Answered step by step

Verified Expert Solution

Question

1 Approved Answer

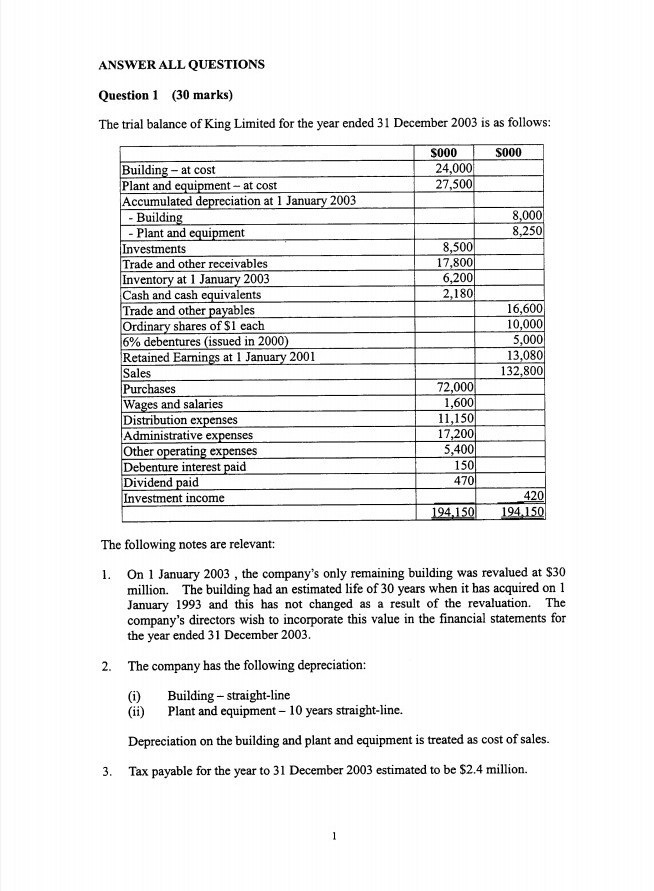

ANSWER ALL QUESTIONS Question 1 (30 marks) The trial balance of King Limited for the year ended 31 December 2003 is as follows: 000 S000

ANSWER ALL QUESTIONS Question 1 (30 marks) The trial balance of King Limited for the year ended 31 December 2003 is as follows: 000 S000 24,000 27,500 8.000 8.250 8,500 17,800 6,200 2,180 Building - at cost Plant and equipment - at cost Accumulated depreciation at 1 January 2003 - Building - Plant and equipment Investments Trade and other receivables Inventory at 1 January 2003 Cash and cash equivalents Trade and other payables Ordinary shares of $1 each 6% debentures (issued in 2000) Retained Earnings at 1 January 2001 Sales Purchases Wages and salaries Distribution expenses Administrative expenses Other operating expenses Debenture interest paid Dividend paid Investment income 16,600 10,000 5,000 13,080 132,800 72,000 1,600 11,150 17,200 5,400 150 4701 194.150 194.150 The following notes are relevant: 1. On 1 January 2003, the company's only remaining building was revalued at $30 million. The building had an estimated life of 30 years when it has acquired on 1 January 1993 and this has not changed as a result of the revaluation. The company's directors wish to incorporate this value in the financial statements for the year ended 31 December 2003. 2. The company has the following depreciation: (i) (ii) Building - straight-line Plant and equipment - 10 years straight-line. Depreciation on the building and plant and equipment is treated as cost of sales 3. Tax payable for the year to 31 December 2003 estimated to be $2.4 million. 4. The directors did not recommend the company to distribute dividend for the year ended 31 December 2003. The company conducted an inventory count on 8 January 2004. The value of the inventory on that date was $7 million at cost. Between the year-end and the inventory count the following transactions have been identified: Normal sales at a mark-up on cost of 30% Goods received at cost $ 4,550,000 $ 710,000 All sales and purchased had been correctly recorded in the period in which they occurred. 6. Prepayment and accruals for the year ended 31 December 2003: Accruals Prepayment $000 490 $000 Sundry administrative expenses Wages and salaries 580 Wages and salaries cost is to be allocated: Cost of sales Distribution cost Administrative expenses 10% 20% 70% 7. On I December 2003, the company learned that one of its customers had been unexpectedly placed in liquidation. As a result of this development, King Limited was likely to suffer an abnormally large bad debt of $6 million. King Limited's management decided to write off the loss as bad debts and further make an allowance for doubtful debts for 5% on the remaining trade receivable balance. Allowance for doubtful debts and bad debts are treated as administrative expenses. Required: (a) Prepare journal entries necessary for the proper preparation of the financial statements. (6 marks) (b) Prepare the income statement (classification by function) of King Limited for the year ended 31 December 2003 and a balance sheet as at 31 December 2003 in accordance with Hong Kong accounting practice and the Company Ordinance. (24 marks) Notes to the financial statement are not required but all workings must be shown. ANSWER ALL QUESTIONS Question 1 (30 marks) The trial balance of King Limited for the year ended 31 December 2003 is as follows: 000 S000 24,000 27,500 8.000 8.250 8,500 17,800 6,200 2,180 Building - at cost Plant and equipment - at cost Accumulated depreciation at 1 January 2003 - Building - Plant and equipment Investments Trade and other receivables Inventory at 1 January 2003 Cash and cash equivalents Trade and other payables Ordinary shares of $1 each 6% debentures (issued in 2000) Retained Earnings at 1 January 2001 Sales Purchases Wages and salaries Distribution expenses Administrative expenses Other operating expenses Debenture interest paid Dividend paid Investment income 16,600 10,000 5,000 13,080 132,800 72,000 1,600 11,150 17,200 5,400 150 4701 194.150 194.150 The following notes are relevant: 1. On 1 January 2003, the company's only remaining building was revalued at $30 million. The building had an estimated life of 30 years when it has acquired on 1 January 1993 and this has not changed as a result of the revaluation. The company's directors wish to incorporate this value in the financial statements for the year ended 31 December 2003. 2. The company has the following depreciation: (i) (ii) Building - straight-line Plant and equipment - 10 years straight-line. Depreciation on the building and plant and equipment is treated as cost of sales 3. Tax payable for the year to 31 December 2003 estimated to be $2.4 million. 4. The directors did not recommend the company to distribute dividend for the year ended 31 December 2003. The company conducted an inventory count on 8 January 2004. The value of the inventory on that date was $7 million at cost. Between the year-end and the inventory count the following transactions have been identified: Normal sales at a mark-up on cost of 30% Goods received at cost $ 4,550,000 $ 710,000 All sales and purchased had been correctly recorded in the period in which they occurred. 6. Prepayment and accruals for the year ended 31 December 2003: Accruals Prepayment $000 490 $000 Sundry administrative expenses Wages and salaries 580 Wages and salaries cost is to be allocated: Cost of sales Distribution cost Administrative expenses 10% 20% 70% 7. On I December 2003, the company learned that one of its customers had been unexpectedly placed in liquidation. As a result of this development, King Limited was likely to suffer an abnormally large bad debt of $6 million. King Limited's management decided to write off the loss as bad debts and further make an allowance for doubtful debts for 5% on the remaining trade receivable balance. Allowance for doubtful debts and bad debts are treated as administrative expenses. Required: (a) Prepare journal entries necessary for the proper preparation of the financial statements. (6 marks) (b) Prepare the income statement (classification by function) of King Limited for the year ended 31 December 2003 and a balance sheet as at 31 December 2003 in accordance with Hong Kong accounting practice and the Company Ordinance. (24 marks) Notes to the financial statement are not required but all workings must be shown

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Forest Management Auditing

Authors: Lucio Brotto

1st Edition

0367605872, 978-0367605872