Answered step by step

Verified Expert Solution

Question

1 Approved Answer

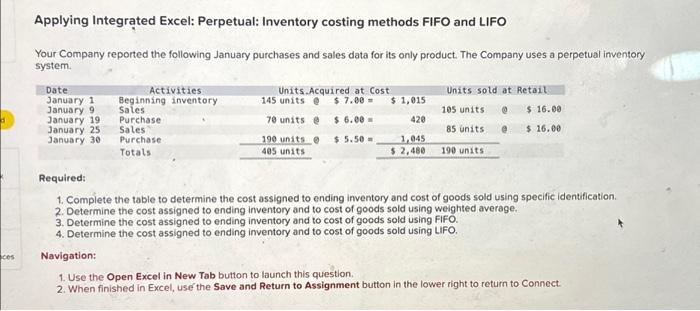

Applying Integrated Excel: Perpetual: Inventory costing methods FIFO and LIFO Your Company reported the following January purchases and sales data for its only product. The

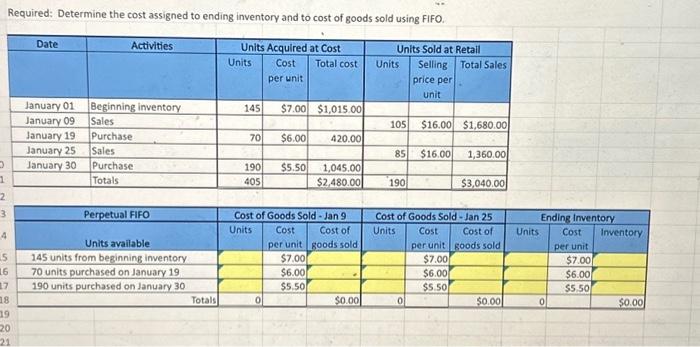

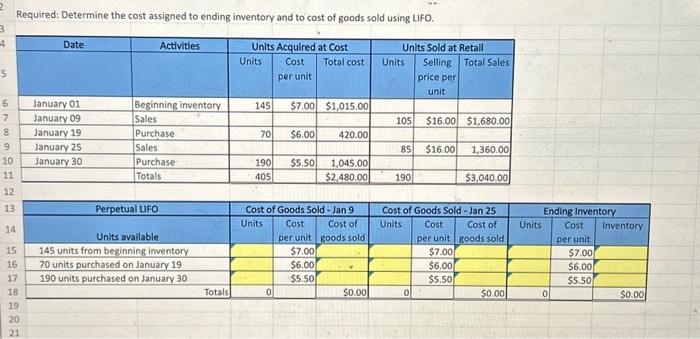

Applying Integrated Excel: Perpetual: Inventory costing methods FIFO and LIFO Your Company reported the following January purchases and sales data for its only product. The Company uses a perpetual inventory system. Date January 1 January 9 January 19 January 25 January 30 Activities Beginning inventory Sales Purchase Sales Purchase Totals Units Acquired at Cost 145 units @ $ 7.00 = 70 units @ $6.00 = 190 units @ 405 units $5.50 = $ 1,015 420 1,045 $ 2,480 Units sold at Retail 105 units @ 85 units 190 units $ 16.00 $ 16.00 Required: 1. Complete the table to determine the cost assigned to ending inventory and cost of goods sold using specific identification. 2. Determine the cost assigned to ending inventory and to cost of goods sold using weighted average. 3. Determine the cost assigned to ending inventory and to cost of goods sold using FIFO. 4. Determine the cost assigned to ending inventory and to cost of goods sold using LIFO. Navigation: 1. Use the Open Excel in New Tab button to launch this question. 2. When finished in Excel, use the Save and Return to Assignment button in the lower right to return to Connect.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Accounting

Authors: Paul D. Kimmel, Jerry J. Weygandt, Donald E. Kieso

8th Edition

1118484320, 978-1118484326