Answered step by step

Verified Expert Solution

Question

1 Approved Answer

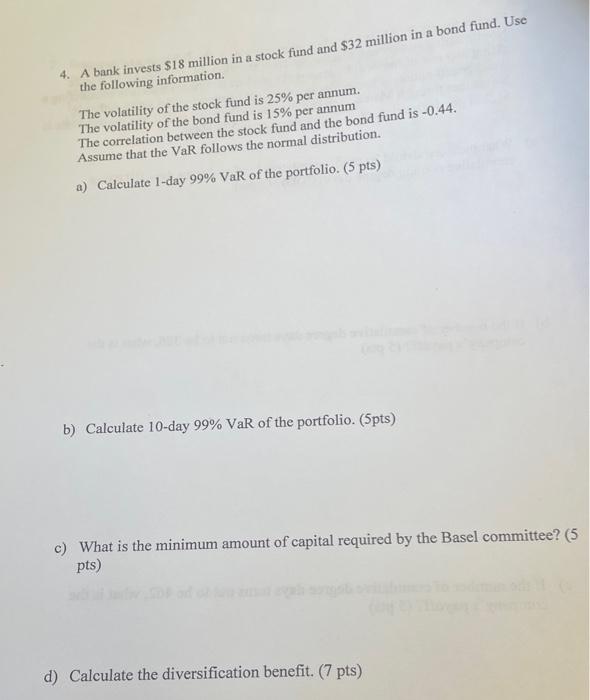

answer all parts of question 4. A bank invests $18 million in a stock fund and $32 million in a bond fund. Use the following

answer all parts of question  4. A bank invests $18 million in a stock fund and $32 million in a bond fund. Use the following information, The volatility of the stock fund is 25% per annum. The volatility of the bond fund is 15% per annum The correlation between the stock fund and the bond fund is -0.44. Assume that the VaR follows the normal distribution. a) Calculate 1-day 99% VaR of the portfolio. (5 pts) b) Calculate 10-day 99% VaR of the portfolio. (5pts) c) What is the minimum amount of capital required by the Basel committee? (5 pts) d) Calculate the diversification benefit. (7 pts)

4. A bank invests $18 million in a stock fund and $32 million in a bond fund. Use the following information, The volatility of the stock fund is 25% per annum. The volatility of the bond fund is 15% per annum The correlation between the stock fund and the bond fund is -0.44. Assume that the VaR follows the normal distribution. a) Calculate 1-day 99% VaR of the portfolio. (5 pts) b) Calculate 10-day 99% VaR of the portfolio. (5pts) c) What is the minimum amount of capital required by the Basel committee? (5 pts) d) Calculate the diversification benefit. (7 pts)

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Restructuring Retirement Risks

Authors: David Blitzstein , Olivia S. Mitchell , Stephen P. Utkus

1st Edition

0199204659,0191525456