspective: - Additional assumption: 0065 Lessor's View. Operating Lease our entrerade on 1231 Entry for no t De Operating Lease continued): . Calculation of Depreciation E nse: Operating Lease (continued): to con Bosch Bc Depron se $13.000 Andere A cest Uute - Annual Degree 309.000 - $13,000 O Send a chat ( d) 1901 Capital Lease Lessee's View Capital Lease: Lessee's View une entry to record Deprecation De Depreciation Experise $15,000 O Acumulated Degre 150.000 145.000 Jumaly above would be adat the end of each of these - Y3 9. Capital Lease: Lessee's View Journal Entry to record the case payment of STR095 A made the conclusion of the of the base om Capital Lease: Lessee's View Step One Calculate the interest Send a chat Myth $45,000 Lease Pricial Interest Rate Year 1 Interest Expense $4,500 O Capital Lease: Lessee's View - Journal Entry to record these payment of 1095 Capital Lease: Lessee's View De C herest Expenses Le Papel med Exper mm www. Capital Lease: Lessee's View Se To Catere portion of the case payment that is reduction in Capital Lease: Lessee's View Se The Journal Entry for 1273 4.500 F 13,595 t De Interest Expense De laseb O Cash Lease Payment Les Interest pense Reduction in Principal 18.095 4.500 $13,595 Send a chat 18.095 Capital Lease: Lessee's View Sterou the Remaring se propel amount outstanding as Capital Lease: Lessee's View Steps tough are the repeated for the remaining two years of the lease 45.000 Principal Outstanding on 1/1 Les Mild Remarang po 12/31/Year 2 journal Entry De Interest Expense 3,141 De Lease Liability 14.954 O Cash 18095 31.05 Capital Lease: Lessee's View - 12/31/Year 3 journal erty: line Capital Lease: Lessee's View Comparison costs capitale vs operating lease Over the three years of the bo Send a chat De Interest Expense De lesse C.Cash 164 16,451 18.09 O Lessor's View: Capital Lease Entries on // Year I to record the sale Capital Lease (continued) Entry to record the lease payment received on 12/01/Year: 12e the tale Dr. Lease Recei O Ses Revenue De Cost of Goods Sold 45,000 45.000 379.000 $39.000 Dr Cash erest Revenue Of Lease Receivable $18,095 4,500 11,595 table Capital Lease (continued): - 12/31/ar 2 journal Capital Lease (continued): 12/31/Year 3 Journal Entry: Orerest Receable Lease Recebe $18,095 33,141 S 14.954 elle De Cash Interest Revenue Glease Receivable $18,095 $1,644 16,451 16,451 Send a chat 3 orale O Analyzing Financial Statements FIN 352 Chapter Seven Assignment: Accounting for a Lease by the Lessor and the Lessee Possible Points: 8 Ford Motor Company (Ford) needs to acquire computer equipment from IBM as of January 1, Year 1. Ford can borrow the necessary funds to purchase the computer for $10,000,000. Ford, however, desires to keep debt off its balance sheet and to structure an operating lease with IBM. The computer has an estimated life to IBM of five years. Ford will lease the computer for three years, at which time the computer reverts back to IBM. The cost to IBM to manufacture the computer is $8,000,000. Ford's borrowing rate for three-year secured financing is 8 percent. Assume that Ford will make annual payments of $3,880,335 on December 31, Year 1, through December 31, Year 3. 1) Operating Icase analysis: For Problem #1, assume that this lease will be accounted for as an operating lease. a. Show the accounting entries that Ford (the lessee) will make on December 31 for each year of this operating lease. You may refer to Slides #9 and #10 of the Part One Powerpoint file for Chapter Seven as you prepare these journal entries, if you wish. b. Show the accounting entries that IBM (the lessor) will make for each year of this operating lease. Slides #32--#36 of the Part One Powerpoint file for Chapter Seven provide helpful examples for these lessor journal entries. 2) Capital lease analysis: For Problem #2, assume that this lease will be accounted for as a capital lease. a First prepare an amortization schedule for this lease transaction. You may use Exhibit 7.12 on page 460 as a guide. b. Show the accounting entries that Ford (the lessce) will make if this lease is accounted for as a capital lease. Slides #11 --#21 of the Part One Powerpoint file for Chapter Seven provide example journal entries. c. Show the accounting entries that IBM (the lessor) will make if this lease is accounted for as a capital lease. Slides #37--#40 of the Part One Powerpoint file for Chapter Seven provide example journal entries. Operating Lease: Lessee Perspective Lesses only the news the property Operating Lease: Lessee Journal entry on 12/31/Year 1: De Rere Expense 18,095 O Cash 18.095 Accounting oves no recognition to the gring of an operating ease Noorso This same journal entry 12/31/Year and Year repeated on Echo T jul for peche Capital Lease: Lessee View - At the time of signing, GAAP treats the lease as Y19. The action of a long term incurring a long term Capital Lease - Lessee's View Journal entries made the time of signing the lease 1 Send a chat "Capi Deleased A S D $45.000 Le long 945,000 som de Psich a n lessee's Bel. chel O Lessor Preferences Example as an Annuity: Aspedie . -le. ONS 18.095 X 2018 - 10.461 Lease From the lessor's Perspective: - Additional assumption: 0065 Lessor's View. Operating Lease our entrerade on 1231 Entry for no t De Operating Lease continued): . Calculation of Depreciation E nse: Operating Lease (continued): to con Bosch Bc Depron se $13.000 Andere A cest Uute - Annual Degree 309.000 - $13,000 O Send a chat ( d) 1901 Capital Lease Lessee's View Capital Lease: Lessee's View une entry to record Deprecation De Depreciation Experise $15,000 O Acumulated Degre 150.000 145.000 Jumaly above would be adat the end of each of these - Y3 9. Capital Lease: Lessee's View Journal Entry to record the case payment of STR095 A made the conclusion of the of the base om Capital Lease: Lessee's View Step One Calculate the interest Send a chat Myth $45,000 Lease Pricial Interest Rate Year 1 Interest Expense $4,500 O Capital Lease: Lessee's View - Journal Entry to record these payment of 1095 Capital Lease: Lessee's View De C herest Expenses Le Papel med Exper mm www. Capital Lease: Lessee's View Se To Catere portion of the case payment that is reduction in Capital Lease: Lessee's View Se The Journal Entry for 1273 4.500 F 13,595 t De Interest Expense De laseb O Cash Lease Payment Les Interest pense Reduction in Principal 18.095 4.500 $13,595 Send a chat 18.095 Capital Lease: Lessee's View Sterou the Remaring se propel amount outstanding as Capital Lease: Lessee's View Steps tough are the repeated for the remaining two years of the lease 45.000 Principal Outstanding on 1/1 Les Mild Remarang po 12/31/Year 2 journal Entry De Interest Expense 3,141 De Lease Liability 14.954 O Cash 18095 31.05 Capital Lease: Lessee's View - 12/31/Year 3 journal erty: line Capital Lease: Lessee's View Comparison costs capitale vs operating lease Over the three years of the bo Send a chat De Interest Expense De lesse C.Cash 164 16,451 18.09 O Lessor's View: Capital Lease Entries on // Year I to record the sale Capital Lease (continued) Entry to record the lease payment received on 12/01/Year: 12e the tale Dr. Lease Recei O Ses Revenue De Cost of Goods Sold 45,000 45.000 379.000 $39.000 Dr Cash erest Revenue Of Lease Receivable $18,095 4,500 11,595 table Capital Lease (continued): - 12/31/ar 2 journal Capital Lease (continued): 12/31/Year 3 Journal Entry: Orerest Receable Lease Recebe $18,095 33,141 S 14.954 elle De Cash Interest Revenue Glease Receivable $18,095 $1,644 16,451 16,451 Send a chat 3 orale O