Question

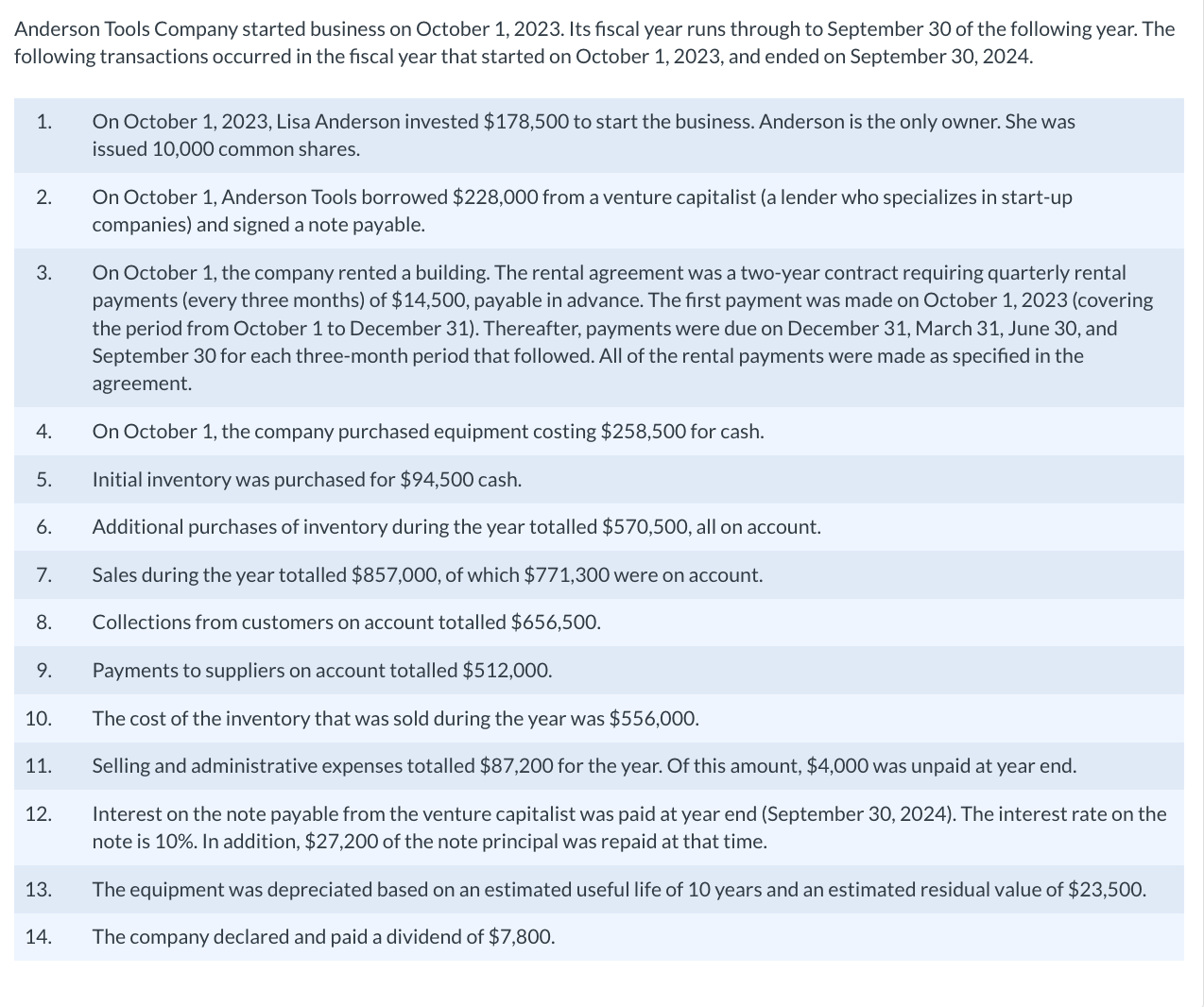

Anderson Tools Company started business on October 1,2023. Its fiscal year runs through to September 30 of the following year. The following transactions occurred in

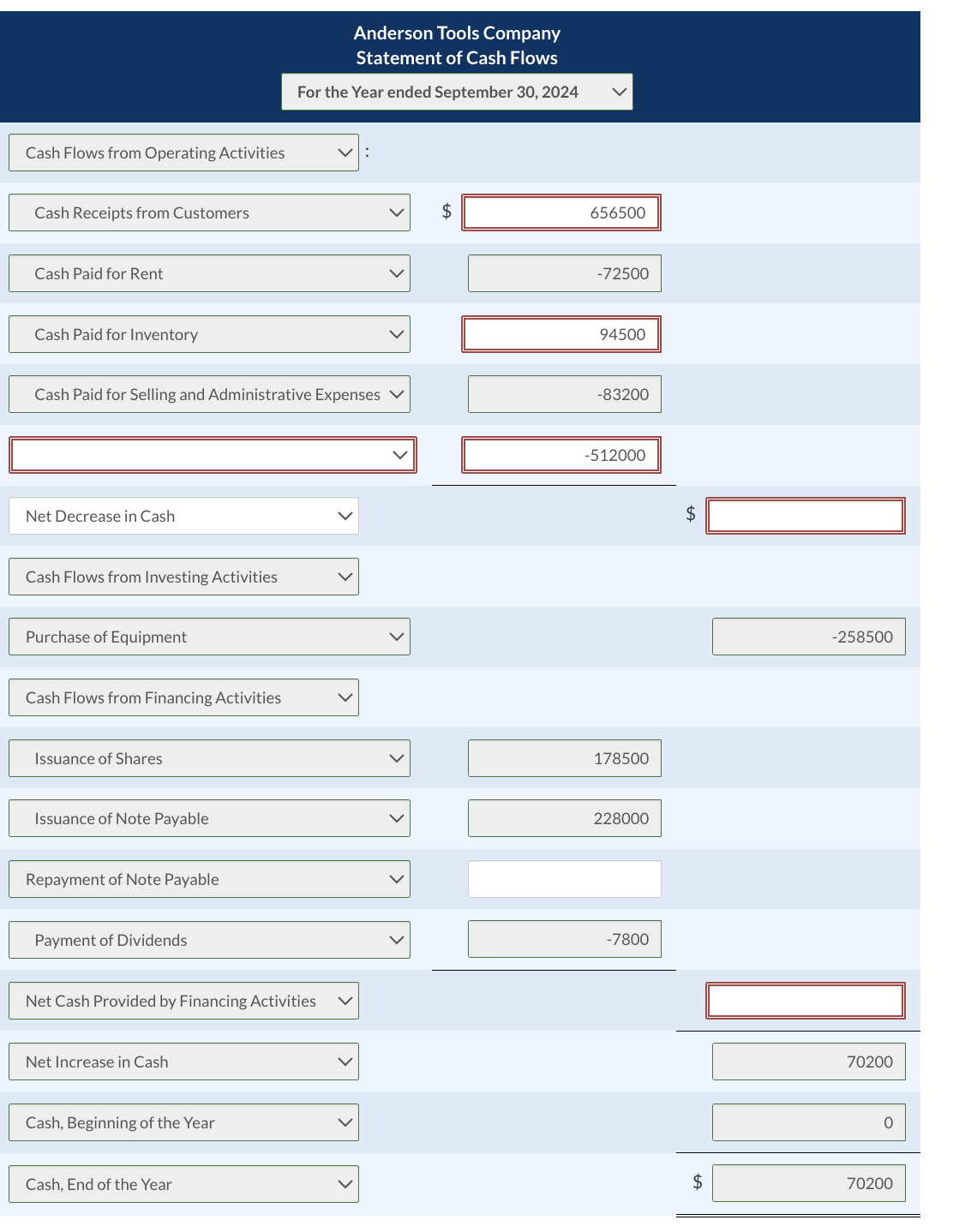

Anderson Tools Company started business on October 1,2023. Its fiscal year runs through to September 30 of the following year. The following transactions occurred in the fiscal year that started on October 1, 2023, and ended on September 30, 2024. Please create a statement of cash flow.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Agile Audit Transformation And Beyond

Authors: Toby DeRoche

1st Edition

1032062894, 978-1032062891