Question: Apple Pay Will Apple pay be a huge success with consumers? Why or why not Why did banks agree to partner with apply for apple

Apple Pay

- Will Apple pay be a huge success with consumers? Why or why not

- Why did banks agree to partner with apply for apple pay in the US?

- Are retailers excited about Apply pay? Why or why not?

- What is Apple Pay's motivation in Launching Apple pay?

- Should Apple make any changes to its Apple pay roll out plan?

1

![to replace this [wallet] and we are going to start with payments."](https://dsd5zvtm8ll6.cloudfront.net/si.experts.images/questions/2024/09/66e4398c89ac4_97266e4398c46fe3.jpg)

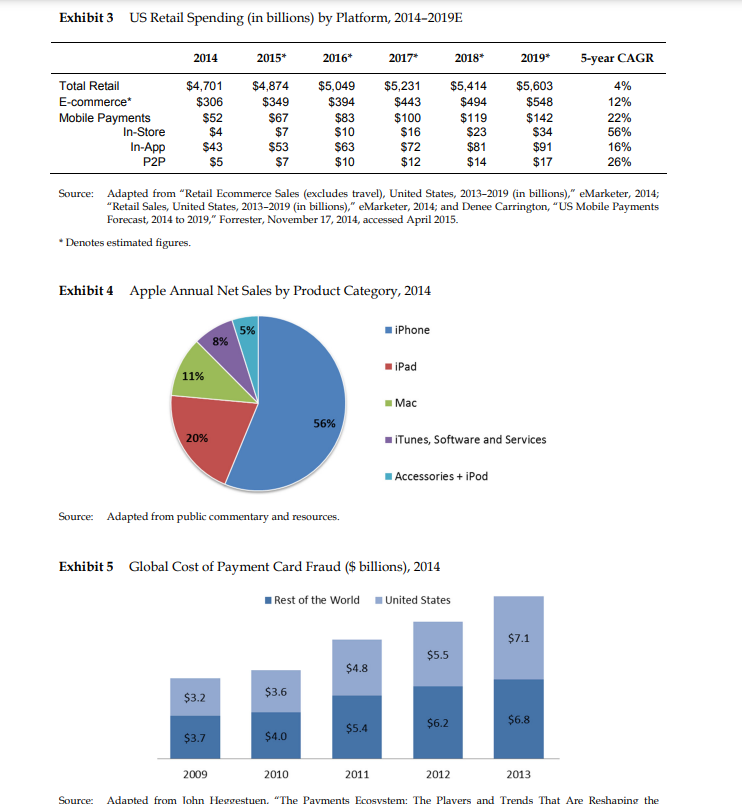

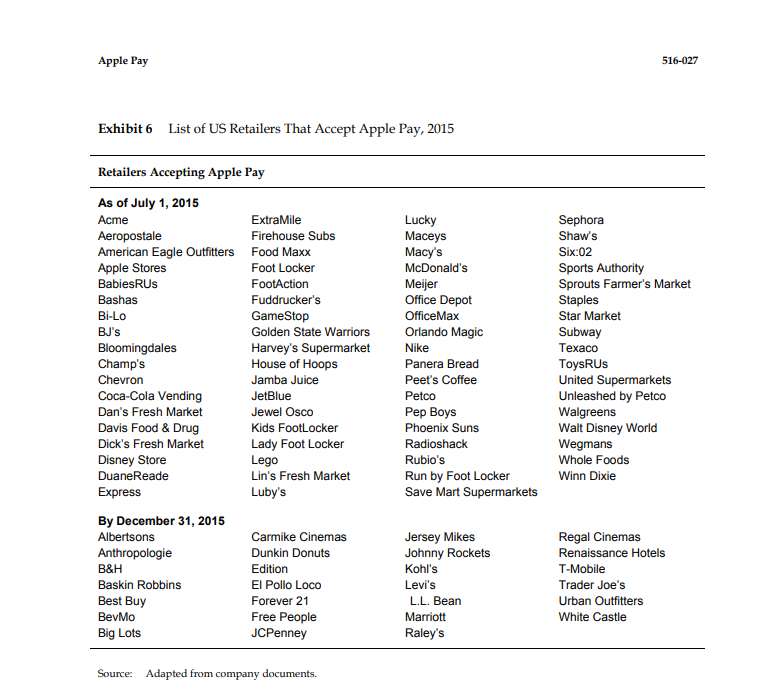

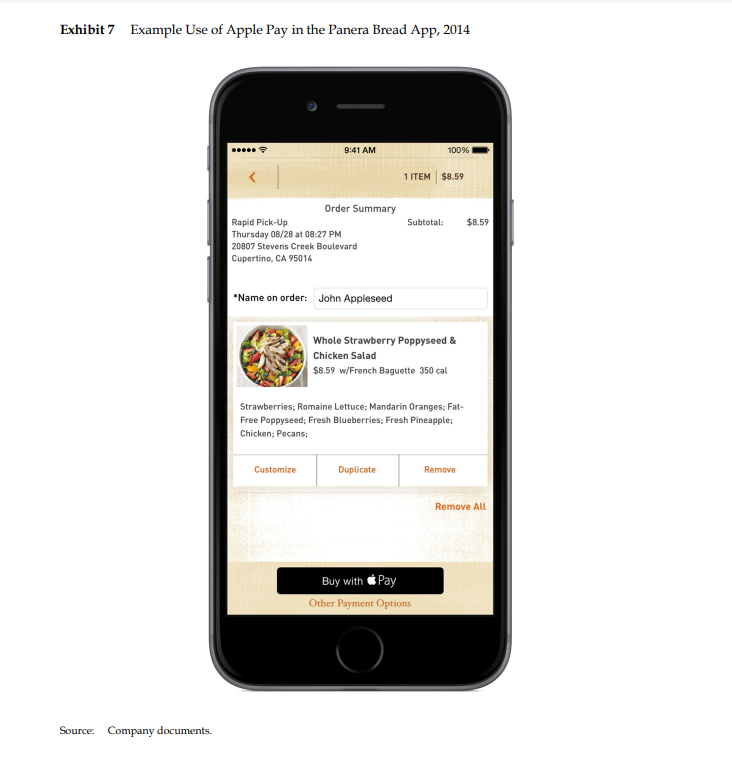

Apple Pay Apple Pay will forever change the way all of us buy things. - Tim Cook, Chief Executive of Apple On September 9, 2014, in front of a packed audience in Cupertino, CA, Tim Cook, the Chief Executive Officer of Apple, announced the much anticipated launch of Apple Pay: "Our vision is to replace this [wallet] and we are going to start with payments." He continued, "Payments are a huge business. Every day between credit and debit, we spend $12 billion in the U.S., and this business is comprised of over 200 million transactions a day."2 Cook then invited Eddy Cue, Apple's Senior Vice President of Internet Software and Services, to the stage to explain how Apple Pay would transform the mobile payments industry. "Over $1 billion a day is spent on online purchasing," said Cue. "That's five million daily transactions just in the U.S. alone, and the process is really cumbersome. You've got these long forms to fill out for each and every app that you shop in." He went on to explain how Apple Pay would allow consumers to complete the checkout process within apps with a single touch, and without the need to repeatedly enter their credit card information, billing address, or shipping address. On October 20, 2014, US consumers could start using Apple Pay in stores with their iPhone 6 or iPhone 6 Plus (and, later, Apple Watch) and within apps using iPhone 6, iPhone 6 Plus, iPad Air 2, and iPad mini 3. All three major payment networks (American Express, MasterCard, and Visa) and 220,000 retail outlets in the US accepted Apple Pay at its launch-and more than 500 banks signed on to bring Apple Pay to their customers. Within a month, Whole Foods reported more than 150,000 Apple Pay transactions, and Mcdonald's processed half of its mobile transactions via Apple Pay.3 By March 2015, Apple Pay was accepted in 700,000 retail locations, including Coca-cola vending machines. "We are the fastest-adopted mobile payment service by a long shot," noted Jennifer Bailey, Vice President of Apple Pay. However, Cue and Bailey were aware that the landscape of mobile wallets and payment services was littered with failures. In 2011, Google introduced Google Wallet and invested hundreds of millions of dollars with limited success. Softcard, originally known as Isis, was formed as a joint venture between Verizon, AT&T, and T-Mobile, but it struggled to gain traction and was sold todifferences in the design of the survey questions and differences in sampling. In November 2:114. a survey conducted during the \"Black Friday\" shopping holiday found that a little over 9'35 of iP'hone IE and 6 Plus users had tried Apple Pay, and only about half of them used Apple Pay regularly.\" The survey was conducted again four months later, when the trial rate increased to 15%; but regular users remained less than half of those who tried it.\" Another survey conducted in April 21315 found self-reported use of Apple Pay to be far higher, with 56% of iPhone users claiming to have activated Apple Pay and 58%- of iPhone users claiming to have used Apple Pay at least oncel' This survey also noted that 68%- of respondents who had used Apple Pay in stores had encountered some problems during purchase.\" The most common problem was the P05 terminal taking too much time to record the transaction, followed by store-s claiming not to accept Apple Pay even though the retailer allegedly supported the service. Over one-third of respondents also cited issues with employees not knowing how to accept payment via a mobile wallet or errors in how the sale posted. Some observers were skeptical about the added value of Apple Pay beyond the credit card. \"The problem Apple tells us it's solving is the horrendously time consuming. arduous task of paying with these antiquated pieces of plastic.\" said David S. Evans, economist and founder of Market Platform Dynamics. "Paying with a card is so fast and convenient that it is hard to beat. It takes a few seconds. Everyone knows how to do it. All the cashiers know how to take it. [t is simple."-15 Competition Apple F'ay's launch spurred a tornado of activity among its competitors. For example: I Softcard, the mobile wallet owned b1. the three largest US carriers, was sold to lCioogle in 2015 for an undisclosed sum. The carriers also agreed to pro-install a retooled version of lIEoogle Wallet on the new Android phones they sold.\" I In May 21315, lICioogle announced the launch of Android Pay; a service that would let consumers pay by simply tapping their phone on an NFC terminal without waking up the phone or entering a PIN or password.\" I'Google did not earn any transaction fees from bank issuers that supported Android Fay.\" Google also plarmed to launch Android Pay with few selected retailers\" loyalty programs integrated into the app. 3" I In 201:4J eBay annotmced that PayPal. which had launched a mobile wallet smartphone app that supported multiple payment types in EH13, would be spun off as a separate company the following year.\" I 111 21315, PayFal announced it would acquire Paydiant for $230 million.\" Faydiant was a start- up that supplied back-end wallet technology to large retailers for use in their apps. I In 2012.. a group of large retailers, including F-Eleven CV5. Gap, Lowe's. Target, and Walmart. created a joint venture called the Merchant Customer Exchange [MICK], which planned to launch a mobile payment platform. CurrentC. in 2015. Payments made with CurrentC would link directly to the user's bank aocount [rather than being processed through a credit card to avoid incurring the approximately 2% interchange feel.\"- lCurrentC also offered participating retailers the chance to track consumer shopping behavior and loyalty data across all merchants that accepted CurrentC.\" I In February 2:115, rival handset-maker Samsung acquired LoopPay, a start-up whose payment system worked with both NFC and mag-stripe technology. A month later, Samsung announced the launch of its new mobile wallet. Samsung Pay, which would use tokenization and, on select Samsung phones like the Galaxy '36 and 55; Edge, fingerprint scanning to conduct secure mobile transactions.\"'1 Samsung Pay's compatibility with both NFC and mag; stripe technology meant that it would work with Q'i- of retail outlets when it launched in the US in the summer of 215.i5 Additionally. many observers believed that banks would create their own wallets in the future. Tien-Tsin Huangr an analyst at {P Morgan, stated: "A big bank may have over 20 million digital consumers, so launching a mobile wallet that fails has a high cost. Why not partner with Apple Pay at first, then create their own mobile wallet later?\" Richard Crone, CED, Crone Consulting LLC, gave a more pressing case. \"The one who enrolls is the one who controls," he said, noting that owning the mobile transaction interface and data appealed to merchants, banks, and thirdsparty wallets. \"Banks are clearly frustrated to lose their consumer touch points. As traffic to their branches declines, the banks will need to create value-added services before, during. and after payment-because that is where they will connect with their customers." Finally, while there was upside for the payment networks in parh'lering with Apple, they were also exploring alternative payment technologies. Before Apple Pay, MasterCard, American Express, and Visa had worked on developing the tokenization standards that Apple Pay usedslf1 MasterCard and Visa had each previously launched contactless cards that could be used to "tap to pay\" in stores, as well as mobile wallet solutions that banks, merchants, and other partners could use to build their own branded mobile wallets for in-store and online purchases. In the UK, MasterCard lUJ'IZl'tEEl a card that used fingerprint authentication for transactions instead of Ple.\" Reecting on the future of mobile paymenls, Ajay Banga, rChief Executive of MasterCard, said: I think the jury is still out on how the mobile and digital payments will evolveit's miclear who the winners and losers will be. We are the providers of the infrastructure, so we are investing in many different possible outcomes. If you care about the payments ecosystem and you are willing to partner with us, we want to work with you to reduce cash and make payments simple, safe, and smart. The Apple Pay learn was unfazed by the urry of competitive activity following the launch of their service. Cue said, \"I never worry about the competition, because I can't do anything about them I keep a close eye on them, but I worry about what] can do.'r His focus remained on maintaining a high rate of speed to market, both for upcoming Apple Pay innovations and new market latmches. "Apple Pay is built to be an integral part of the iPhone experience; wallets from others will require users to install and open an app to pay,\" added Bailey. Although the Apple Pay service was built using industry-standanl technologies like tokenization and NFC that could be used by Apple's competitors, she said, "We have faith in our ability to outperform, out-create, and out-innovate the competition, in particular in the phone environment." Beyond the First Inning W's are more condent than E'Ut'i' that 2015 will be the year oprpl'e Pay Tim Cook, Chief Executive Officer, Apple4'H In Apple's January 2015 earnings call, Cook said that Apple Pay accounted for more than $2 of every 53 spent using contac'dess payments across the networks of Visa, MasterCard, and American Express.\" "I think we're still in the first inning [with Apple Pay]. There's tons of things on our roadmap of adding functionality to it,\" said Cook. By May 2U15, Apple Pay was still making headlines: Apple was in discussions wid'l Home Depot to incorporate Apple Pay in over 2,000 stores5\" and said it wished to expand internationally in countries such as China. \"We very much want to get Apple Pay in China," Cook told Xinhua, a Chinese news outlet. \"I'm very bullish on Apple Pay in v'China.\"51 \"As Tim said, our longterm goal is to replace the wallet, so we're looking at all the things that are inside your wallet to see where our core technology could be applied to add value,\" said Bailey. "Mass adoption is key. We are not in 1111? business of making niche products." As Bailey considered what would be needed to achieve mass adoption, she thought about how to prioritize the activities needed to continue Apple Pay' s momentum. Should she focus on launchng new capabilities beyond Ihe current features of Apple Pay? In July 2015, Apple Pay launched in the United Kingdom. What other regions should the service target next? And how would Apple Pays competitors react? Exhibit 1 Payment Types Used in the US by Value, 2014 Other Paper- Payments 14% Card Cash Payments Payments 46% 25% Electronic Direct/Automated Clearing House (ACH) Source: Adapted from "Financial cards and payments in the US," Euromonitor International, February 2015, accessed May 2015. Exhibit 2 Credit Card Systems by Transaction Value (in $ billions) in the US, 2009-2013 3500 3000 2500 2000 1500 1000 500 2009 2010 2011 2012 2013 Open System . Closed System Private LabelExhibit 3 US Retail Spending (in billions) by Platform, 2014-2019E 2014 2015* 2016* 2017* 2018* 2019* 5-year CAGR Total Retail $4,701 $4,874 $5,049 $5,231 $5,414 $5,603 4% E-commerce* $306 $349 $394 $443 $494 $548 12% Mobile Payments $52 $67 $83 $100 $119 $142 22% In-Store $4 $7 $10 $16 $23 $34 56% In-App $43 $53 $63 $72 $81 $91 16% P2P $5 $7 $10 $12 $14 $17 26% Source: Adapted from "Retail Ecommerce Sales (excludes travel), United States, 2013-2019 (in billions)," eMarketer, 2014; "Retail Sales, United States, 2013-2019 (in billions)," eMarketer, 2014; and Denee Carrington, "US Mobile Payments Forecast, 2014 to 2019," Forrester, November 17, 2014, accessed April 2015. * Denotes estimated figures. Exhibit 4 Apple Annual Net Sales by Product Category, 2014 5% iPhone iPad 11% Mac 56% 20% ITunes, Software and Services Accessories + iPod Source: Adapted from public commentary and resources. Exhibit 5 Global Cost of Payment Card Fraud ($ billions), 2014 Rest of the World . United States $7.1 $5.5 $4.8 $3.2 $3.6 56.8 $5.4 $6.2 $3.7 $4.0 2009 2010 2011 2012 2013Apple Pay 516-027 Exhibit 6 List of US Retailers That Accept Apple Pay, 2015 Retailers Accepting Apple Pay As of July 1, 2015 Acme ExtraMile Lucky Sephora Aeropostale Firehouse Subs Macey's Shaw's American Eagle Outfitters Food Maxx Macy's Six:02 Apple Stores Foot Locker Mcdonald's Sports Authority BabiesRUs FootAction Meijer Sprouts Farmer's Market Bashas Fuddruckers Office Depot Staples Bi-Lo GameStop OfficeMax Star Market BJ's Golden State Warriors Orlando Magic Subway Bloomingdales Harvey's Supermarket Nike Texaco Champ's House of Hoops Panera Bread ToysRUs Chevron Jamba Juice Peet's Coffee United Supermarkets Coca-Cola Vending JetBlue Petco Unleashed by Petco Dan's Fresh Market Jewel Osco Pep Boys Walgreens Davis Food & Drug Kids FootLocker Phoenix Suns Walt Disney World Dick's Fresh Market Lady Foot Locker Radioshack Wegmans Disney Store Lego Rubio's Whole Foods DuaneReade Lin's Fresh Market Run by Foot Locker Winn Dixie Express Luby's Save Mart Supermarkets By December 31, 2015 Albertsons Carmike Cinemas Jersey Mikes Regal Cinemas Anthropologie Dunkin Donuts Johnny Rockets Renaissance Hotels B&H Edition Kohl's T-Mobile Baskin Robbins El Pollo Loco Levi's Trader Joe's Best Buy Forever 21 L.L. Bean Urban Outfitters BevMo Free People Marriott White Castle Big Lots JCPenney Raley's Source: Adapted from company documents.Exhibit 7 Example Use of Apple Pay in the Panera Bread App, 2014 9:41 AM 100% 1 ITEM $8.59 Order Summary Rapid Pick-Up Subtotal: $8.59 Thursday 08/28 at 08:27 PM 20807 Stevens Creek Boulevard Cupertino, CA 95014 *Name on order: John Appleseed Whole Strawberry Poppyseed & Chicken Salad $8.59 w/French Baguette 350 cal Strawberries; Romaine Lettuce; Mandarin Oranges; Fat- Free Poppyseed; Fresh Blueberries; Fresh Pineapple; Chicken; Pecans; Customize Duplicate Remove Remove ALL Buy with = Pay Other Payment Options Source: Company documents.Get all the power of American Express when you use Apple Pay' TM AMERICAN EXPRESS Pay Source: American Express, "Apple Pay," https://www.americanexpress.com/us/content/apple-pay/, accessed May 2015. Exhibit 8b Apple Pay Advertisements Whole Foods Market . Follow @WholeFoods Grocery shopping takes long enough! Now #ApplePay makes it easier to check-out... LEARN MORE: bit.ly/1DgBHP5 NOW ACCEPTING APPLE PAY. Apple Pay is the easy, secure and private way to pay on your iPhone 6. #applepay Pay Source: Whole Foods, "Apple Pay," Twitter, October 31, 2014.Google in March 2015. And while Apple Pay's acceptance in 700,000 retail locations within six months was impressive, it accounted for less than 10% of the 7 to 9 million retail establishments in the US.* Reflecting on these challenges, Bailey wondered, "What should Apple do to continue the early momentum for the adoption and use of Apple Pay?" US Payments Landscape In 2015, annual US retail spending was projected to reach $4.7 trillion and to grow at 4% per year through 2019.5 Payments were not simply a large business; they were also an important touch point for consumers. "Payments are an integral part of everyone's lives," said Bailey. "In the US, adults make over 400 payments per year. In some Asian countries, it's 700 and growing." In the US, consumers used cash for 25% of their monthly payments by value, while credit and debit cards made up 46% of payments by value (see Exhibit 1). Although cash was less convenient for consumers to obtain and use than credit or debit cards, it was more widely accepted. Merchants saw credit cards as a double-edged sword: credit cards carried transaction fees but also had larger- than-average transaction sizes. The origins of modern credit cards could be traced to the private-label store cards issued by Sears, one of the oldest department stores in the US, in the early part of the 20th century. The cards allowed shoppers to buy items on credit, but only at Sears stores. In 1950, Diner's Club created a credit card that could be used at participating restaurants in New York City. Eight years later, American Express launched a card for travel and entertainment expenses." In 1966, MasterCard and Visa launched the first "open" credit payment systems through a consortium of banks, which allowed consumers to use credit at a variety of participating retail outlets." By 2015, private-label cards like the Sears card, closed system cards such as American Express and Discover, and open system cards existed side by side. Open system cards processed over four times the transaction value of the closed system and private-label cards (see Exhibit 2 for US market sizes). Mobile Payments Although e-commerce and mobile commerce (m-commerce) made up only 6.5% and 1.1% of all US retail transactions in 2014, they were expected to grow much faster than the total market (see Exhibit 3) due to increasing smartphone penetration and the growing number of retailer apps that allowed m-commerce. In-store mobile payments, where the phone worked like a payment device, were expected to grow in the US from 0.1% of all in-store retail payment volume in 2014 to almost 15% by 2019. 11 Many companies and start-ups had offered in-store mobile payment services in recent years, but no clear winner had emerged. Even mobile wallets launched by digitally savvy firms like Google had failed to take off. Google Wallet, launched in 2011, had fewer than 10 million global downloads two years after its launch. Several factors contributed to the limited adoption of Google Wallet, including merchants and banks withholding support for the service due to concerns over the ownership of consumers' transaction data; the limited number of phones that carried the "near-field communication" (NFC) chip needed to make mobile payments; and the refusal by three large US telecom carriers (T-Mobile, Verizon, and AT&T) to support Google Wallet on their networks.Apple Apple Computer (Apple) was founded in 1926 by Steve Jobs and Steve Wozniak. The companyr launched its easytouse Apple [1 personal computer in 19518, which helped the emerging personal computing market to grow quickly. Apple's computers had strong sales through me 19805 and 1990's, until it began creating lower-priced products to better compete against IBM and other PC manufacturers_13 By 199?, some insiders believed that Apple was on due brink of bankruptcy. Steve Jobs, who had left the firm in 1985, returned to Apple that year and ushered in a new era of innovation, launching groundbreaking products like the iI-'od (2001), due iI'hone (2007], and \"die ii-'ad [2010). Unlike other computer or smartphone manufacturers, Apple produced both hardware and software for its products, as well as services, which allowed it to create seamless user experiences d1at were difficult for its competitors to replicate. in October 2014, Boston Consulting Group ranked Apple as the most innovative company in the world for the tenth consecutive year."I In 2013, Apple's most popular product, the iI'hone, accounted for over half of Apple's revenues, with unit sales of 150 million and revenue of $91 billion worldwide. Apple launched die iPhone 6 and 6 Plus in October 2014; in \"die first weekend following the launch, it sold a combined 10 million units of these new phones.'5 At d1e end of the first full quarter of sales, Apple had sold 3'45 million iI-'hone unitsaa 46% increase over the previous year.1Er In March 2015, analysts estimated d1at the il'hone 6 and 6 Plus accounted for 29% of all il'hone usage."r In the fourth quarter of 2014, Apple's share of phone sales in the US was nearly 42%, while Samsung, Apple's largest handset competitor, had a market share of 30%.1H Globally, Samsung led with a 21% share compared to Apple's 10% share.\" In addition, two major operating systems dominated d'le marketApple's iOS for iPhone and iPad, and lCoogle's Android, which supported multiple phone manufacturers, including Samsung. Apple's iDS had worldwide market share of 20%,2U although its US market share was far higher, at 43 93. By 2015, Apple had become the largest company in the world, with market cap of over $700 billion, sales of more than $170 billion, and gross profit of over $64 billion. While the majority of Apple's revenue came from U'IE sale of its devices {Exhibit 4], revenues from services, such as music sold through iTunes and apps for d1e iPhone and il'ad from H'lE App Store, were growing steadily. Developing Apple Pay Apple's Approach Although Apple's portfolio included many billiondollar products and services, \"they didn't start as multibilliondollar projects," said Cue, who was instrumental in creating the Apple online store in 1998, the iTunes store in 2003, and the App Store in 2008. "When we created die App Store, we had no idea that it would be a $20 billion business. The danger here is doing only things you think will be multibilliondollar ideas." Bailey expanded on Apple's approach to developing new products and services: We don't think about how to justify these services to the business. For example, we don't charge people for their use of Siri, yet some people lead better lives with Siri than without it. We didn't do an ROI on Siri, because certain categories of service are obvious places where Apple can add value. Replacing the wallet is one, as is Siri, as is Maps. If we create new, better experiences with our products and technologies, that will help us succeed in the long run. Cue agreed: "Most companies start with the economics; we start from the consumer's point of view. If we solve a consumer's problem, then someone will pay for it." This view was ingrained in Apple's culture and reflected Jobs's philosophy of taking a long-term view and having a relentless focus on the consumer experience. This intense focus on consumers had paid off well for Apple in the past. "When Apple launched iTunes," said Bailey, "the goal wasn't to disrupt the music industry; it was to create a new consumer experience." Cue recalled that when iTunes was launched, the largest music labels told Jobs that in order for it to be successful, iTunes would need to sell 1 million songs over a one-month period within the first six months of launch. "We sold 1 million songs in the first six days," said Cue. "We didn't know how successful iTunes would be; we just knew it was a killer product." Designing Apple Pay for a Better Consumer Experience While everyone expected Apple to disrupt the existing payment system, Apple instead decided to work within some elements of the current payments ecosystem. Bailey explained: We want to support what people already use and love. Consumers are already comfortable using their credit and debit cards that are supported by the majority of merchants and banks. Banks are good at what they do: they are good at credit, branding, customer service, and conducting payments. Apple's role was simply to bring together the hardware, software, and services to create the experience on the phone. However, working within the current ecosystem that consumers "already use and love" created the challenge of bringing additional value through Apple Pay. After studying the existing card payment process and current pain points of consumers, Apple decided that if Apple Pay was easy, secure, and private, then it could, in fact, add value to consumers. The iPhone 6 and 6 Plus featured hardware designed for this purpose, including NFC technology (wireless technology used to communicate with NFC-equipped merchant point-of-sale terminals"), Touch ID (a fingerprint reader used to authenticate transactions), and the secure element (a chip on which sensitive information was stored separately from the rest of the device). Easy George Dicker, the engineering manager for Apple Pay, noted that Apple Pay, like every Apple product, followed Jobs's mentality of "it just works" right out of the box. During the setup for the iPhone 6 or 6 Plus, a user was asked whether she wanted to enable Apple Pay and if she wanted to add the card on file in iTunes to Apple Pay. If she elected to use the card in iTunes, only the card verification value (CVV) was needed to complete the setup. Consumers could include additional cards by using the iPhone's isight camera to recognize the card, and then their bank would verify the information. The credit and debit cards used by Apple Pay were stored in Passbook (subsequentlyrenamed Wallet), an application launched by Apple in 2012 to store coupons, airline tickets, and loyalty cards. Apple Pay was also easy to use in stores. Unlike competing wallets, which had to be downloaded from an app store and opened at checkout, the NFC signal from a point-of-sale (POS) device would automatically "wake up" Apple Pay so that the service was ready for immediate use by consumers at checkout without the need to unlock the device. Additionally, Apple's Touch ID eliminated the need for consumers to enter a password to authenticate a purchase Secure Credit card fraud in the US amounted to over $7 billion in 2013, a 35% increase over that in 2012,21 and globally, total credit card fraud was almost twice that number (see Exhibit 5). Consumers could experience fraud in two ways: individual fraud (when a card was lost, stolen, or declined for an authentic purchase) or merchant breaches (when Target's or Home Depot's databases were breached, and the consumer had to remember if she had shopped there to know whether her card was at risk). In a typical card transaction, a customer's credit card data might be shared with the merchant, the merchant acquirer, the card network, and the issuing bank. Each one of these handoffs was an opportunity for fraud and/ or data privacy breaches to occur. Cue said, "I can't go one week without thinking about these issues as a consumer." The cost of this fraud was typically borne by the banks that issued the cards. Enhanced security was one of the most important features of Apple Pay. When a consumer used Apple Pay, the transaction was authenticated using a fingerprint or a typed pass code, and then encrypted using a tokenization process-a onetime security code and a device-specific token to conduct payment transactions, rather than providing the merchant with a consumer's credit or debit card number, expiration date, CVV, and billing address. Tokenization limited the opportunities for data breaches by not using a consumer's actual credit or debit card number. Apple Pay also eliminated many hassles to consumers that resulted from fraud. For example, if an iPhone was lost or stolen, banks could generate a new token remotely that would be linked to the same credit card as before, removing the need to cancel and issue a new card. If a breach at a merchant occurred, fraudsters could obtain only the token information, which could not be used for payment unless it was accompanied by the transaction-specific cryptogram generated by the tokenized device. Private Many mobile wallets built their business models around using consumer purchase data to make money on advertising or other services. In contrast, Apple Pay did not store consumers' transaction data. Cue observed that consumer expectations of data use were shaped by credit cards: You assume the bank knows about your payment, since they must know the total amount to accept the charge, and you assume the merchant knows what you bought and how much you paid. We entered a market where every one of the alternatives wanted to know where and what you were buying, and wanted to use that data to make money. Consumers were often unaware of how their data was used, and those who were aware often viewed it negatively. Apple Pay shared only the data necessary to complete the transaction, but unlike a credit card, Apple Pay was designed to protect the consumer's personal information, transaction data, and credit and debit card information. Payment transactions were between the consumer, the merchant, and the bank. Merchants and banks also benefited from Apple Pay's privacy because it protected the merchants' purchase data from use by third parties. Cue said: "If you're Target and a mobile payments company sells your data to your competitors, that is a real threat."Apple Team Structure To design Apple Pay and create these consumer benefits, Apple formed a small team of experts from Apple's functional groups in wireless technology, server technology, iOS, retail, and human interface, among others. "Large companies typically distribute decisions and define P&L responsibilities that create friction," said Cue. "We are structured like a small company where everyone comes together for a common purpose. \"Bailey explained: All of Apple's products could fit onto one conference table; it's complicated, but simple. If you look at our competitors, they're :in it] different businesses, including services, which are not that related from a core technology perspective. For Apple, there are core skills like expertise in iD'E'I or wireless that are present in all of our devices. That's why a functional structure works for Apple. Bailey noted, \"We believe a functional structure is better for Apple than the business unit structure, because busiJ'Ie-ss units create agendas around themselves. The team that works on wireless today doesn't have a business unit agenda; they have a consumer agenda.'r Bailey cited Apple's strong debate culture as a driver of success for Apple Pay. "A software engineer may see a 'server solution,r but the hardware engineer might be able to offer an easier, chip-based solution to the same issue," she said. "Apple Pay is the culmination of that culture; it is one of the most crosssfunctional consumer-focused teams.\"r Despite its intense focus on the consumer experience, Apple performed little to no consumer testing before launch. jobs believed that consumers could not "see around the corners,'r especially for teclmology products. The user-interface teams worked closely with several designers to produce concepts for the whole team to review. The top concepts were shared with decision makers, who picked the designs to push forward. Then the team performed an engineering implementation test to ensure the concepts were teci'uiologicaliy feasible. Apple employees tested Apple Pay at several retailers and within apps before launch to ensure that the service worked easily and quickly. Biifi, Networks, and Merchants To create a great customer experience on the phone, Bailey realized Apple Pay would need to \"win the hearts and minds not only of consumers, but also of banks and merchants.\"r Apple considered a number of payment approaches for Apple Pay, including a service for web checkout using the cards on file with lTllrtES} launching an entirely new system that didn't use credit or debit cards at all; and partnering with a payment network or a bank to create a new, co-branded payment platform. However, none of these alternatives could meet the goal of adding value for consumers, merchants, and banks. Bailey explained: "We didn't want to disrupt the payment industry. We wanted you, the consumer, to be able use the payment methods you loved.\" Cue elaborated, "Nmnerous start-ups and larger technology companies tried to disrupt the payment industry, however, convincing consumers and merchants to adopt a new payment system, when they were satised with the old system, was very difficult." The process to select Apple's approach to payments produced "a thousand 'no's for every 'yes,'\" according to Bailey, before the team chose a system that used the existing credit card and bank systems as its base. Banks Apple worked with several leading banks [including American Express, Bank of America, Barclaycard, Capital One Bank, lChase, Citi, Navy Federal Credit Union, PNC Bank, USAA and US. Bank, and 1It'lfells Fargo}, which together accounted for 33% of the credit card transaction volume in the US, around the launch of Apple Pay. By March 215, over 2,500 banks had agreed to make Apple Pay available to their consumers. Apple Pay offered banks a way to improve the consumer experience, remain top-of-wallet in a new payment ecosystem, and grow m-commerce transactions. Apple approached the banks roughly nine months before launch. Bailey explained: When we began the negotiations with the banks, the banks had to take it on faith that Apple Pay would be an amazing experience for their consumers. The leaders in the payment industry signed on first, those who had a vision for mobile payments and where the industry needed to go. They chose to partner with us because they believed Apple Pay to be the platform that would drive mobile payments over time. Apple negotiated a fee to be paid by its bank partners for each transaction conducted with Apple Pay. "We were adding value and we were also incurring costs to put the chips into the devices," said Cue. Some media and industry analysts speculated Apple might receive 15 basis points per credit card transaction and roughly half a penny per debit card transaction.2 Apple Pay was expected to generate savings for banks by reducing fraud and increasing revenues by replacing more cash-based transactions. Payment networks The three largest US payment networks, MasterCard, Visa, and American Express, collaborated with Apple. As Bailey explained, "The networks want payment volume; that is their core business. Apple Pay will drive volume, which is better for the payment networks." Since Apple Pay "rode the rails" of the existing credit and debit networks, Cue believed that consumers' opinions of the payment networks would improve. "We told the whole world that American Express, MasterCard, Visa, and your banks are a great way to pay," he said. Merchants Apple divided US retailers into three segments: The top 100 merchants that collectively conducted roughly 40% of transactions by value. "Our team works closely with these merchants to cultivate relationships and explain how Apple Pay works," said Cue. The thousands of small to-medium-sized enterprises (SMEs) that possessed credit card POS terminals and conducted roughly 50% of transactions. To reach the SMEs, the Apple Pay team worked with large payment acquirers, the companies that managed payment processing for small businesses, including First Data, Bank of America Merchant Services, and Elavon, to educate the payment acquirers about the use of Apple Pay. The payment acquirers then leveraged their sales staff, which sold credit card terminals to the SMEs, to set up Apple Pay in those retailers. Finally, there were millions of small merchants, such as farmer's market vendors, who conducted about 5% of transactions. These merchants were supported through traditional electronics retailers, including Apple Stores, which sold low-cost mobile-based terminals that could accept Apple Pay. Apple provided all merchants with public resources and a Frequently Asked Questions (FAQ) page to educate them on how to start accepting Apple Pay, a place to download the payment mark so they could let customers know that they accepted Apple Pay, and a number to call with questions. At the time of Apple Pay's launch, 220,000 merchants (including grocers, pharmacies, quick-service restaurants, clothing stores, and stadiums, among others) were offering Apple Pay to customers (see Exhibit 6). Various retailers adopted Apple Pay for their own specific use: Panera incorporated Apple Pay into its stores and in its app to increase throughput and ordering ahead during the busy lunch period. Apple Pay's flexibility gave consumers morechoice in how to order. "I'm a merchant; I want people to pay however they want to pay," said Blaine Hurst, Chief Growth and Transformation Officer at Panera. "If you would like to use Apple Pay in-store, there is no need to download the Panera app to do so. However, if you are using our app, you have the option to pay with Apple Pay." Whole Foods offered Apple Pay to customers as a way to provide a better experience for its wealthy, digitally savvy consumers. "Our consumers' expectations of what the optimal in- store experience should be are not being set by other grocers-they are being set by the Apple Store or Nordstrom. Since we share consumers with these cutting-edge retailers, we have adopted new technologies to meet evolving expectations," said Jason Buechel, Chief Information Officer at Whole Foods. . OpenTable, a restaurant reservation app, decided to integrate Apple Pay to allow diners to pay their bill through OpenTable's app. Matt Roberts, Chief Executive of OpenTable, said, "With Apple Pay, OpenTable diners can skip the step of adding a card to their profile and simply settle their check with a single touch using iPhone 6 or iPhone 6 Plus."23 By March 2015, almost 700,000 retailers in the US accepted Apple Pay, up from 220,000 just six months earlier, yet this still accounted for less than 10% of the retailers that accepted credit cards.24 Some small businesses could not justify the cost of upgrading their POS terminals to an NFC- equipped terminal that might cost them $300-$500 per terminal.25 Others found these costs nominal compared to the benefits, especially since most merchants would soon be required to support credit cards with EMV chips and re-terminalize anyway, or risk accepting more liability if a breach occurred. Certain larger retailers declined to accept Apple Pay because they were involved in the creation of a rival payments platform called the Merchant Customer Exchange (MCX), which planned to launch its own mobile payment app in 2015. Shortly after Apple Pay launched, CVS and Rite Aid blocked the use of Apple Pay in their stores by disabling their NFC readers. In addition, some retailers had successfully launched their own payment systems and did not see any value in replacing it with Apple Pay. For example, Starbucks' mobile app combined payment with loyalty via a bar-code-based app. In 2013, 11% of Starbucks' sales volume came from its mobile wallet, which processed around 4 million payments per week. Although Starbucks later announced it would integrate Apple Pay into its app as a way to add money to the Starbucks mobile wallet, it did not offer in-store POS-based Apple Pay transactions.28 Launching Apple Pay Apple executives carefully thought through the timing of Apple Pay's launch. Cue explained: If you time it well, amazing things can happen. iPod was successful due to the 1.8- inch drive that was designed for laptops. iPhone leveraged the timing of 3G. For Apple Pay, there are significant changes coming in October 2015, when merchants will be required to migrate to EMV-compliant cards with built-in smart chips or pay for fraudulent charges themselves. Use of EMV in stores required POS terminals that were equipped to read the chips and often resulted in longer transaction times, since reading the microchip was more involved than swiping a magnetic stripe (mag-stripe). Although NFC technology was not integral to the technology needed tosupport Elk-W cards. the surge in demand for new terminals provided an oppothnity for many retailers to aoquire the NFC-equipped terminals needed for Apple Pay at little to no cost above those incurred to be in compliarce with the new regulation. In October 2014, Apple Pay was launched in the US for purchases in stores and within apps. For payments, Apple had previously engaged the large community of iDS app developers to integrate Apple Pay into their apps [see Exhibit 5'" for examples}. Baris Cetinok, Head of Product Marketing for Apple Pay, said: \"To integrate Apple Pay into an app. the developers did not need to talk to us. They could simply go to iDS developer center and grab the relevant code.'r Large merchant partners had a similarly positive experience. According to Prat vemana, 1|tuiice President of Mobile Commerce at Staples, \"The Staples team that worked on Apple Pay was one of the most enthusiastic and fast- moving teams. It took us only eight weeks to integrate Apple Pay into the Staples app.'r "Payments in stores and within apps required similar security measures and consumer information,'r said Bailey. "The adoption of encryption and other security standards varied by website, which made it challenging to create a consistent consumer experience on the websites." In addition, Cue observed. "Many websites were moving towards apps, so with Apple Pay's focus on apps, we were being future-forward.'r Apple decided to go after a broad range of purchase occasions rather than to target specic apps for Apple Pay. The team believed that in order to habituate consumers. they had to go after high-volume transactions like those in quick-serve restaurants, groceries, and pharmacies. Many of the large merchants and banks accepting Apple Pay launched ads touting its benefits {see Exhibits Ba and Eb}. Apple itself did no advertising for Apple Pay's launch beyond a handful of co- marketing programs. "Our products are our best marketing," said Cetinok. Apple's partners agreed. "Mobile has the lowest conversion rate of all digital sites because it is tedious for consumers to fill almost 4t] fields to enter their credit card and address on a small screen,\" said Staple's liemana. "Apple Pay makes it easy to go to the mobile cart and authenticate with your finger then you are done! [if the customers who use Apple Pay in the Staples app, one-third are first-time Staples customers and about a quarter return to Staples to purchase again with Apple Pay.\" In spring 21315, Apple created PCB decals and other material for retailers to display in the stores. And in April 21315, Apple launched the Apple Watch. which made it even easier to pay in stores with Apple Pay. [n lune 21315, Apple announced that Apple Pay would give shoppers more ways to pay by adding support for rewards programs and store-issued credit and debit cards with a new version of iDS launching that fall. With the addition of support for Discover cards, also beginning in the fall, Apple Pay would accept credit and debit cards across all the major card networks, issued by the most popular banks, representing 98% of all credit card purchase volume in the US. It was also announced in luly 1015 that Apple Pay acceptance had reached over 1 million locations in the US and that the service would expand to the UK. with over 25, locations accepting Apple Pay and support from eight of the UK's most established banks. across all of the major credit and debit card networks. litMn rlret Performance Within F2 hours of Apple Pay's launch, over 1 million credit and debit cards had been activated on the service}? By the fourth week following launch. Apple Pay accounted for over 150M transactions at Whole Foods and 50% of the tap-to-pay transactions at McDonald's 111,011! US locations, and it had doubled the number of mobile payments at Walgreens'\" Even though Apple Pay was the rrmst quickly adopted mobile payment system ever. there were conflicting reports of how frequently Apple Pay was used. Much of the discrepancy was likely due to

Step by Step Solution

There are 3 Steps involved in it

Will Apple Pay be a huge success with consumers Why or why not Apple Pay has the potential for succe... View full answer

Get step-by-step solutions from verified subject matter experts