any answers will be rated immediately :)

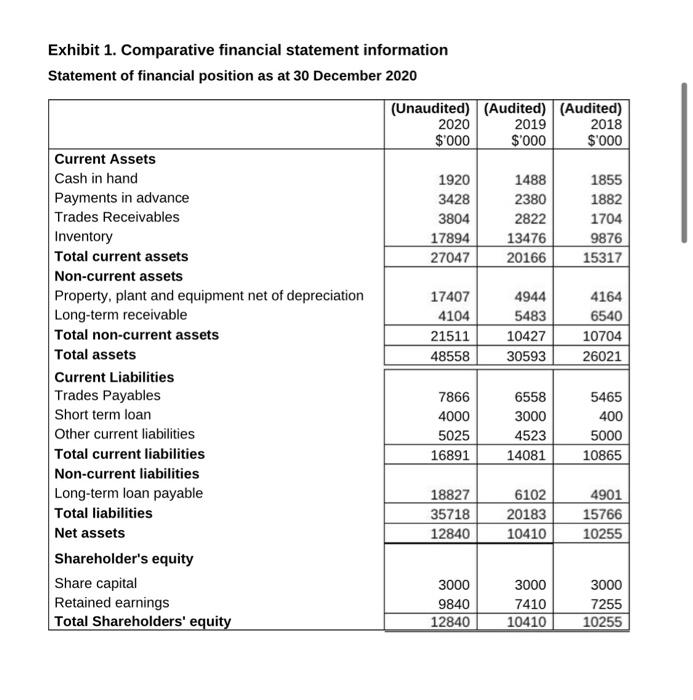

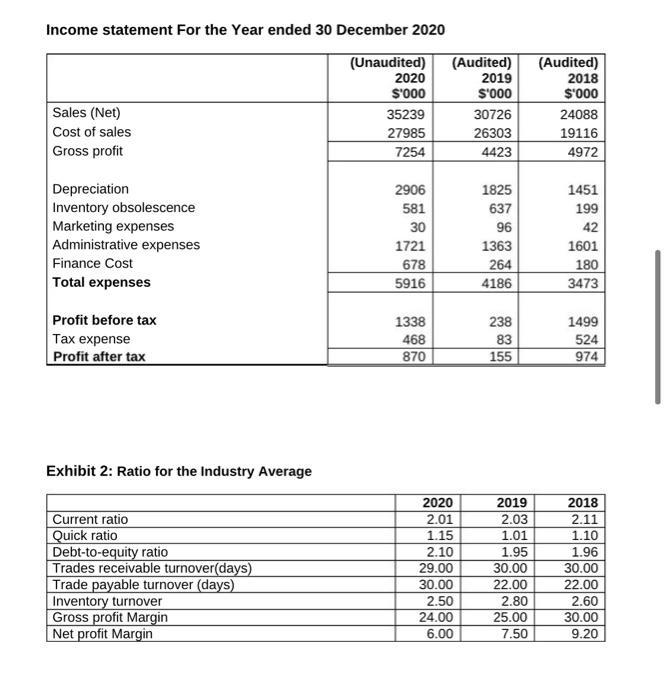

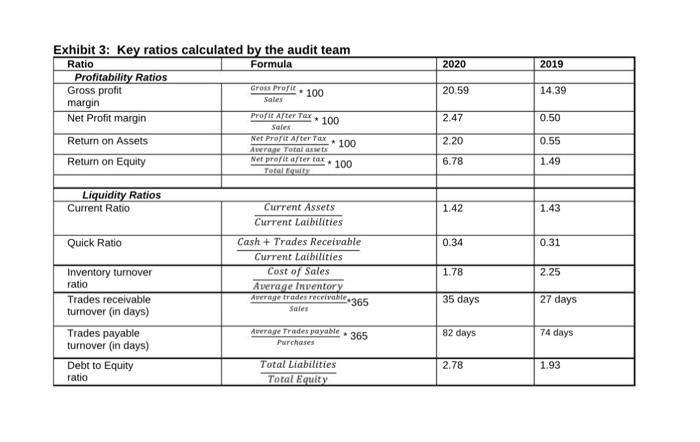

Case Study - Rice Company of Australia Ltd FKC is a mid-tier accounting firm based in Melbourne. In 2020, a new audit client, Rice Company of Australia Ltd (RCA), expressed its interest to work with FKC. RCA is a medium size company located in Melbourne. Josh Prakash, who is an audit partner at FKC, assessed FKC's independence as well as competence to audit RCA. Finally, Josh decided to accept this new client. Rebecca Cheng was assigned as the audit manager in charge of planning and supervising the conduct of the RCA audit. You are currently employed as an audit assistant and have been assigned to work on the RCA audit. You will be assisting Rebecca. RCA's background RCA's principal business activities include importing, grading, packing, and selling rice (i.e.. rice is a common food for many households across the world). RCA focuses on the Australian market and South Pacific markets such as Fiji, Vanuatu, Solomon Islands, etc. RCA was founded in 1982 and has developed a highly efficient processing line using fully automated machinery. It has installed a state-of-the-art rice sorter in the processing line to remove any foreign particles and unwanted components such as rice husks. The reputation of focusing on quality gives RCA its competitive edge. RCA has various types of rice that cover most preferences in the market: Australian Calrose medium grain rice, Australian long grain rice, long grain rice imported from Vietnam, fragrant Jasmine rice imported from Thailand, and Basmati rice imported from India and Pakistan. Before sorting and packaging both the imported and locally grown rice into various package sizes, the raw material (pre-processed rice) is stored in a series of side by side silos. These silos can hold up to 1000 tonnes of grain each. The raw material inventory represents a significant portion of the total inventory. The different types of rice are then put through the sorting and packaging process and stored in the company's warehouse in Melbourne before shipping to customers. Forecast Financial Statements You have been given the unaudited financial statements for the year ending 31st December 2020, as well as the previous two years' audited results (Exhibit 1), ratio for the industry average (Exhibit 2), and key ratios calculated by the audit team (Exhibit 3). Exhibit 1. Comparative financial statement information Statement of financial position as at 30 December 2020 (Unaudited) (Audited) (Audited) 2020 2019 2018 $'000 $'000 $'000 Current Assets Cash in hand 1920 1488 1855 Payments in advance 3428 2380 1882 Trades Receivables 3804 2822 1704 Inventory 17894 13476 9876 Total current assets 27047 20166 15317 Non-current assets Property, plant and equipment net of depreciation 17407 4944 4164 Long-term receivable 4104 5483 6540 Total non-current assets 21511 10427 10704 Total assets 48558 30593 26021 Current Liabilities Trades Payables 7866 6558 5465 Short term loan 4000 3000 400 Other current liabilities 5025 4523 5000 Total current liabilities 16891 14081 10865 Non-current liabilities Long-term loan payable 18827 6102 4901 Total liabilities 35718 20183 15766 Net assets 12840 10410 10255 Shareholder's equity Share capital 3000 3000 3000 Retained earnings 9840 7410 7255 Total Shareholders' equity 12840 10410 10255 Income statement for the Year ended 30 December 2020 Sales (Net) Cost of sales Gross profit (Unaudited) 2020 S'000 35239 27985 7254 (Audited) 2019 S'000 30726 26303 4423 (Audited) 2018 $'000 24088 19116 4972 2906 581 Depreciation Inventory obsolescence Marketing expenses Administrative expenses Finance Cost Total expenses 30 1721 678 5916 1825 637 96 1363 264 4186 1451 199 42 1601 180 3473 Profit before tax Tax expense Profit after tax 1338 468 238 83 155 1499 524 974 870 Exhibit 2: Ratio for the Industry Average Current ratio Quick ratio Debt-to-equity ratio Trades receivable turnover(days) Trade payable turnover (days) Inventory turnover Gross profit Margin Net profit Margin 2020 2.01 1.15 2.10 29.00 30.00 2.50 24.00 6.00 2019 2.03 1.01 1.95 30.00 22.00 2.80 25.00 7.50 2018 2.11 1.10 1.96 30.00 22.00 2.60 30.00 9.20 2020 2019 20.59 14.39 Exhibit 3: Key ratios calculated by the audit team Ratio Formula Profitability Ratios Gross profit Gross Profit 100 Sales margin Net Profit margin Sales Return on Assets Net Propie After Tax * 100 ART Total Return on Equity Net profit after tax * 100 Totally Profit After Tur. 100 2.47 0.50 2.20 0.55 6.78 1.49 Liquidity Ratios Current Ratio 1.42 1.43 Current Assets Current Laibilities Quick Ratio 0.34 0.31 Cash + Trades Receivable Current Laibilities Cost of Sales Average Inventory Average trades receivable 365 Sales 1.78 2.25 35 days 27 days Inventory turnover ratio Trades receivable turnover (in days) Trades payable turnover (in days) Debt to Equity ratio Average Trades payable Purchases 365 82 days 74 days 2.78 1.93 Total Liabilities Total Equity Additional Information 1. RCA has local and overseas customers as stated above. For the Australian market, all the sales are made in bulk to major supermarkets (like Coles and Woolworths) or to various Asian grocery stores. For international sales, they represent a significant proportion of total sales, most of the customers are the supermarket chains in the relevant island nation. The sales to the local market are in Australian dollars while the sales to the international market are in US dollars. Some of the increased sales in 2020 could be attributed to panic buying of customers in supermarkets which forced the supermarkets to increase their orders from RCA. The sales in final quarter of 2020 was more subdued. Revenue is recognized as soon as the sale is made for the local customers. For the international market, the ownership of the goods remain with RCA until the shipment is delivered to the customer. The revenue is recognized by RCA once the goods are delivered to these customers. Due to COVID-19 pandemic travel restrictions, the delivery of goods to the Pacific island customers can take more than a month. All raw material imported from overseas is paid in US dollars. The transfer of ownership from the overseas suppliers to the client varies with the contract that RCA has with the supplier 2. RCA has taken out one significantly large long-term loan from Commonwealth Bank. The loan agreement puts certain restrictions on further borrowing possibilities of RCA. It also requires RCA to submit its audited financial statements to Commonwealth Bank by April 30 of every year until the loan is fully paid. 3. The short-term loan is due to be paid shortly. RCA is in negotiation with the bank to refinance the short-term loan and its board of directors has indicated that their strong preference is to raise additional funds from the shareholders. 4. RCA has a board of directors comprising of five members. The company also has an audit committee that consists of a chair who is an independent director, the chief executive officer and a non-independent director. 5. Some countries from which RCA imports the raw material from have imposed strict limitation on the exports to other countries due to limited supplies in their own countries because of COVID-19 pandemic. In addition, RCA is also dealing with limited supply from the local rice growers due to bush fires and drought during last summer. These factors have pushed the price of unprocessed rice. Some of the suppliers have also indicated that future orders would require RCA to make payments in advance to secure the supply. The company anticipates that 2021 will be a better year for rice growers in Australia as more rain is expected. However, the rice price from the overseas suppliers is expected to remain high in the near future. 6. Due to the current economic climate, the audit client expects the demand for rice to decline due to falling income levels in the various Pacific island nations. There is evidence that the consumers in some of these countries are switching to more traditional root crops. The demand from the Australian consumers is expected to remain stable. Required: 1. ASA 315 requires auditors to understand the client for the purpose of assessing the risk of material misstatements in financial reports. Based on the provided information in this case, please write down two to three major inherent risks, and explain why you believe they are inherent risks. 2. Based on the inherent risks you identified, write down internal controls that you would expect management to implement. 3. Conduct the analytical review with key financial ratios and a. identify the key financial ratios or financial accounts that audit team should pay greater attention to. Explain why. b. Based on your risk assessment identify one account that has a high risk of material misstatement. For the chosen account, identify the key assertion that would be at risk. 4. The management is responsible for preparation of the financial statements. They make an assessment regarding going concern when preparing the statements. For the year ending 31st December 2020, RCA's management has prepared the financial statements on this basis. a. Explain what role the auditor has regarding the going concern assumption made by management b. Based on the information provided and the analytical review carried out by you in question 3, state if there are any indicators of going concern problem. c. If there are indicators of going concern issue, identify any mitigating factors