Question

Appendix D Differences Between U.S. GAAP and IFRS Standards While much of the presentation guidance in U.S. GAAP is similar to that in IFRS Standards,

Appendix D Differences Between U.S. GAAP and IFRS Standards While much of the presentation guidance in U.S. GAAP is similar to that in IFRS Standards, there are key differences. The table below summarizes these differences. Subject U.S. GAAP IFRS Standards Scope Although all entities are required to present a statement of cash flows, there are certain exceptions. Entities that are not required to present a statement of cash flows include defined benefit pension plans that prepare financial information in accordance with ASC 960, certain investment companies within the scope of ASC 946 that meet all of the conditions in ASC 230-10-15-4(c), and certain funds described in ASC 230-10- 15-4(b)(3). Under paragraph 7 of IAS 7, all entities are required to present a statement of cash flows (i.e., there are no scope exceptions). Comparative periods Under ASC 230, presentation of comparative periods is not required. However, SEC Regulation S-X, Rule 3-02, requires that an audited cash flow statement be presented for the previous three fiscal years. Under paragraph 36 of IAS 7, the most recent two years must be presented. Under the general requirements of paragraphs 38 and 38A of IAS 1, comparative information related to the preceding period should be presented for all amounts reported in the currentperiod statement of cash flows and the supporting notes. Consequently, an entity should present, at a minimum, two statements of cash flows. Definitions of cash and cash equivalents The definitions of cash and cash equivalents in ASC 230-10-20 include cash and short-term, highly liquid investments. However, bank overdrafts are excluded from these definitions. An entitys statement of cash flows must explain the change during the period in the total of cash, cash equivalents, and amounts generally described as restricted cash or restricted cash equivalents (emphasis added). The definitions of cash and cash equivalents in paragraph 6 of IAS 7 include cash and short-term, highly liquid investments. Bank overdrafts may be included in these definitions in certain situations (i.e., if they are an integral part of an entitys cash management). An entity that classifies bank overdrafts as cash and cash equivalents will need to disclose this policy. 118 Deloitte | A Roadmap to the Preparation of the Statement of Cash Flows (2019) (Table continued) Subject U.S. GAAP IFRS Standards Classification in the statement of cash flows ASC 230-10-45-10 requires that cash flows be classified and presented in one of three categories: operating, investing, or financing. ASC 230 provides more specific guidance than IFRS Standards on items to be included in each category. Paragraph 10 of IAS 7, requires that cash flows be classified and presented in one of three categories: operating, investing, or financing. IAS 7 is more flexible than U.S. GAAP regarding which items are to be included in each category. Method of reporting cash flows from operating activities Under ASC 230-10-45-25, use of the direct or indirect method is allowed. Under both methods, net income must be reconciled to net cash flows from operating activities. Under paragraph 18 of IAS 7, use of the direct or indirect method is allowed. Net income must be reconciled to net cash flows from operating activities only under the indirect method. Presentation of components of transactions with characteristics of more than one category of cash flows Under ASC 230-10-45-22, ASC 230-10- 45-22A, and ASC 230-10-45-23, an entity will first need to determine whether there are separately identifiable cash flows. If so, such cash flows are presented on the basis of their nature. In the absence of separately identifiable cash flows, an entity would present such cash flows collectively on the basis of the predominant source or use of the cash flows. Paragraph 12 of IAS 7 requires that individual components of a single transaction be classified separately as operating, investing, or financing activities. Disclosure of cash flows pertaining to discontinued operations An entity must disclose either of the following if it is not already presented on the face of the cash flows statement: The total operating and investing cash flows of the discontinued operation. The depreciation, amortization, capital expenditures, and significant operating and investing noncash items of the discontinued operation. In accordance with paragraph 33(c) of IFRS 5, disclosure of cash flows from discontinued operations under each category is required either on the face of the cash flow statement or in the notes. Presentation of cash flow per share on the face of the financial statements ASC 230-10-45-3 prohibits an entity from reporting cash flow per share. Under IFRS Standards (including IAS 7, which does not mention this metric), disclosure of cash flow per share is not explicitly prohibited. Cash flows from hedging instruments A company may classify cash flows from hedging activities in the same category as the cash flows from the hedged item provided that the requirements in ASC 230-10-45-27 are met (i.e., regarding the financing element at inception and disclosure of the accounting policy). Paragraph 16 of IAS 7 requires entities to classify cash flows from hedging activities in the same category as the cash flows from the item being hedged. 119 Appendix D Differences Between U.S. GAAP and IFRS Standards (Table continued) Subject U.S. GAAP IFRS Standards Taxes paid Under ASC 230-10-45-25, taxes paid are classified as operating activities. Under paragraph 14(f) of IAS 7, taxes paid are classified as operating activities unless they can be specifically identified within financing and investing activities. Interest and dividends paid and received Under ASC 230, interest paid and received is classified as operating activities. Dividends received are classified as operating activities because these are generally considered to be returns on an entitys investment. However, a dividend from an equity method investment may be investing if the distribution is a return of investment. That is, for distributions from equity method investments, an entity is required to determine whether the distribution is a return on or a return of the entitys investment. See Section 6.1.4 for specific guidance on distributions from equity method investments. Dividends paid are classified as financing activities. Under IAS 7, entities may present interest paid as either operating or financing activities. In addition, entities may present interest and dividends received as either operating or investing activities. Note that IAS 7 does not include a requirement to determine whether a distribution from an equity method investment is a return on, or a return of, the entitys investment. Settlement of zerocoupon debt instruments or other debt instruments that are insignificant in relation to the effective interest rate of the borrowing As bonds are accreted from issuance to maturity, the interest expense is presented as a reconciling item between net income and cash flows from operating activities. At redemption, the cash paid to settle the interest component is classified as an operating activity and the cash paid to settle the principal is classified as a financing activity. See Sections 6.4.2 and 6.4.3. Rather than including specific guidance as is done in U.S. GAAP, IFRS Standards include principles related to assessing the classification of the cash flows as operating, investing, or financing activities. Contingent consideration payments made after the date of a business combination Contingent consideration payments that are not made soon after the acquisition date must be classified as financing activities; any excess cash payments will be classified as operating activities. Cash payments made soon after the acquisition date in a business combination transaction must be classified as investing activities (see Section 7.5.4.1). IFRS Standards do not provide guidance similar to that in U.S. GAAP (under U.S. GAAP, such guidance is based on when contingent consideration payments are made in relation to the date of a business combination). Instead, an entity should assess the nature of the transaction on the basis of the general principle of classification of the cash flows as operating or financing activities. Proceeds from the settlement of insurance claims Proceeds from the settlement of insurance claims should generally be classified on the basis of the nature of the loss (see Section 6.3.2). Rather than including specific guidance as is done in U.S. GAAP, IFRS Standards include principles related to assessing the classification of the cash flows as operating, investing, or financing activities. 120 Deloitte | A Roadmap to the Preparation of the Statement of Cash Flows (2019) (Table continued) Subject U.S. GAAP IFRS Standards Proceeds from the settlement of companyowned or bank-owned life insurance policies ASC 230-10-45-21C indicates that proceeds from the settlement of company-owned or bank-owned life insurance policies should be classified as investing activities (see Section 6.1.7). Rather than including specific guidance as is done in U.S. GAAP, IFRS Standards include principles related to assessing the classification of the cash flows as operating, investing, or financing activities. Beneficial interests in a securitization transaction For U.S. GAAP guidance, see Sections 7.9 and 7.9.1. Rather than including specific guidance as is done in U.S. GAAP, IFRS Standards include principles related to assessing the classification of the cash flows as operating, investing, or financing activities. Income tax effects of share-based payment awards Excess tax benefits or tax deficiencies represent operating activities (see Section 7.3.2). IFRS Standards do not include explicit guidance on classifying excess tax benefits related to share-based payment awards. Remittances of minimum statutory withholding on share-based payment awards For U.S. GAAP guidance, see Section 7.3.6. IAS 7 does not specify how an entity should classify cash that an employer pays to tax authorities when the entity repurchases shares from the employee to satisfy the entitys tax withholding obligation. An entity should assess the nature of the cash flows as operating or financing, as well as the applicable noncash activity disclosures. Leases After the adoption of ASC 842, a lessee should present payments associated with operating leases as an operating activity in the statement of cash flows. A lessee should present payments associated with finance leases in the statement of cash flows as (1) a financing activity, for the principal portion of the payment, and (2) an operating activity, for the interest portion of the payment. See Section 7.6.1. Under IFRS 16, a lessee is required to use a single approach (similar to the FASBs finance lease approach) to subsequently account for the ROU asset. For this reason, the lessee should present payments associated with its leases in the statement of cash flows as (1) a financing activity, for the principal portion of the payment in accordance with IAS 7.17(e), and (2) interest as either a financing or an operating activity in the statement of cash flows, depending on the lessees accounting policy election under IAS 7.1 1 Paragraph 33 of IAS 7 acknowledges that there is no consensus on the classification of interest paid and that an e

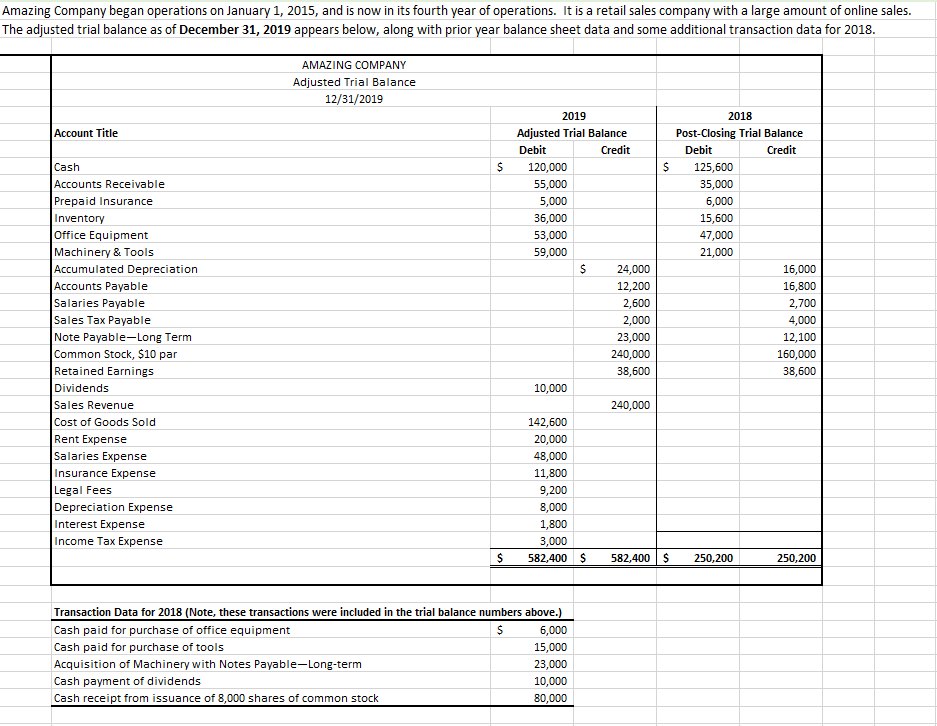

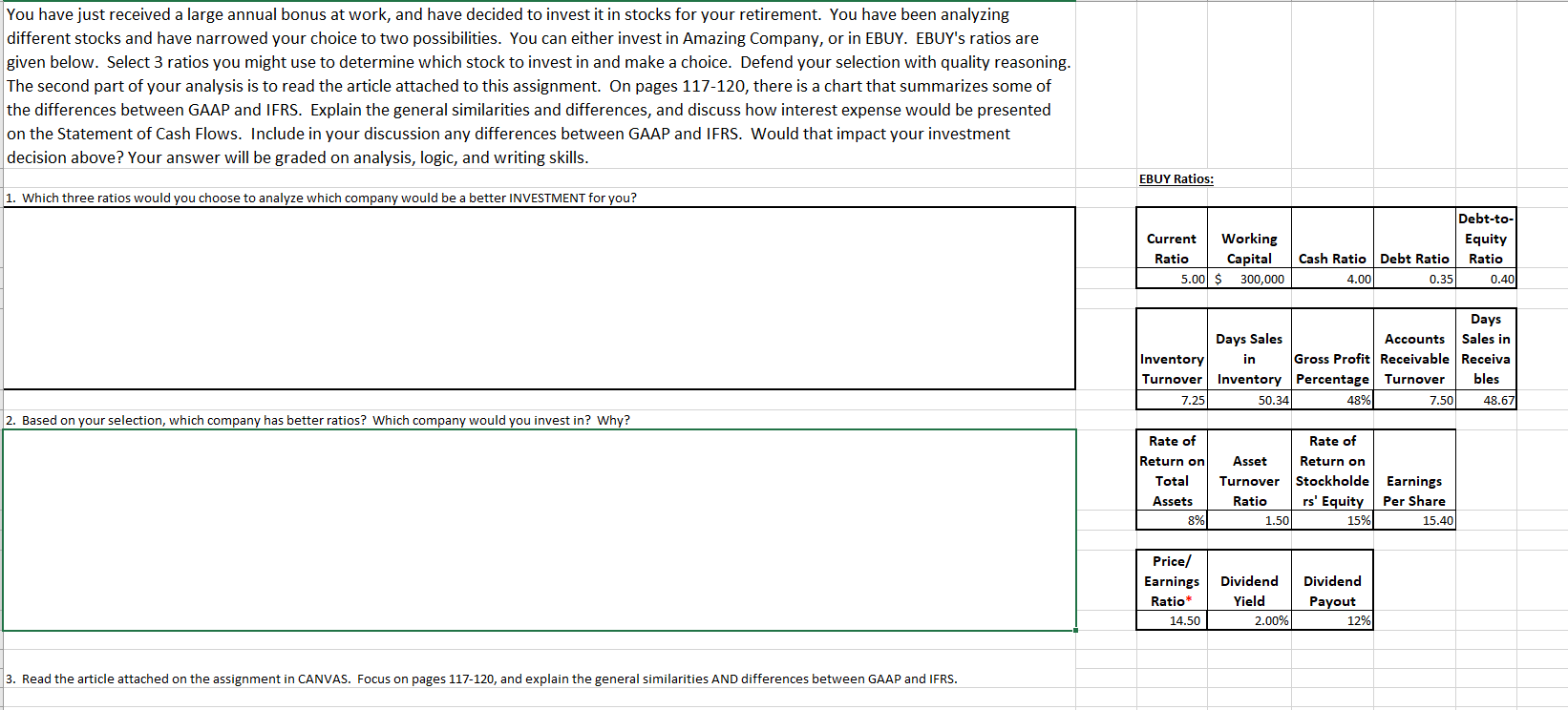

Amazing Company began operations on January 1, 2015, and is now in its fourth year of operations. It is a retail sales company with a large amount of online sales. The adjusted trial balance as of December 31, 2019 appears below, along with prior year balance sheet data and some additional transaction data for 2018. AMAZING COMPANY Adjusted Trial Balance 12/31/2019 Account Title $ Cash Accounts Receivable Prepaid Insurance Inventory Office Equipment Machinery & Tools Accumulated Depreciation Accounts Payable Salaries Payable Sales Tax Payable Note Payable-Long Term Common Stock, $10 par Retained Earnings Dividends Sales Revenue Cost of Goods Sold Rent Expense Salaries Expense Insurance Expense Legal Fees Depreciation Expense Interest Expense Income Tax Expense 2019 Adjusted Trial Balance Debit Credit 120,000 $ 55,000 5,000 36,000 53,000 59,000 $ 24,000 12,200 2,600 2,000 23,000 240,000 38,600 10,000 240,000 142,600 20,000 48,000 11,800 9,200 8,000 1,800 3,000 582,400 $ 582,400$ 2018 Post-Closing Trial Balance Debit Credit 125,600 35,000 6,000 15,600 47,000 21,000 16,000 16,800 2,700 4,000 12,100 160,000 38,600 $ 250,200 250,200 Transaction Data for 2018 (Note, these transactions were included in the trial balance numbers above.) Cash paid for purchase of office equipment $ 6,000 Cash paid for purchase of tools 15,000 Acquisition of Machinery with Notes Payable-Long-term 23,000 Cash payment of dividends 10,000 Cash receipt from issuance of 8,000 shares of common stock 80,000 You have just received a large annual bonus at work, and have decided to invest it in stocks for your retirement. You have been analyzing different stocks and have narrowed your choice to two possibilities. You can either invest in Amazing Company, or in EBUY. EBUY's ratios are given below. Select 3 ratios you might use to determine which stock to invest in and make a choice. Defend your selection with quality reasoning. The second part of your analysis is to read the article attached to this assignment. On pages 117-120, there is a chart that summarizes some of the differences between GAAP and IFRS. Explain the general similarities and differences, and discuss how interest expense would be presented on the Statement of Cash Flows. Include in your discussion any differences between GAAP and IFRS. Would that impact your investment decision above? Your answer will be graded on analysis, logic, and writing skills. EBUY Ratios: 1. Which three ratios would you choose to analyze which company would be a better INVESTMENT for you? Current Working Ratio Capital 5.00 $ 300,000 Debt-to- Equity Cash Ratio Debt Ratio Ratio 4.00 0.35 0.40 Inventory Turnover 7.25 Days Days Sales Accounts Sales in in Gross Profit Receivable Receiva Inventory Percentage Turnover bles 50.34 48% 7.50 48.67 2. Based on your selection, which company has better ratios? Which company would you invest in? Why? Rate of Return on Total Assets 8% Rate of Asset Return on Turnover Stockholde Earnings Ratio rs' Equity Per Share 1.50 15% 15.40 Price/ Earnings Ratio* 14.50 Dividend Yield 2.00% Dividend Payout 12% 3. Read the article attached on the assignment in CANVAS. Focus on pages 117-120, and explain the general similarities AND differences between GAAP and IFRS. Amazing Company began operations on January 1, 2015, and is now in its fourth year of operations. It is a retail sales company with a large amount of online sales. The adjusted trial balance as of December 31, 2019 appears below, along with prior year balance sheet data and some additional transaction data for 2018. AMAZING COMPANY Adjusted Trial Balance 12/31/2019 Account Title $ Cash Accounts Receivable Prepaid Insurance Inventory Office Equipment Machinery & Tools Accumulated Depreciation Accounts Payable Salaries Payable Sales Tax Payable Note Payable-Long Term Common Stock, $10 par Retained Earnings Dividends Sales Revenue Cost of Goods Sold Rent Expense Salaries Expense Insurance Expense Legal Fees Depreciation Expense Interest Expense Income Tax Expense 2019 Adjusted Trial Balance Debit Credit 120,000 $ 55,000 5,000 36,000 53,000 59,000 $ 24,000 12,200 2,600 2,000 23,000 240,000 38,600 10,000 240,000 142,600 20,000 48,000 11,800 9,200 8,000 1,800 3,000 582,400 $ 582,400$ 2018 Post-Closing Trial Balance Debit Credit 125,600 35,000 6,000 15,600 47,000 21,000 16,000 16,800 2,700 4,000 12,100 160,000 38,600 $ 250,200 250,200 Transaction Data for 2018 (Note, these transactions were included in the trial balance numbers above.) Cash paid for purchase of office equipment $ 6,000 Cash paid for purchase of tools 15,000 Acquisition of Machinery with Notes Payable-Long-term 23,000 Cash payment of dividends 10,000 Cash receipt from issuance of 8,000 shares of common stock 80,000 You have just received a large annual bonus at work, and have decided to invest it in stocks for your retirement. You have been analyzing different stocks and have narrowed your choice to two possibilities. You can either invest in Amazing Company, or in EBUY. EBUY's ratios are given below. Select 3 ratios you might use to determine which stock to invest in and make a choice. Defend your selection with quality reasoning. The second part of your analysis is to read the article attached to this assignment. On pages 117-120, there is a chart that summarizes some of the differences between GAAP and IFRS. Explain the general similarities and differences, and discuss how interest expense would be presented on the Statement of Cash Flows. Include in your discussion any differences between GAAP and IFRS. Would that impact your investment decision above? Your answer will be graded on analysis, logic, and writing skills. EBUY Ratios: 1. Which three ratios would you choose to analyze which company would be a better INVESTMENT for you? Current Working Ratio Capital 5.00 $ 300,000 Debt-to- Equity Cash Ratio Debt Ratio Ratio 4.00 0.35 0.40 Inventory Turnover 7.25 Days Days Sales Accounts Sales in in Gross Profit Receivable Receiva Inventory Percentage Turnover bles 50.34 48% 7.50 48.67 2. Based on your selection, which company has better ratios? Which company would you invest in? Why? Rate of Return on Total Assets 8% Rate of Asset Return on Turnover Stockholde Earnings Ratio rs' Equity Per Share 1.50 15% 15.40 Price/ Earnings Ratio* 14.50 Dividend Yield 2.00% Dividend Payout 12% 3. Read the article attached on the assignment in CANVAS. Focus on pages 117-120, and explain the general similarities AND differences between GAAP and IFRSStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Tips For The New Auditor

Authors: Marty Sturino

1st Edition

1733097813, 978-1733097819