Answered step by step

Verified Expert Solution

Question

1 Approved Answer

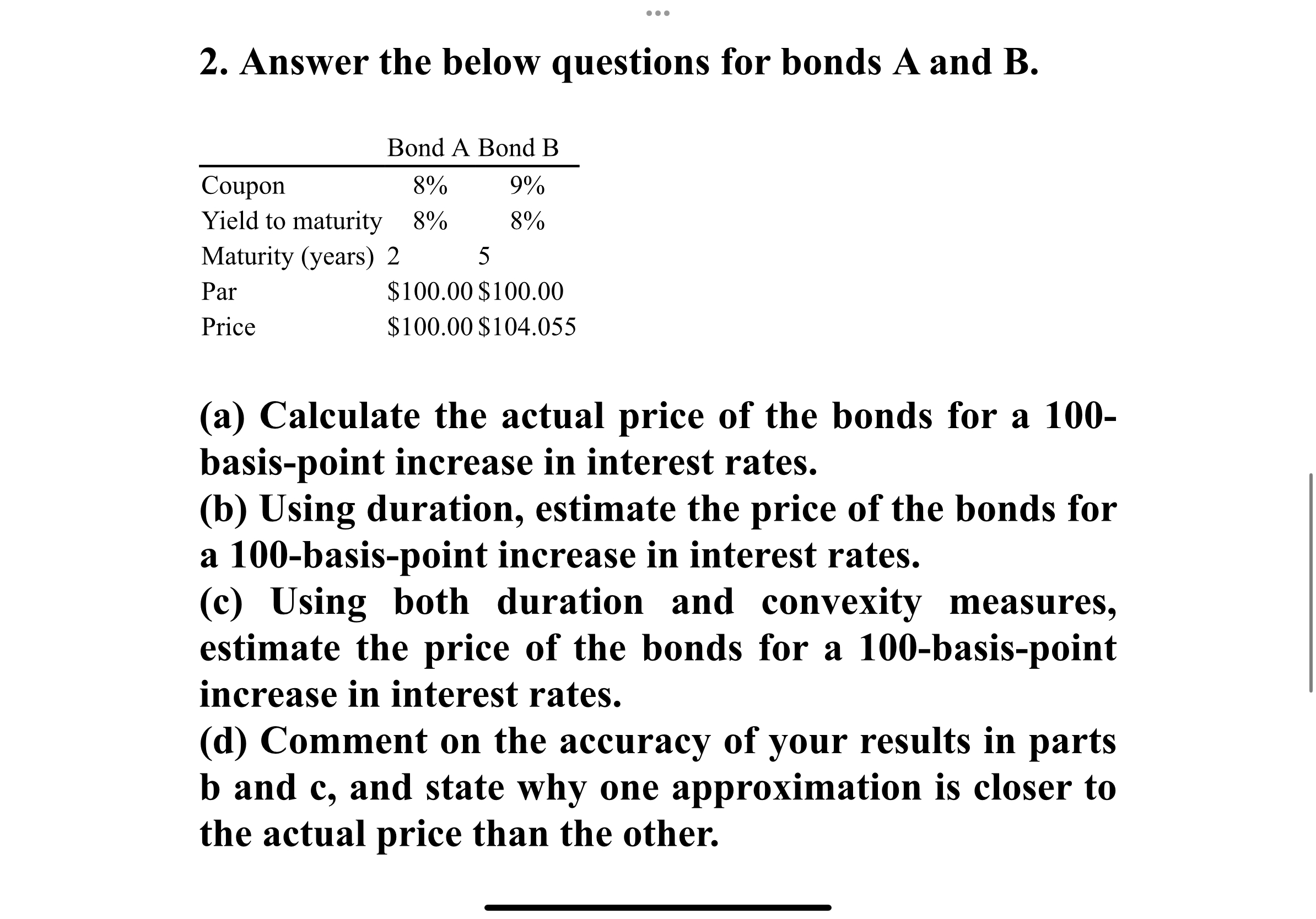

Answer the below questions for bonds A and B . table [ [ , Bond A Bond B ] , [ Coupon , 8

Answer the below questions for bonds A and

tableBond A Bond BCouponYield to maturity,Maturity yearsPar$$Price$$

a Calculate the actual price of the bonds for a basispoint increase in interest rates.

b Using duration, estimate the price of the bonds for a basispoint increase in interest rates.

c Using both duration and convexity measures, estimate the price of the bonds for a basispoint increase in interest rates.

d Comment on the accuracy of your results in parts and and state why one approximation is closer to the actual price than the other.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Finance For Executives Managing For Value Creation

Authors: Gabriel Hawawini, Claude Viallet

2nd Edition

0324117752, 9780324117752