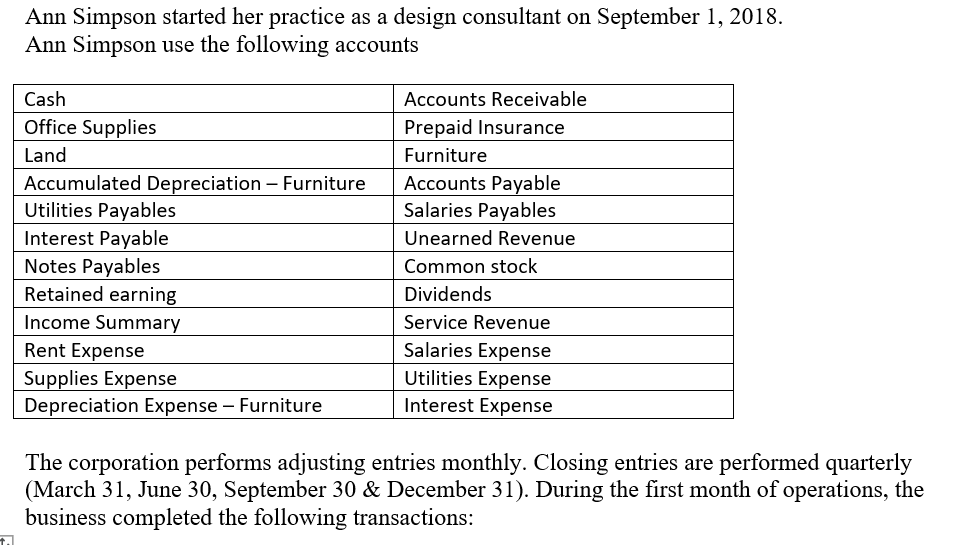

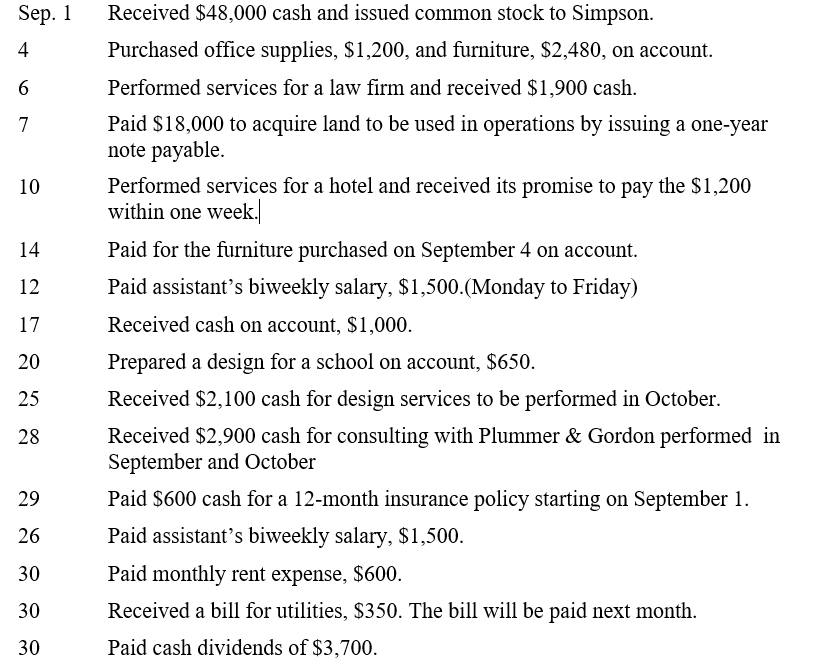

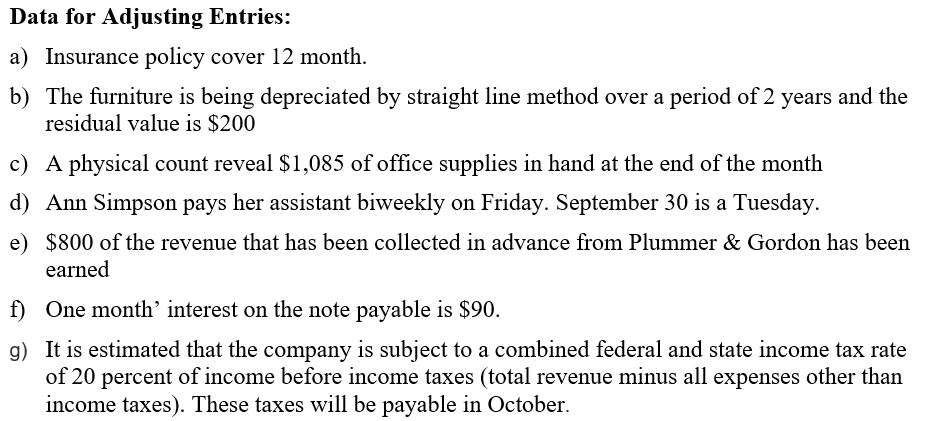

Ann Simpson started her practice as a design consultant on September 1, 2018. Ann Simpson use the following accounts Cash Office Supplies Land Accumulated Depreciation - Furniture Utilities Payables Interest Payable Notes Payables Retained earning Income Summary Rent Expense Supplies Expense Depreciation Expense - Furniture Accounts Receivable Prepaid Insurance Furniture Accounts Payable Salaries Payables Unearned Revenue Common stock Dividends Service Revenue Salaries Expense Utilities Expense Interest Expense The corporation performs adjusting entries monthly. Closing entries are performed quarterly (March 31, June 30, September 30 & December 31). During the first month of operations, the business completed the following transactions: + Sep. 1 4 6 7 10 14 12 17 Received $48,000 cash and issued common stock to Simpson. Purchased office supplies, $1,200, and furniture, $2,480, on account. Performed services for a law firm and received $1,900 cash. a Paid $18,000 to acquire land to be used in operations by issuing a one-year note payable. Performed services for a hotel and received its promise to pay the $1,200 within one week. Paid for the furniture purchased on September 4 on account. Paid assistant's biweekly salary, $1,500.(Monday to Friday) Received cash on account, $1,000. Prepared a design for a school on account, $650. Received $2,100 cash for design services to be performed in October. Received $2,900 cash for consulting with Plummer & Gordon performed in September and October Paid $600 cash for a 12-month insurance policy starting on September 1. Paid assistant's biweekly salary, $1,500. Paid monthly rent expense, $600. Received a bill for utilities, $350. The bill will be paid next month. Paid cash dividends of $3,700. 20 25 28 29 26 30 30 30 Data for Adjusting Entries: a) Insurance policy cover 12 month. b) The furniture is being depreciated by straight line method over a period of 2 years and the residual value is $200 c) A physical count reveal $1,085 of office supplies in hand at the end of the month d) Ann Simpson pays her assistant biweekly on Friday. September 30 is a Tuesday. e) $800 of the revenue that has been collected in advance from Plummer & Gordon has been earned f) One month' interest on the note payable is $90. g) It is estimated that the company is subject to a combined federal and state income tax rate of 20 percent of income before income taxes (total revenue minus all expenses other than income taxes). These taxes will be payable in October. Instructions a. Perform the following steps of the accounting cycle for the month of September: 1. Journalize the September transactions. Do not record adjusting entries at this point. 2. Post the September transactions to the appropriate ledger accounts. 3. Prepare the unadjusted trial balance columns of a 10-column worksheet for the year ended September 30. 4. Prepare the necessary adjusting entries for September. 5. Post the September adjusting entries to the appropriate ledger accounts. 6. Complete the 10-column worksheet for the year ended September 30. b. Prepare an income statement and statement of retained earnings for the quarter ended September 30, and a balance sheet (in report form) as of September 30. C. Prepare required disclosures to accompany the September 30 financial statements. Your solution should include a separate note addressing each of the following areas: (1) depreciation policy, (2) maturity dates of major liabilities. d. Prepare closing entries and post to ledger accounts. e. Prepare an after-closing trial balance as of September 30