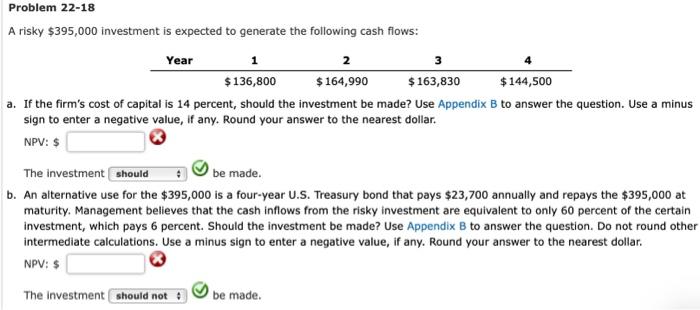

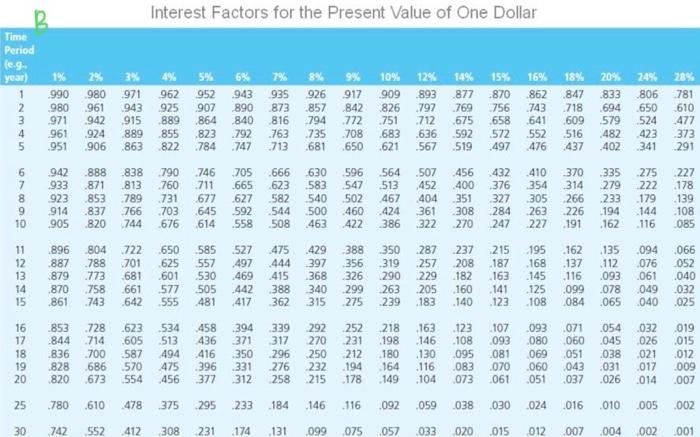

A risky $395,000 investment is expected to generate the following cash flows: a. If the firm's cost of capital is 14 percent, should the investment be made? Use Appendix B to answer the question. Use a minus sign to enter a negative value, if any. Round your answer to the nearest dollar. NPV: $ The investment be made. b. An alternative use for the $395,000 is a four-year U.S. Treasury bond that pays $23,700 annually and repays the $395,000 at maturity. Management believes that the cash inflows from the risky investment are equivalent to only 60 percent of the certain investment, which pays 6 percent. Should the investment be made? Use Appendix B to answer the question. Do not round other intermediate calculations. Use a minus sign to enter a negative value, if any. Round your answer to the nearest dollar. NPV: $ The investment be made. \begin{tabular}{|c|c|c|c|c|c|c|c|c|c|c|c|c|c|c|c|c|c|c|} \hline \begin{tabular}{l} Time \\ Period \\ (eg. \\ year) \end{tabular} & 1% & 2% & 3% & 4% & 5% & 6% & 7% & 8% & 9% & 10% & 12% & 14% & 15% & 16% & 18% & 20% & & 28% \\ \hline 1 & .990 & .980 & 971 & 962 & 952 & .943 & .935 & 926 & 917 & .909 & .893 & 877 & .870 & .862 & .847 & .833 & .806 & .781 \\ \hline 2 & .980 & .961 & 943 & 925 & 907 & 890 & 873 & 857 & 842 & 826 & .797 & .769 & .756 & .743 & 718 & 694 & .650 & .610 \\ \hline 3 & 971 & .942 & .915 & 889 & .864 & 840 & 816 & 794 & .772 & .751 & .712 & .675 & .658 & .641 & .609 & .579 & .524 & .477 \\ \hline 4 & .961 & .924 & 889 & .855 & 823 & .792 & .763 & .735 & .708 & 683 & .636 & .592 & 572 & .552 & .516 & .482 & .423 & .373 \\ \hline 5 & .951 & .906 & 863 & .822 & .784 & .747 & .713 & .681 & .650 & .621 & .567 & .519 & .497 & .476 & .437 & .402 & .341 & 291 \\ \hline 6 & .942 & 888 & 838 & .790 & .746 & 705 & .666 & 630 & 596 & .564 & 507 & 456 & 432 & 410 & 370 & 335 & 275 & .227 \\ \hline 7 & .933 & 871 & 813 & .760 & .711 & .665 & .623 & 583 & 547 & 513 & .452 & .400 & 376 & .354 & 314 & .279 & .222 & .178 \\ \hline 8 & 923 & .853 & .789 & .731 & 677 & .627 & 582 & .540 & .502 & .467 & .404 & .351 & 327 & 305 & 266 & .233 & .179 & .139 \\ \hline 9 & .914 & 837 & .766 & .703 & .645 & .592 & .544 & .500 & .460 & 424 & 361 & .308 & .284 & .263 & 226 & .194 & .144 & .108 \\ \hline 10 & .905 & .820 & .744 & .676 & .614 & .558 & .508 & .463 & .422 & 386 & .322 & .270 & 247 & .227 & .191 & .162 & .116 & .085 \\ \hline 11 & 896 & 804 & .722 & .650 & .585 & .527 & .475 & .429 & .388 & 350 & .287 & .237 & .215 & .195 & .162 & .135 & .094 & .066 \\ \hline 12 & .887 & 788 & .701 & .625 & .557 & .497 & .444 & 397 & .356 & .319 & .257 & .208 & .187 & .168 & .137 & .112 & .076 & .052 \\ \hline 13 & .879 & .773 & .681 & .601 & .530 & .469 & .415 & .368 & .326 & .290 & .229 & .182 & .163 & .145 & .116 & .093 & .061 & .040 \\ \hline 14 & .870 & .758 & .661 & 577 & .505 & .442 & .388 & 340 & 299 & 263 & .205 & .160 & .141 & .125 & .099 & .078 & .049 & .032 \\ \hline 15 & 861 & .743 & .642 & .555 & .481 & .417 & .362 & 315 & .275 & 239 & .183 & .140 & .123 & .108 & .084 & .065 & .040 & .025 \\ \hline 16 & .853 & .728 & 623 & .53 & .458 & .394 & .33 & 29 & .25 & 2 & .16 & .12 & .107 & .093 & .071 & .054 & .032 & .019 \\ \hline 17 & 844 & 714 & .605 & .513 & .436 & 371 & 317 & 270 & 231 & .198 & .146 & .108 & .093 & .080 & .060 & .045 & .026 & .015 \\ \hline 18 & .836 & 700 & .587 & .494 & .416 & .350 & .296 & .250 & 212 & .180 & .130 & .095 & .081 & .069 & .051 & .038 & .021 & .012 \\ \hline 19 & .828 & .686 & .570 & .475 & .396 & .331 & .276 & .232 & 194 & .164 & .11 & .083 & .070 & .060 & .043 & .031 & .017 & .009 \\ \hline 20 & 820 & .673 & .554 & .456 & 377 & 312 & .258 & 215 & .178 & .149 & .104 & .073 & .061 & .051 & .037 & .026 & .014 & .007 \\ \hline 25 & .780 & .610 & 478 & .375 & .295 & .233 & .184 & .146 & .116 & .092 & .059 & .038 & .030 & .024 & .016 & .010 & .005 & .002 \\ \hline 30 & .742 & 552 & 412 & 308 & .231 & .174 & .131 & .099 & .075 & .057 & .033 & .020 & .015 & .012 & .007 & .004 & .002 & .001 \\ \hline \end{tabular}