Answer Question 1 from the case study image above (question is also posted below same from case study)

- Conduct research to (i) find out the PCAOB auditing standard related to the use of analytical procedure during audit; (ii) List the four factors impacting the expected effectiveness and efficiency of analytical procedure; (iii) list at least four requirements in the standard related to developing an expectation and conducting analytical procedures when those procedures are intended to provide substantive evidence. (1 point. Point allocation: 0.2 point for (i); 0.4 point for (ii); 0.4 point for (iii))Conduct research to (i) find out the PCAOB auditing standard related to the use of analytical procedure during audit; (ii) List the four factors impacting the expected effectiveness and efficiency of analytical procedure; (iii) list at least four requirements in the standard related to developing an expectation and conducting analytical procedures when those procedures are intended to provide substantive evidence. (1 point. Point allocation: 0.2 point for (i); 0.4 point for (ii); 0.4 point for (iii))

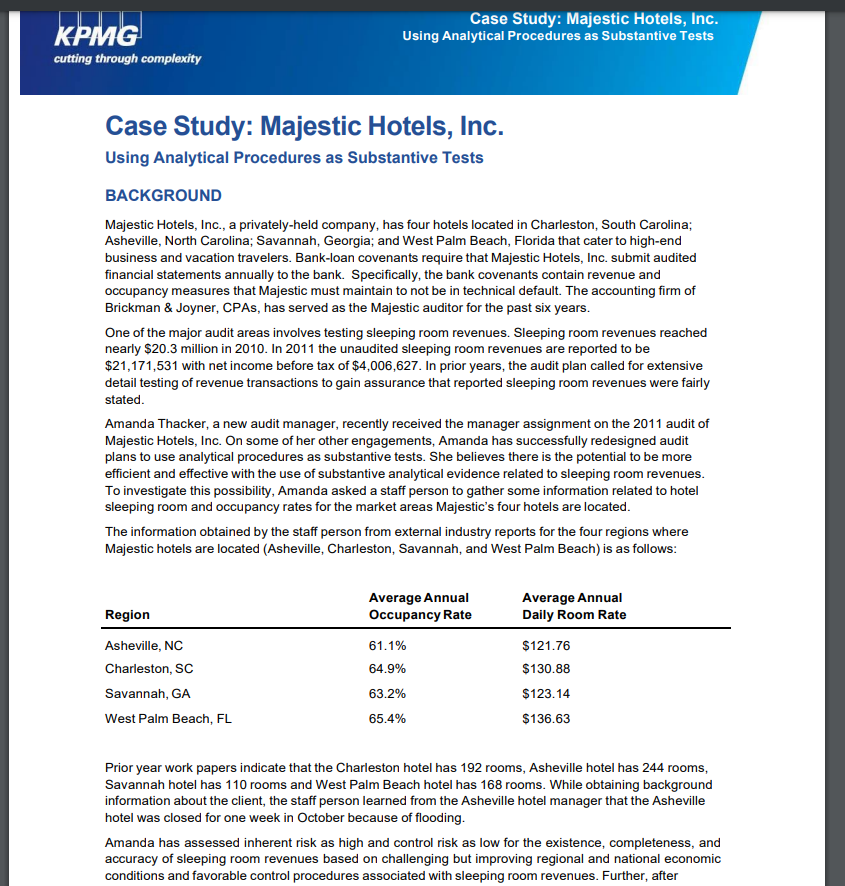

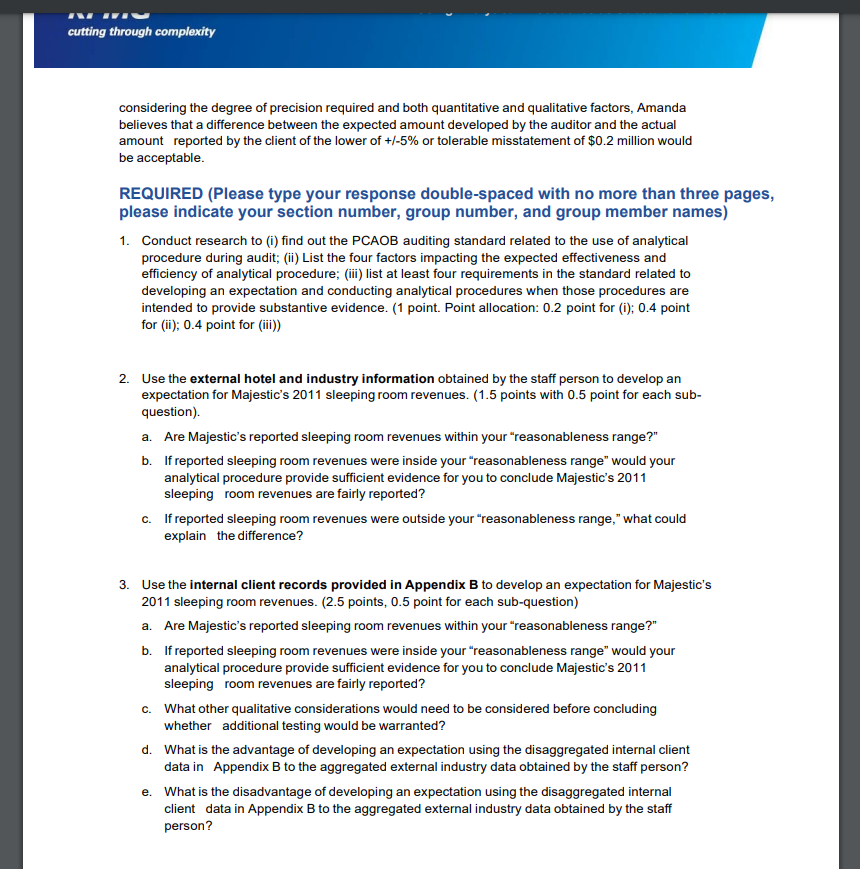

Case Study: Majestic Hotels, Inc. Using Analytical Procedures as Substantive Tests BACKGROUND Majestic Hotels, Inc., a privately-held company, has four hotels located in Charleston, South Carolina; Asheville, North Carolina; Savannah, Georgia; and West Palm Beach, Florida that cater to high-end business and vacation travelers. Bank-loan covenants require that Majestic Hotels, Inc. submit audited financial statements annually to the bank. Specifically, the bank covenants contain revenue and occupancy measures that Majestic must maintain to not be in technical default. The accounting firm of Brickman \& Joyner, CPAs, has served as the Majestic auditor for the past six years. One of the major audit areas involves testing sleeping room revenues. Sleeping room revenues reached nearly \$20.3 million in 2010. In 2011 the unaudited sleeping room revenues are reported to be $21,171,531 with net income before tax of $4,006,627. In prior years, the audit plan called for extensive detail testing of revenue transactions to gain assurance that reported sleeping room revenues were fairly stated. Amanda Thacker, a new audit manager, recently received the manager assignment on the 2011 audit of Majestic Hotels, Inc. On some of her other engagements, Amanda has successfully redesigned audit plans to use analytical procedures as substantive tests. She believes there is the potential to be more efficient and effective with the use of substantive analytical evidence related to sleeping room revenues. To investigate this possibility, Amanda asked a staff person to gather some information related to hotel sleeping room and occupancy rates for the market areas Majestic's four hotels are located. The information obtained by the staff person from external industry reports for the four regions where Majestic hotels are located (Asheville, Charleston, Savannah, and West Palm Beach) is as follows: Prior year work papers indicate that the Charleston hotel has 192 rooms, Asheville hotel has 244 rooms, Savannah hotel has 110 rooms and West Palm Beach hotel has 168 rooms. While obtaining background information about the client, the staff person learned from the Asheville hotel manager that the Asheville hotel was closed for one week in October because of flooding. Amanda has assessed inherent risk as high and control risk as low for the existence, completeness, and accuracy of sleeping room revenues based on challenging but improving regional and national economic conditions and favorable control procedures associated with sleeping room revenues. Further, after considering the degree of precision required and both quantitative and qualitative factors, Amanda believes that a difference between the expected amount developed by the auditor and the actual amount reported by the client of the lower of +/5% or tolerable misstatement of $0.2 million would be acceptable. REQUIRED (Please type your response double-spaced with no more than three pag please indicate your section number, group number, and group member names) 1. Conduct research to (i) find out the PCAOB auditing standard related to the use of analytical procedure during audit; (ii) List the four factors impacting the expected effectiveness and efficiency of analytical procedure; (iii) list at least four requirements in the standard related to developing an expectation and conducting analytical procedures when those procedures are intended to provide substantive evidence. (1 point. Point allocation: 0.2 point for (i); 0.4 point for (ii); 0.4 point for (iii)) 2. Use the external hotel and industry information obtained by the staff person to develop an expectation for Majestic's 2011 sleeping room revenues. (1.5 points with 0.5 point for each subquestion). a. Are Majestic's reported sleeping room revenues within your "reasonableness range?" b. If reported sleeping room revenues were inside your "reasonableness range" would your analytical procedure provide sufficient evidence for you to conclude Majestic's 2011 sleeping room revenues are fairly reported? c. If reported sleeping room revenues were outside your "reasonableness range," what could explain the difference? 3. Use the internal client records provided in Appendix B to develop an expectation for Majestic's 2011 sleeping room revenues. ( 2.5 points, 0.5 point for each sub-question) a. Are Majestic's reported sleeping room revenues within your "reasonableness range?" b. If reported sleeping room revenues were inside your "reasonableness range" would your analytical procedure provide sufficient evidence for you to conclude Majestic's 2011 sleeping room revenues are fairly reported? c. What other qualitative considerations would need to be considered before concluding whether additional testing would be warranted? d. What is the advantage of developing an expectation using the disaggregated internal client data in Appendix B to the aggregated external industry data obtained by the staff person? e. What is the disadvantage of developing an expectation using the disaggregated internal client data in Appendix B to the aggregated external industry data obtained by the staff person