Answered step by step

Verified Expert Solution

Question

1 Approved Answer

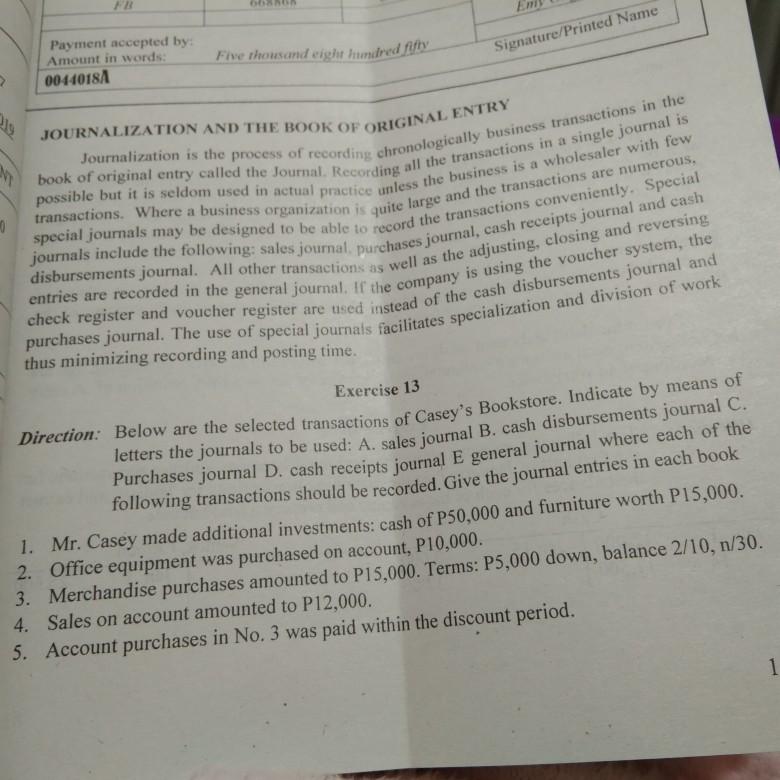

Answer numbers 1-15 with solution and explanation on how you get the answer. Please read the direction. Payment accepted by: Amount in words: 00440181 Five

Answer numbers 1-15 with solution and explanation on how you get the answer. Please read the direction.

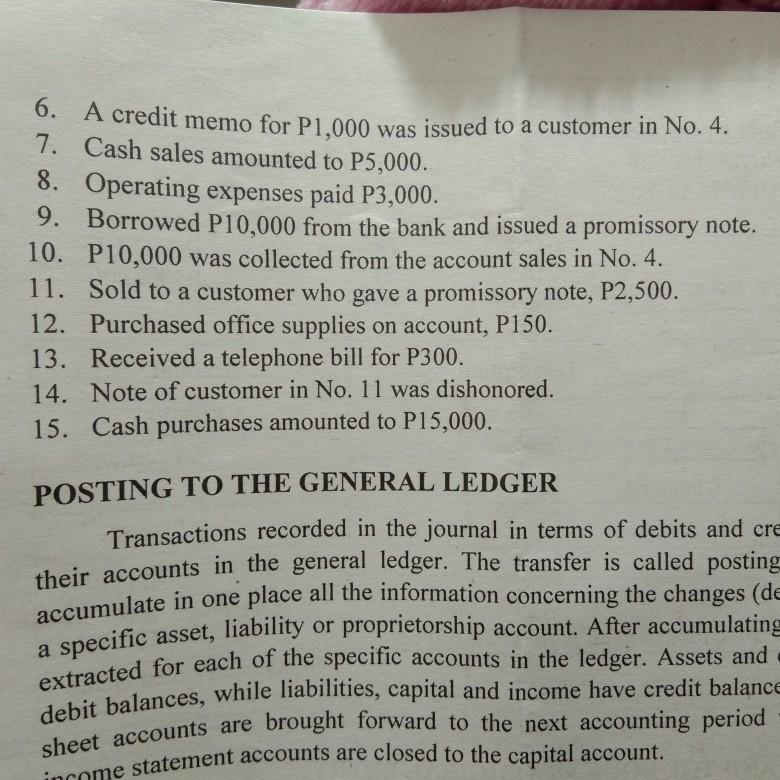

Payment accepted by: Amount in words: 00440181 Five thousand eight hundred fifty Signature/Printed Name JOURNALIZATION AND THE BOOK OF ORIGINAL ENTRY Journalization is the process of recording chronologically business transactions in the possible but it is seldom used in actual practice unless the business is a wholesaler with few book of original entry called the Journal. Recording all the transactions in a single journal is 0 special journals may be designed to be able to record the transactions conveniently. Special transactions. Where a business organization is quite large and the transactions are numerous, disbursements journal. All other transactions as well as the adjusting, closing and reversing journals include the following: sales journal purchases journal, cash receipts journal and cash entries are recorded in the general journal. If the company is using the voucher system, the check register and voucher register are used instead of the cash disbursements journal and purchases journal. The use of special journals facilitates specialization and division of work thus minimizing recording and posting time. Exercise 13 Direction: Below are the selected transactions of Casey's Bookstore. Indicate by means of letters the journals to be used: A. sales journal B. cash disbursements journal C. Purchases journal D. cash receipts journal E general journal where each of the following transactions should be recorded. Give the journal entries in each book 1. Mr. Casey made additional investments: cash of P50,000 and furniture worth P15,000. 2. Office equipment was purchased on account, P10,000. 3. Merchandise purchases amounted to P15,000. Terms: P5,000 down, balance 2/10, n/30. 4. Sales on account amounted to P12,000. 5. Account purchases in No. 3 was paid within the discount period. 1 6. A credit memo for P1,000 was issued to a customer in No. 4. 7. Cash sales amounted to P5,000. 8. Operating expenses paid P3,000. 9. Borrowed P10,000 from the bank and issued a promissory note. 10. P10,000 was collected from the account sales in No. 4. 11. Sold to a customer who gave a promissory note, P2,500. 12. Purchased office supplies on account, P150. 13. Received a telephone bill for P300. 14. Note of customer in No. 11 was dishonored. 15. Cash purchases amounted to P15,000. POSTING TO THE GENERAL LEDGER Transactions recorded in the journal in terms of debits and cre their accounts in the general ledger. The transfer is called posting accumulate in one place all the information concerning the changes (de a specific asset, liability or proprietorship account. After accumulating extracted for each of the specific accounts in the ledger. Assets and debit balances, while liabilities, capital and income have credit balance sheet accounts are brought forward to the next accounting period come statement accounts are closed to the capital account

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

A History Of Auditing The Changing Audit Process In Britain From The Nineteenth Century To The Present Day

Authors: Derek Matthews

1st Edition

0415648343, 978-0415648349