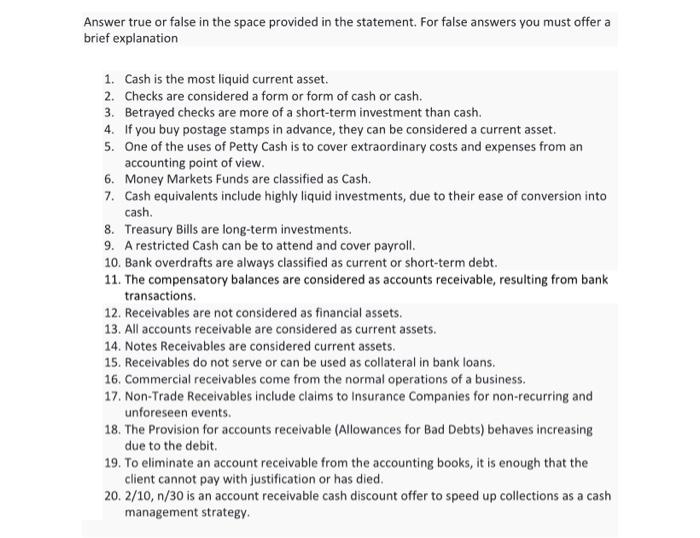

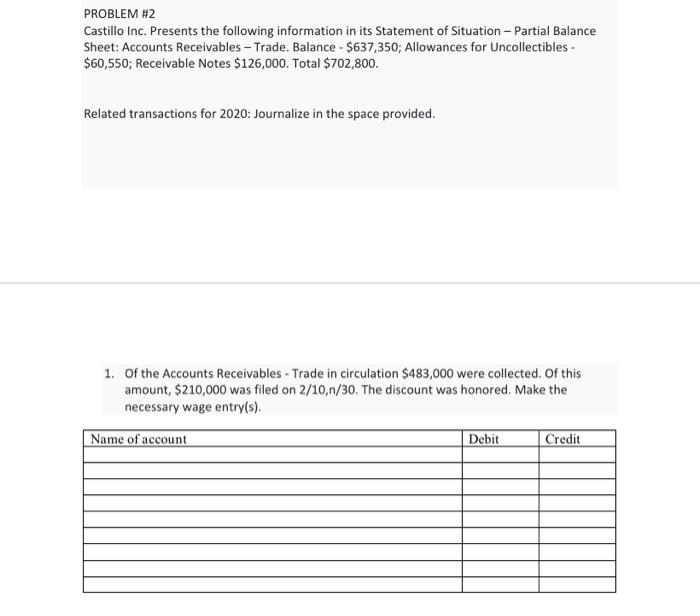

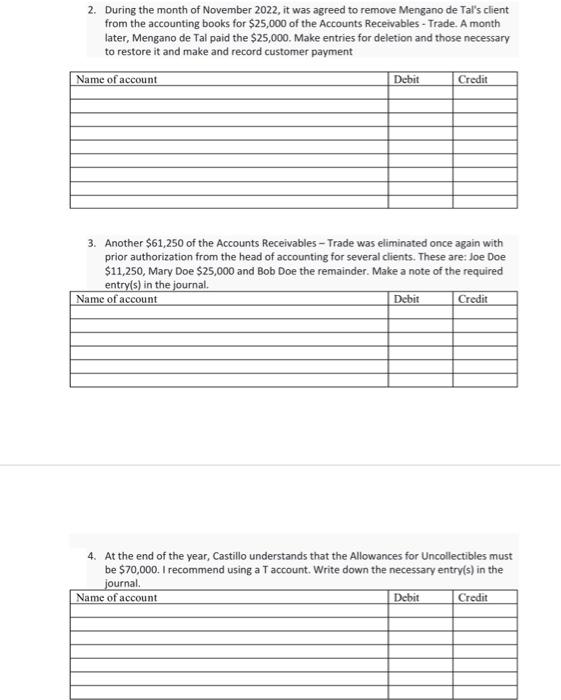

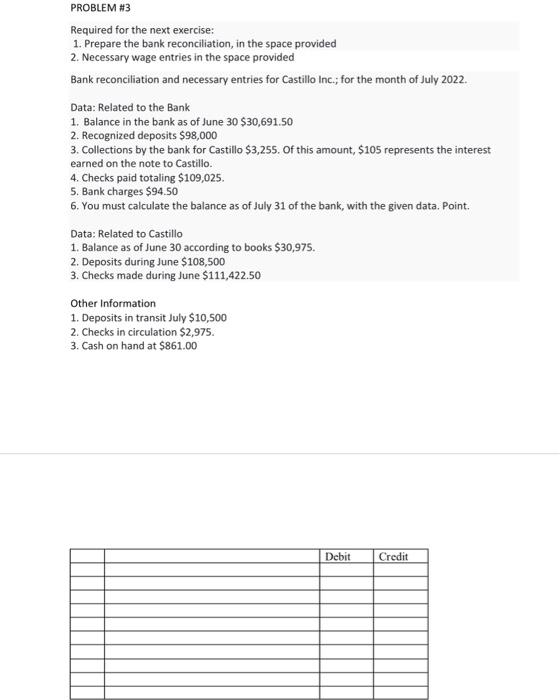

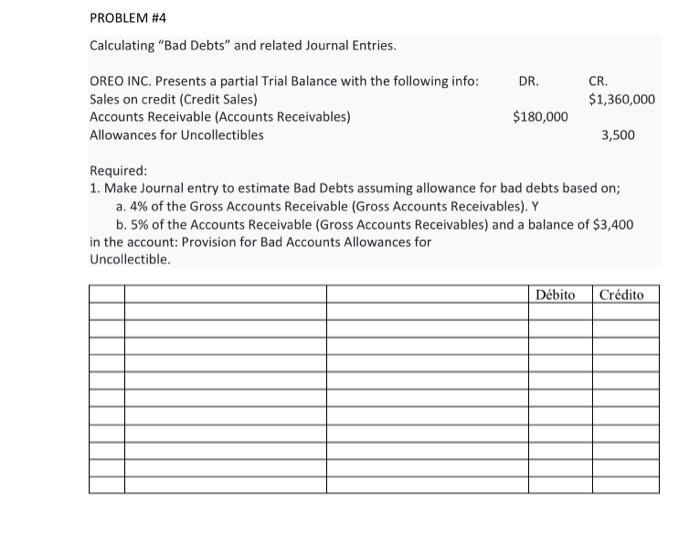

Answer true or false in the space provided in the statement. For false answers you must offer a brief explanation 1. Cash is the most liquid current asset. 2. Checks are considered a form or form of cash or cash. 3. Betrayed checks are more of a short-term investment than cash. 4. If you buy postage stamps in advance, they can be considered a current asset. 5. One of the uses of Petty Cash is to cover extraordinary costs and expenses from an accounting point of view. 6. Money Markets Funds are classified as Cash. 7. Cash equivalents include highly liquid investments, due to their ease of conversion into cash. 8. Treasury Bills are long-term investments. 9. A restricted Cash can be to attend and cover payroll. 10. Bank overdrafts are always classified as current or short-term debt. 11. The compensatory balances are considered as accounts receivable, resulting from bank transactions. 12. Receivables are not considered as financial assets. 13. All accounts receivable are considered as current assets. 14. Notes Receivables are considered current assets. 15. Receivables do not serve or can be used as collateral in bank loans. 16. Commercial receivables come from the normal operations of a business. 17. Non-Trade Receivables include claims to Insurance Companies for non-recurring and unforeseen events. 18. The Provision for accounts receivable (Allowances for Bad Debts) behaves increasing due to the debit. 19. To eliminate an account receivable from the accounting books, it is enough that the client cannot pay with justification or has died. 20. 2/10,n/30 is an account receivable cash discount offer to speed up collections as a cash management strategy. PROBLEM \#2 Castillo Inc. Presents the following information in its Statement of Situation - Partial Balance Sheet: Accounts Receivables - Trade. Balance - $637,350; Allowances for Uncollectibles $60,550; Receivable Notes $126,000. Total $702,800. Related transactions for 2020 : Journalize in the space provided. 1. Of the Accounts Receivables - Trade in circulation $483,000 were collected. Of this amount, $210,000 was filed on 2/10,n/30. The discount was honored. Make the necessary wage entry(s). 2. During the month of November 2022, it was agreed to remove Mengano de Tal's client from the accounting books for $25,000 of the Accounts Receivables - Trade. A month later, Mengano de Tal paid the $25,000. Make entries for deletion and those necessary to restore it and make and record customer payment 3. Another $61,250 of the Accounts Receivables - Trade was eliminated once again with prior authorization from the head of accounting for several clients. These are: Joe Doe $11,250, Mary Doe $25,000 and Bob Doe the remainder. Make a note of the required entruicl in the inurnal 4. At the end of the year, Castillo understands that the Allowances for Uncollectibles must be $70,000. I recommend using a T account. Write down the necessary entry(s) in the PROBLEM \#3 Required for the next exercise: 1. Prepare the bank reconciliation, in the space provided 2. Necessary wage entries in the space provided Bank reconciliation and necessary entries for Castillo Inc.; for the month of July 2022. Data: Related to the Bank 1. Balance in the bank as of June 30$30,691.50 2. Recognized deposits $98,000 3. Collections by the bank for Castillo $3,255. Of this amount, $105 represents the interest earned on the note to Castillo. 4. Checks paid totaling $109,025. 5. Bank charges $94.50 6. You must calculate the balance as of July 31 of the bank, with the given data. Point. Data: Related to Castillo 1. Balance as of June 30 according to books $30,975. 2. Deposits during June $108,500 3. Checks made during June $111,422.50 Other Information 1. Deposits in transit July $10,500 2. Checks in circulation $2,975. 3. Cash on hand at $861.00 Required: 1. Make Journal entry to estimate Bad Debts assuming allowance for bad debts based on; a. 4% of the Gross Accounts Receivable (Gross Accounts Receivables). Y b. 5% of the Accounts Receivable (Gross Accounts Receivables) and a balance of $3,400 in the account: Provision for Bad Accounts Allowances for Uncollectible