Answered step by step

Verified Expert Solution

Question

1 Approved Answer

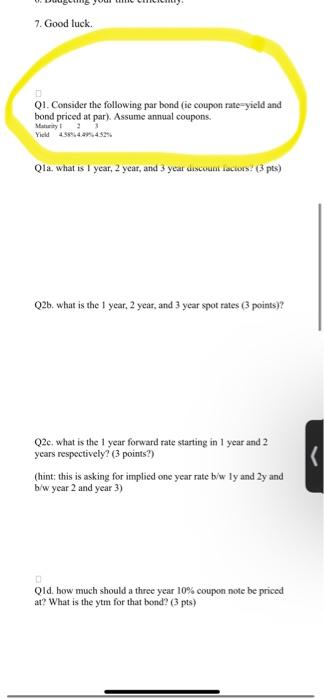

answer Q1D ONLY PLEASE! Q1. Consider the following par bond (ie coupon rate-yield and bond priced at park. Assume annual coupons. Q1a. What is 1

answer Q1D ONLY PLEASE!

Q1. Consider the following par bond (ie coupon rate-yield and bond priced at park. Assume annual coupons. Q1a. What is 1 year, 2 year, and 3 year discueni lactors: (3 pts ) Q2b. what is the 1 year, 2 year, and 3 year spot rates ( 3 points)? Q2e, what is the 1 year forward rate starting in 1 year and 2 years respectively? ( 3 points?) (hint: this is asking for implied one year rate b/w ly and 2y and b/w year 2 and year 3) Qld. bow much should a three year 10% coupon note be priced at? What is the ytm for that bond? (3 pts) Q1. Consider the following par bond (ie coupon rate-yield and bond priced at park. Assume annual coupons. Q1a. What is 1 year, 2 year, and 3 year discueni lactors: (3 pts ) Q2b. what is the 1 year, 2 year, and 3 year spot rates ( 3 points)? Q2e, what is the 1 year forward rate starting in 1 year and 2 years respectively? ( 3 points?) (hint: this is asking for implied one year rate b/w ly and 2y and b/w year 2 and year 3) Qld. bow much should a three year 10% coupon note be priced at? What is the ytm for that bond? (3 pts) Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Research In Finance Volume 24

Authors: Andrew H. Chen

1st Edition

0762313773, 978-0762313778