Answered step by step

Verified Expert Solution

Question

1 Approved Answer

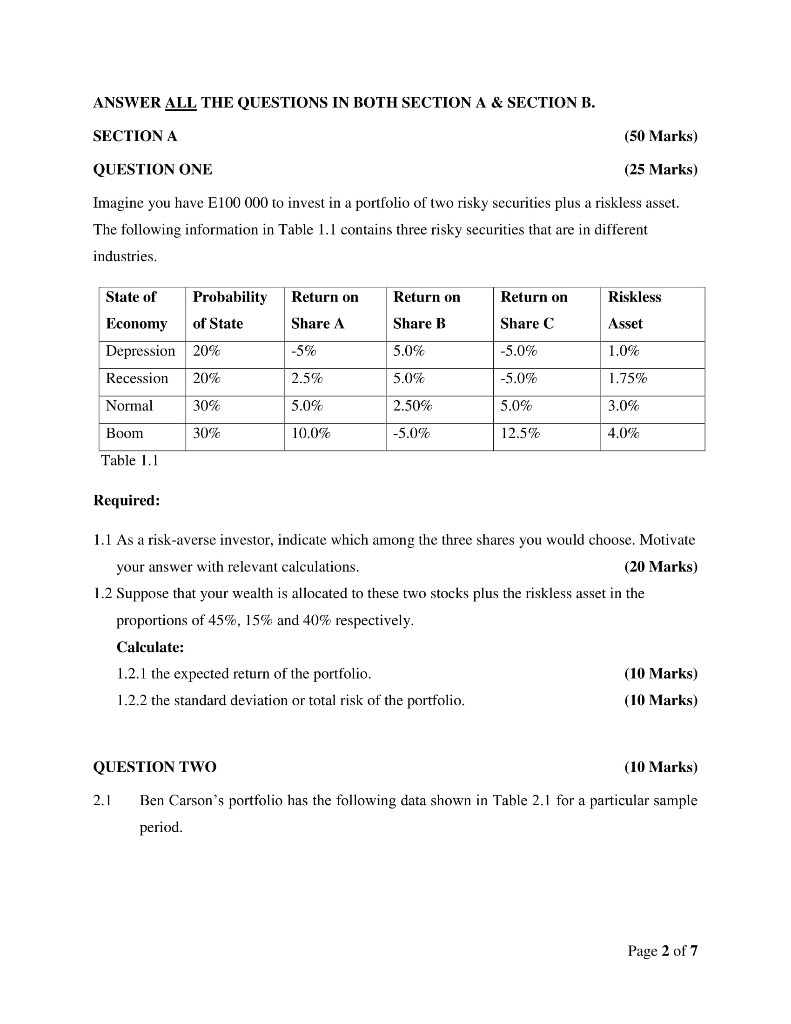

ANSWER ALL THE QUESTIONS IN BOTH SECTION A & SECTION B. SECTION A (50 Marks) QUESTION ONE (25 Marks) Imagine you have E100 000 to

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Private Funds Where And How

Authors: Dechert LLP

2018 Edition

152650300X,1526503018