:Answer all please.

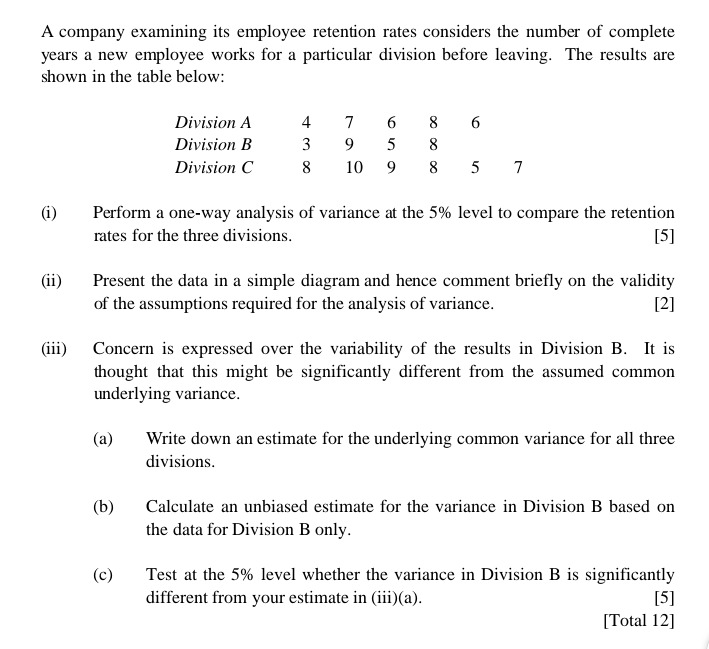

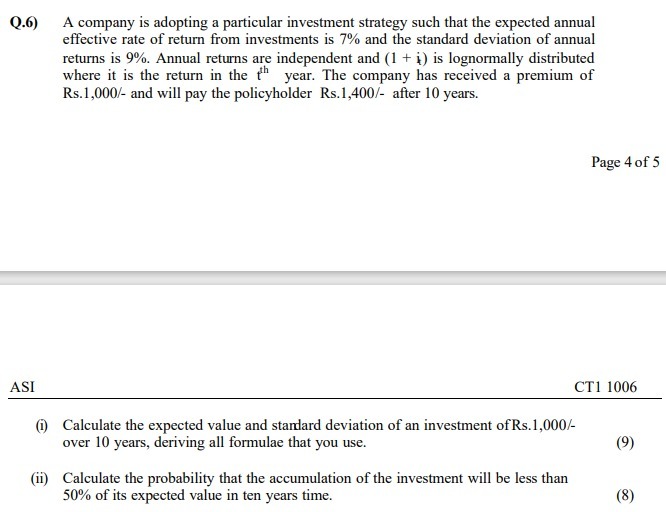

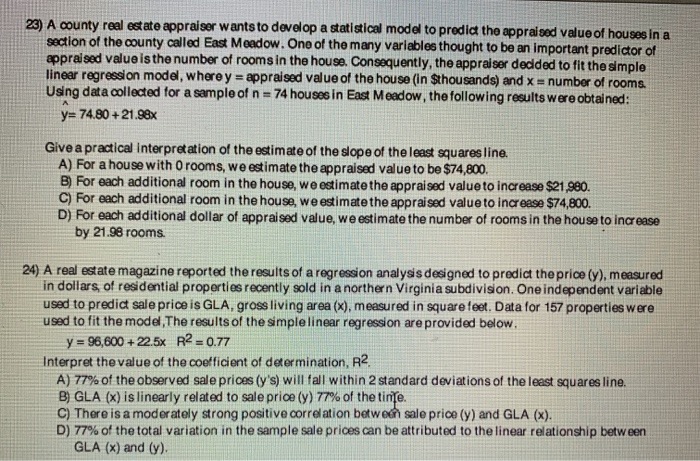

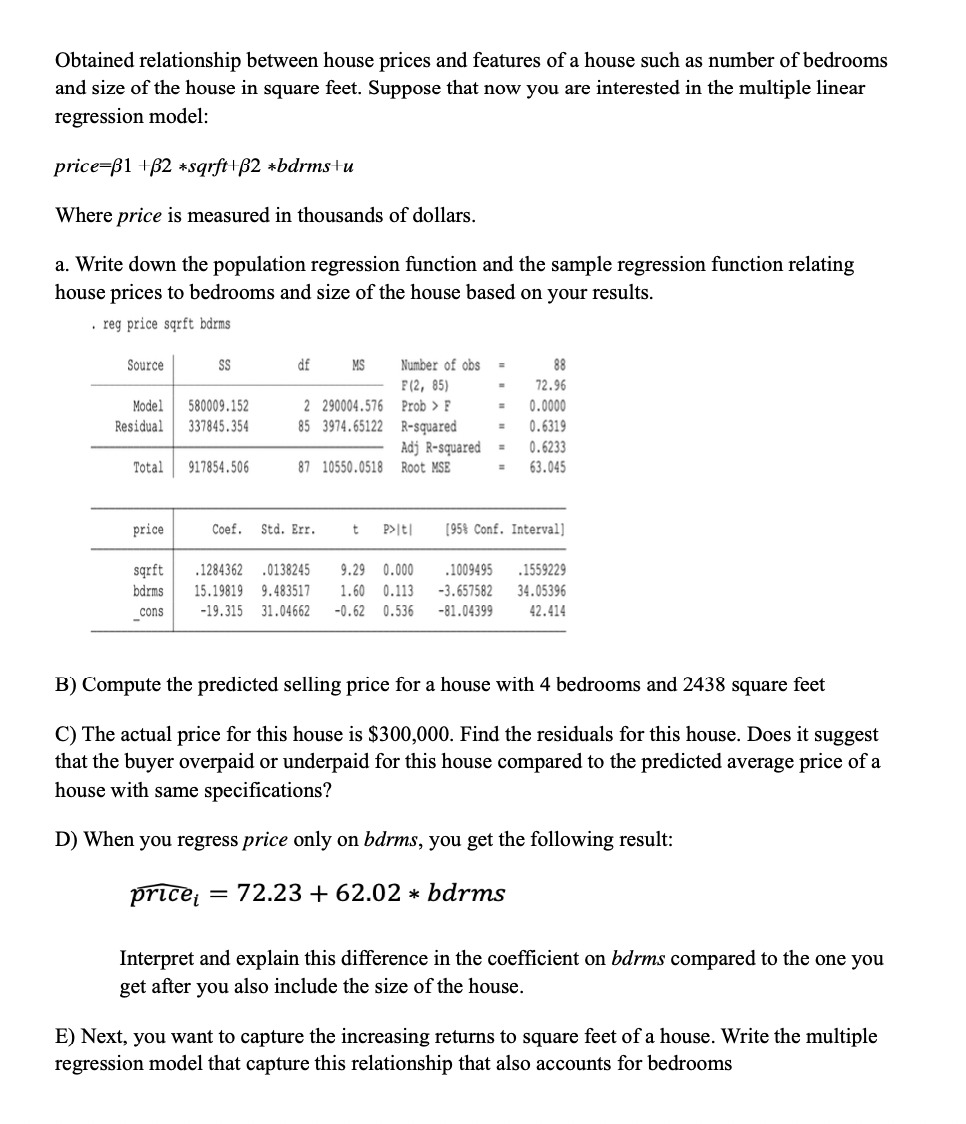

A company examining its employee retention rates considers the number of complete years a new employee works for a particular division before leaving. The results are shown in the table below: Division A 6 Division B Division C 8 10 5 7 (i) Perform a one-way analysis of variance at the 5% level to compare the retention rates for the three divisions. [5] (ii) Present the data in a simple diagram and hence comment briefly on the validity of the assumptions required for the analysis of variance. [2] (iii) Concern is expressed over the variability of the results in Division B. It is thought that this might be significantly different from the assumed common underlying variance. (a) Write down an estimate for the underlying common variance for all three divisions. (b) Calculate an unbiased estimate for the variance in Division B based on the data for Division B only. (c) Test at the 5% level whether the variance in Division B is significantly different from your estimate in (iii)(a). [5] [Total 12]().6) A company is adopting a particular investment strategy such that the expected annual effective rate of return from investments is 7% and the standard deviation of annual returns is 9%. Annual returns are independent and (1 + i) is lognormally distributed where it is the return in the ( year. The company has received a premium of Rs.1,000/- and will pay the policyholder Rs.1,400/- after 10 years. Page 4 of 5 ASI CT1 1006 (1) Calculate the expected value and standard deviation of an investment of Rs.1,000/- over 10 years, deriving all formulae that you use. (9) (ii) Calculate the probability that the accumulation of the investment will be less than 50% of its expected value in ten years time. (8)23) A county real estate appraiser wants to develop a statistical model to predict the appraised value of houses in a section of the county called East Meadow. One of the many variables thought to be an important predictor of appraised value is the number of rooms in the house. Consequently, the appraiser decided to fit the simple linear regression model, where y = appraised value of the house (in $thousands) and x = number of rooms. Using data collected for a sample of n = 74 houses in East Meadow, the following results were obtained: y= 74.80 + 21.98x Give a practical Interpretation of the estimate of the slope of the least squares line. A) For a house with 0 rooms, we estimate the appraised value to be $74,800, B) For each additional room in the house, we estimate the appraised value to increase $21,980. C) For each additional room in the house, we estimate the appraised value to increase $74,800. D) For each additional dollar of appraised value, we estimate the number of rooms in the house to increase by 21.98 rooms. 24) A real estate magazine reported the results of a regression analysis designed to predict the price (y), measured in dollars, of residential properties recently sold in a northern Virginia subdivision. One independent variable used to predict sale price is GLA, gross living area (x), measured in square feet. Data for 157 properties were used to fit the model, The results of the simple linear regression are provided below, y = 96,600 + 22.5x R2 = 0.77 Interpret the value of the coefficient of determination, R2. A) 77% of the observed sale prices (y's) will fall within 2 standard deviations of the least squares line. B) GLA (x) is linearly related to sale price (y) 77% of the time. C) There is a moderately strong positive correlation between sale price (y) and GLA (x). D) 77% of the total variation in the sample sale prices can be attributed to the linear relationship between GLA (x) and (y)Obtained relationship between house prices and features of a house such as number of bedrooms and size of the house in square feet. Suppose that now you are interested in the multiple linear regression model: price=1 +492 *sqerZ *bdnns+u Where price is measured in thousands of dollars. a. Write down the population regression mction and the sample regression lnction relating house prices to bedrooms and size of the house based on your results. . rag price aqrft bdrm Source SS at MS Huber of obs - 08 m. 85] - 12.96 Model 580009.152 2 200004.516 Prob > E . 0.0000 Residual 331845.351 85 3914.55122 R-squared - 0.6319 Mj R-squared I 0.5233 Total 917854.505 E? 10550.0510 Root H53 I 63.005 price Coat. Std. Err. t P>lt| {95% Cent. Interval] sqrft .1234352 .0135215 9.29 0.000 .1009495 .1559229 bdrms 15.19319 9.43351? 1.60 0.113 -3.651502 34.05396 _ccns -19.315 31.0465! -.62 0.536 -81.0439 i2.ill B) Compute the predicted selling price for a house with 4 bedrooms and 2438 square feet C) The actual price for this house is $300,000. Find the residuals for this house. Does it suggest that the buyer overpaid or underpaid for this house compared to the predicted average price of a house wii same specications? D) When you regress price only on bdrms, you get the following result: no t = 72.23 + 62.02 * bdrms Interpret and explain this di'erence in the coefcient on bdnns compared to the one you get after you also include the size of the house. E) Next, you want to capture the increasing returns to square feet of a house. Write the multiple regression model that capture this relationship that also accounts for bedrooms Part I: Theoretical Questions 1. Consider two independent random variables, X and Y. Random variable X takes value of 1 with probability 3/4 and value of zero otherwise. Random variable Y is uniformly distributed on [0.2] interval. (a) Find mean and variance of random variable X. [3 marks] (b) Find mean and variance of random variable Y. [3 marks] (c) Find covariance of X and Y. [3 marks] (d) Find variance of random variable Y+3X. [3 marks] 2. Consider an ARMA(2,1) process J": = elytl 'l' Bah2 'l' 5t 'l' 'l'Etln where e, is white noise. (a) Under what conditions is this process covariance stationary? Explain your answer. [5 marks] (b) Assuming that the process is covariance stationary. derive the mean and covariance function of this process. [10 marks] 3. Write down the theoretical expressions for one-step-ahead, two-step-ahead and three-stepahead forecasts from an ARMA(1,2) with non-zero mean. Compute the theoretical forecast error and variance of the forecast error. Does the variance of the forecast error converge as h > Do? If so, what value does it converge to? Explain your answer. [15 marks] 4. Suppose that {y,} and {at} are 1(1) processes. but ytzt is 1(0) for some 34E 0. Show that for any 5 96 [3, y1r '53: is HI). [6 marks] 5. Let th be the annual growth in the money supply and let unemt be the unemployment rate. Assuming that unemt follows a stationary AR( 1) process. explain in detail how you would test whether gM Granger causes unem. [5 marks]