Answered step by step

Verified Expert Solution

Question

1 Approved Answer

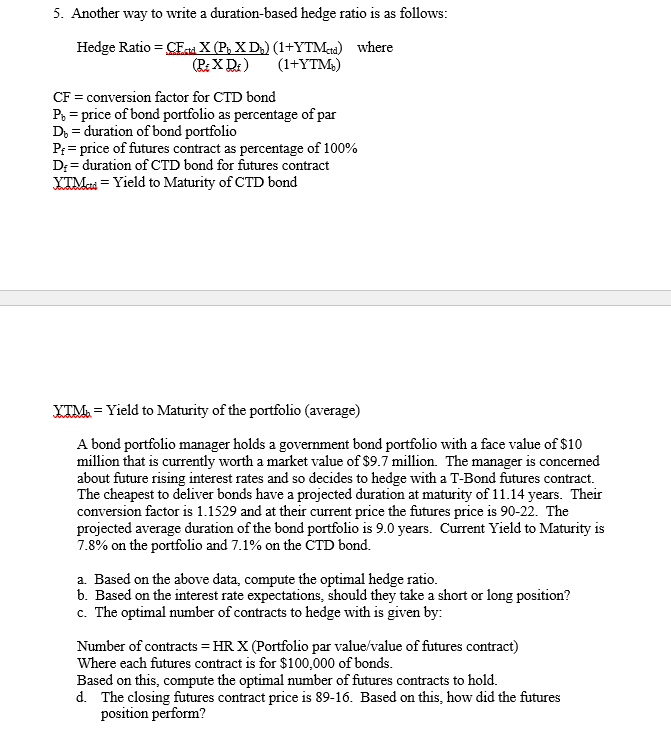

Another way to write a duration - based hedge ratio is as follows: Hedge Ratio = C F c o t d x ( P

Another way to write a durationbased hedge ratio is as follows:

Hedge Ratio where

conversion factor for CTD bond

price of bond portfolio as percentage of par

duration of bond portfolio

price of futures contract as percentage of

duration of CTD bond for futures contract

YTd Yield to Maturity of CTD bond

Yield to Maturity of the portfolio average

A bond portfolio manager holds a government bond portfolio with a face value of $

million that is currently worth a market value of $ million. The manager is concerned

about future rising interest rates and so decides to hedge with a TBond futures contract.

The cheapest to deliver bonds have a projected duration at maturity of years. Their

conversion factor is and at their current price the futures price is The

projected average duration of the bond portfolio is years. Current Yield to Maturity is

on the portfolio and on the CTD bond.

a Based on the above data, compute the optimal hedge ratio.

b Based on the interest rate expectations, should they take a short or long position?

c The optimal number of contracts to hedge with is given by:

Number of contracts HR X Portfolio par valuevalue of futures contract

Where each futures contract is for $ of bonds.

Based on this, compute the optimal number of futures contracts to hold.

d The closing futures contract price is Based on this, how did the futures

position perform?

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Old Money New Woman How To Manage Your Money And Your Life

Authors: Byron Tully

1st Edition

1950118010, 978-1950118014