answers asap

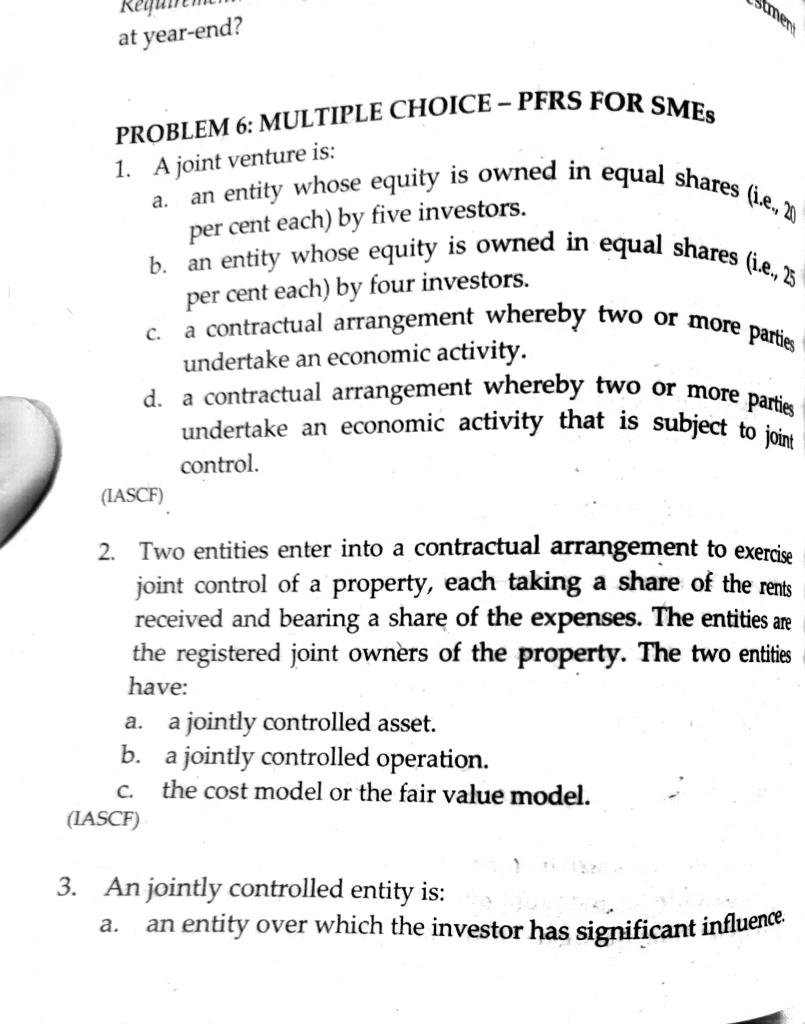

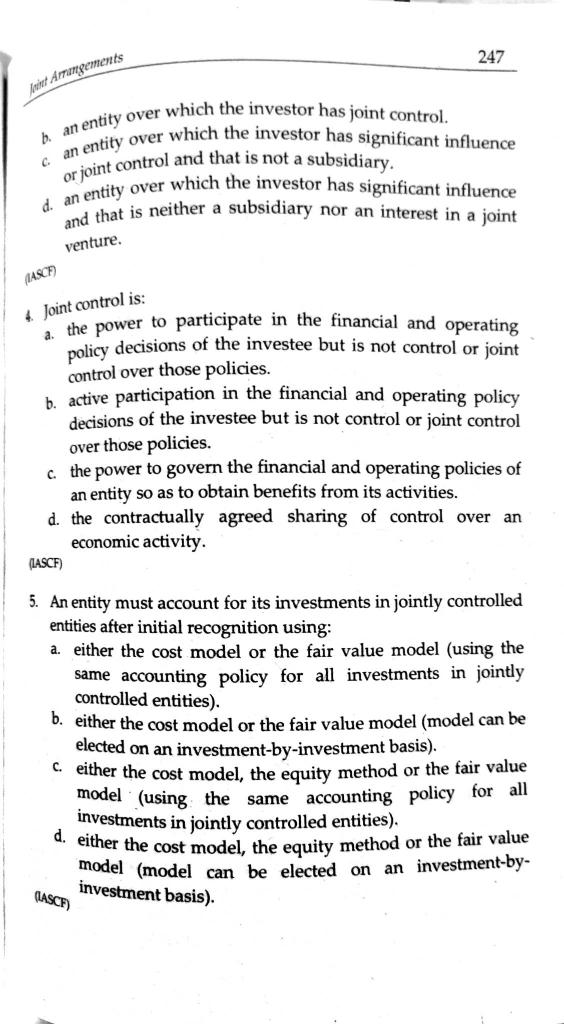

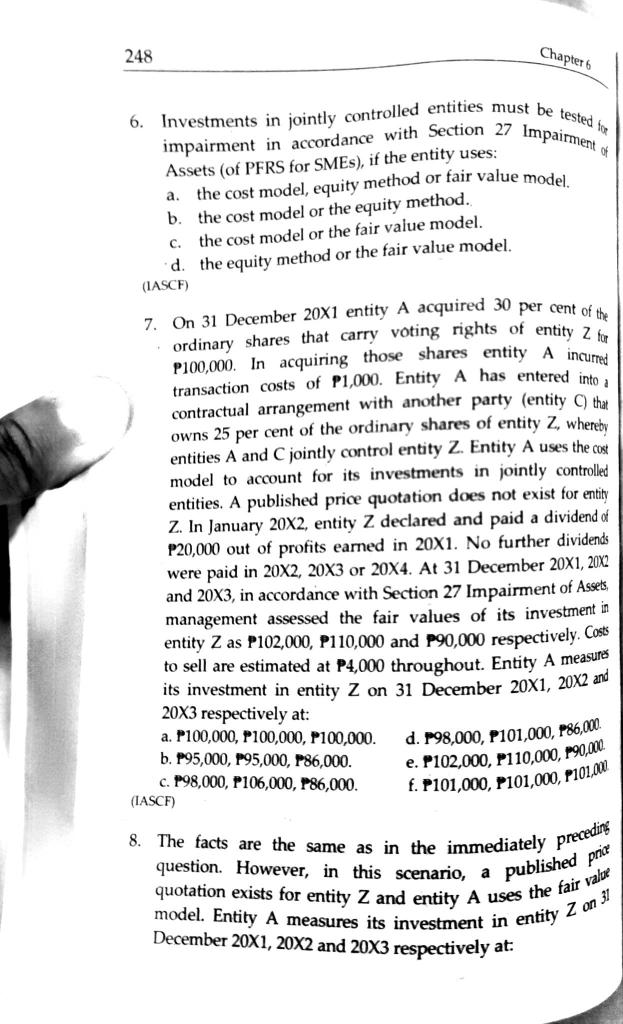

PROBLEM 6: MULTIPLE CHOICE - PFRS FOR SMEs 1. A joint venture is: a. an entity whose equity is owned in equal shares (i,e, 20 b. an entity whose equity is owned in equal shares (i.e., 2. per cent each) by four investors. c. a contractual arrangement whereby two or more parties undertake an economic activity. d. a contractual arrangement whereby two or more parties undertake an economic activity that is subject to joint control. (IASCF) 2. Two entities enter into a contractual arrangement to exercise joint control of a property, each taking a share of the rents received and bearing a share of the expenses. The entities are the registered joint owners of the property. The two entities have: a. a jointly controlled asset. b. a jointly controlled operation. c. the cost model or the fair value model. (IASCF) 3. An jointly controlled entity is: a. an entity over which the investor has significant influence. b. an entity over which the investor has joint control. c. an entity over which the investor has significant influence or joint control and that is not a subsidiary. d. an entity over which the investor has significant influence and that is neither a subsidiary nor an interest in a joint venture. 4. Joint control is: a. the power to participate in the financial and operating policy decisions of the investee but is not control or joint control over those policies. b. active participation in the financial and operating policy decisions of the investee but is not control or joint control over those policies. c. the power to govern the financial and operating policies of an entity so as to obtain benefits from its activities. d. the contractually agreed sharing of control over an economic activity. (ASCF) 5. An entity must account for its investments in jointly controlled entities after initial recognition using: a. either the cost model or the fair value model (using the same accounting policy for all investments in jointly controlled entities). b. either the cost model or the fair value model (model can be elected on an investment-by-investment basis). c. either the cost model, the equity method or the fair value model (using the same accounting policy for all investments in jointly controlled entities). d. either the cost model, the equity method or the fair value model (model can be elected on an investment-byinvestment basis). 6. Investments in jointly controlled entities must be tested fo impairment in accordance with Section 27 Impairment of Assets (of PFRS for SMEs), if the entity uses: a. the cost model, equity method or fair value model. b. the cost model or the equity method. c. the cost model or the fair value model. d. the equity method or the fair value model. (IASCF) 7. On 31 December 201 entity A acquired 30 per cent of the ordinary shares that carry voting rights of entity Z for P100,000. In acquiring those shares entity A incurred transaction costs of P1,000. Entity A has entered into contractual arrangement with another party (entity C) that owns 25 per cent of the ordinary shares of entity Z, whereby entities A and C jointly control entity Z. Entity A uses the cost model to account for its investments in jointly controlled entities. A published price quotation does not exist for entity Z. In January 202, entity Z declared and paid a dividend of P20,000 out of profits earned in 201. No further dividends were paid in 202,203 or 204. At 31 December 201,202 and 203, in accordance with Section 27 Impairment of Asses, management assessed the fair values of its investment in entity Z as P102,000,P110,000 and P90,000 respectively. Cost to sell are estimated at P4,000 throughout. Entity A measure its investment in entity Z on 31 December 201,202 and 203 respectively at: a. P100,000,P100,000,P100,000 d. P98,000, P101,000, P86,000. b. P95,000, P95,000, P86,000. e. P102,000, P110,000, P90,000. c. P98,000, P106,000, P86,000. f. P101,000, P101,000, P101,00 (IASCF) 8. The facts are the same as in the immediately precedint question. However, in this scenario, a published prial quotation exists for entity Z and entity A uses the fair valol model. Entity A measures its investment in entity Z on 3! December 201,202 and 203 respectively at: 9. An investor in a joint venture that does not have joint control accounts for its investment: a. in accordance with Section 11 Basic Financial Instruments. b. in accordance with Section 14 Investments in Associates. c. in accordance with Section 11 Basic Financial Instruments or, if it has significant influence in the joint venture, in accordance with Section 14 Investments in Associates. d. in accordance with Section 9 Consolidated and Separate Financial Statements. MSCF) 10. Which of the following statements is false? a. Joint control over an entity can be gained or lost without a change in absolute or relative ownership levels. b. In determining whether two or more entities jointly control another entity, the existence and effect of potential voting rights that they hold that are currently exercisable or convertible are considered. c. An entity considers the existence and effect of potential voting rights held by other parties that are currently exercisable or convertible when determining whether it together with its co-venturers jointly controls another entity. d. In determining whether an entity and its co-venturers jointly control another entity, only present ownership interests are considered. The possible exercise or conversions of potential voting rights are not considered