Answered step by step

Verified Expert Solution

Question

1 Approved Answer

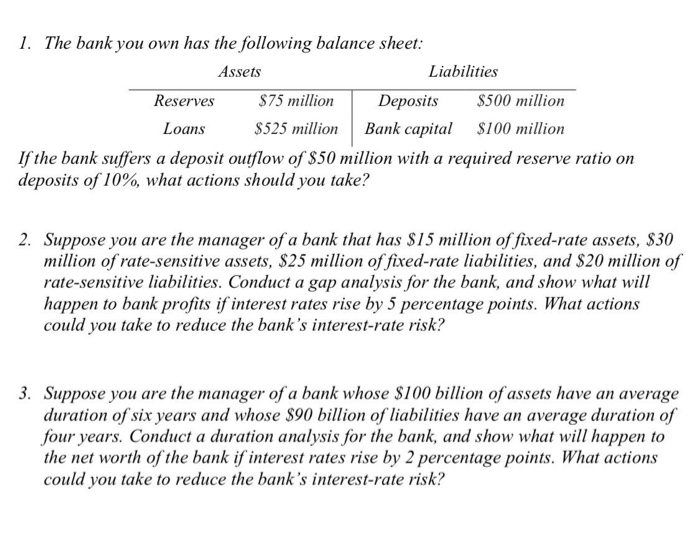

ANSWER 3 ONLY 1. The bank you own has the following balance sheet: Assets Liabilities Reserves $75llon Deposits S500 million Loans S525 million Bank caita

ANSWER 3 ONLY

ANSWER 3 ONLY Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Currency Wars Offense And Defense Through Systemic Thinking

Authors: Jeffrey Yi-Lin Forrest , Yirong Ying , Zaiwu Gong

1st Edition

3319677640,3319677659