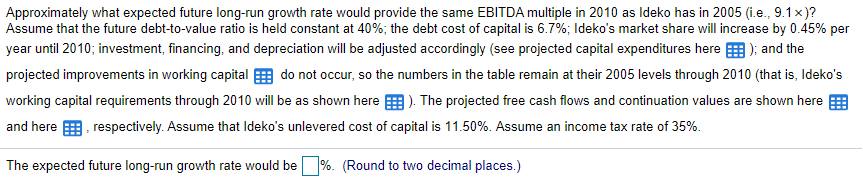

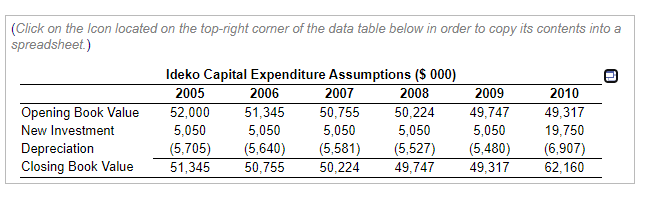

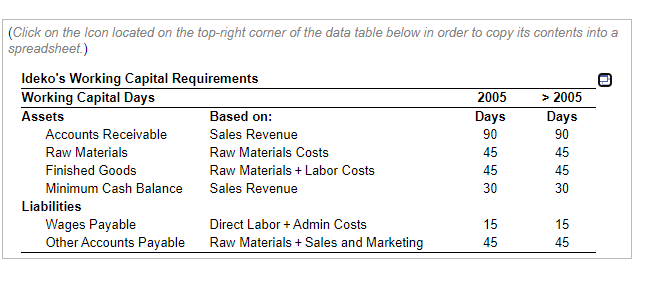

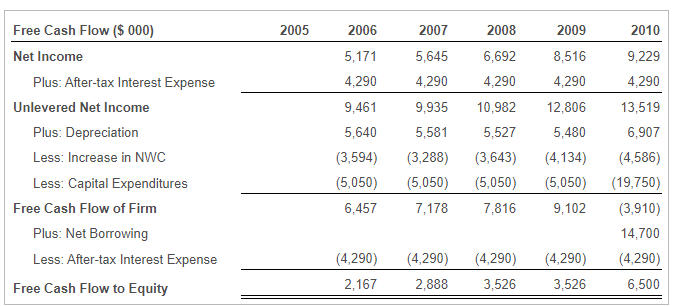

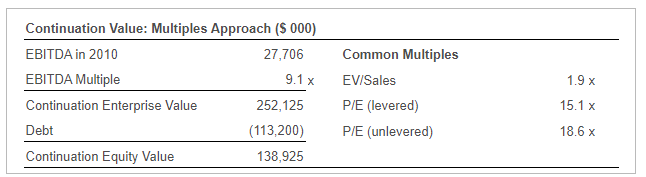

Approximately what expected future long-run growth rate would provide the same EBITDA multiple in 2010 as ldeko has in 2005 (i.e., 9.1 x)? Assume that the future debt-to-value ratio is held constant at 40%, the debt cost of capital is 6.7%; Ideko's market share will increase by 0.45% per year until 2010; investment, financing, and depreciation will be adjusted accordingly (see projected capital expenditures here ); and the projected improvements in working capital do not occur, so the numbers in the table remain at their 2005 levels through 2010 (that is, Ideko's working capital requirements through 2010 will be as shown here :). The projected free cash flows and continuation values are shown here and here respectively. Assume that Ideko's unlevered cost of capital is 11.50%. Assume an income tax rate of 35%. The expected future long-run growth rate would be %. (Round to two decimal places.) (Click on the Icon located on the top-right corner of the data table below in order to copy its contents into a spreadsheet.) Ideko Capital Expenditure Assumptions ($ 000) 2005 2006 2007 2008 2009 2010 Opening Book Value 52,000 51,345 50,755 50,224 49,747 49,317 New Investment 5,050 5,050 5,050 5,050 5,050 19,750 Depreciation (5,705) (5,640) (5,581) (5,527) (5,480) (6,907) Closing Book Value 51,345 50,755 50,224 49,747 49,317 62,160 (Click on the Icon located on the top-right corner of the data table below in order to copy its contents into a spreadsheet.) Ideko's Working Capital Requirements Working Capital Days 2005 > 2005 Assets Based on: Days Days Accounts Receivable Sales Revenue 90 90 Raw Materials Raw Materials Costs 45 45 Finished Goods Raw Materials + Labor Costs 45 45 Minimum Cash Balance Sales Revenue 30 30 Liabilities Wages Payable Direct Labor + Admin Costs 15 15 Other Accounts Payable Raw Materials + Sales and Marketing 45 45 2005 2006 2007 2008 2009 2010 18,148 26,017 1,960 2,556 20,834 2,091 4,607 6,945 4,216 23,301 2,314 5,178 7,767 38,560 5,812 8,672 Working Capital ($ 000) Assets Accounts Receivable Raw Materials Finished Goods Minimum Cash Balance Total Current Assets Labilities Wages Payable Other Accounts Payable Total Current Liabilities Net Working Capital Increase in Net Working Capital 29,006 2,819 6,515 9,669 48,009 32,292 3,104 7,294 10,764 53,454 6,049 30,373 34,477 43,057 1,340 1,363 1,542 1,697 1,866 3,350 4,690 25,683 3,837 5,200 29,277 3,594 4,453 5,995 32,565 5,152 6,849 36,208 3,643 5,801 7,667 40,342 2,102 6,424 8,526 44,928 4,586 3,288 4,134 2005 2006 2007 2008 2009 2010 8,516 4,290 Free Cash Flow ($ 000) Net Income Plus: After-tax Interest Expense Unlevered Net Income Plus: Depreciation Less: Increase in NWC Less: Capital Expenditures Free Cash Flow of Firm Plus: Net Borrowing Less: After-tax Interest Expense Free Cash Flow to Equity 5,171 4,290 9,461 5,640 (3,594) (5,050) 6,457 5,645 4,290 9,935 5,581 (3,288) (5,050) 7,178 6,692 4,290 10,982 5,527 (3,643) (5,050) 7,816 12,806 5,480 (4,134) (5,050) 9,102 9,229 4,290 13,519 6,907 (4,586) (19,750) (3,910) 14,700 (4,290) 6,500 (4,290) 2,167 (4,290) 2,888 (4,290) 3,526 (4,290) 3,526 Continuation Value: Multiples Approach ($ 000) EBITDA in 2010 27,706 EBITDA Multiple 9.1 x Continuation Enterprise Value 252,125 Debt (113,200) Continuation Equity Value 138,925 Common Multiples EV/Sales P/E (levered) P/E (unlevered) 1.9 x 15.1 x 18.6 x Approximately what expected future long-run growth rate would provide the same EBITDA multiple in 2010 as ldeko has in 2005 (i.e., 9.1 x)? Assume that the future debt-to-value ratio is held constant at 40%, the debt cost of capital is 6.7%; Ideko's market share will increase by 0.45% per year until 2010; investment, financing, and depreciation will be adjusted accordingly (see projected capital expenditures here ); and the projected improvements in working capital do not occur, so the numbers in the table remain at their 2005 levels through 2010 (that is, Ideko's working capital requirements through 2010 will be as shown here :). The projected free cash flows and continuation values are shown here and here respectively. Assume that Ideko's unlevered cost of capital is 11.50%. Assume an income tax rate of 35%. The expected future long-run growth rate would be %. (Round to two decimal places.) (Click on the Icon located on the top-right corner of the data table below in order to copy its contents into a spreadsheet.) Ideko Capital Expenditure Assumptions ($ 000) 2005 2006 2007 2008 2009 2010 Opening Book Value 52,000 51,345 50,755 50,224 49,747 49,317 New Investment 5,050 5,050 5,050 5,050 5,050 19,750 Depreciation (5,705) (5,640) (5,581) (5,527) (5,480) (6,907) Closing Book Value 51,345 50,755 50,224 49,747 49,317 62,160 (Click on the Icon located on the top-right corner of the data table below in order to copy its contents into a spreadsheet.) Ideko's Working Capital Requirements Working Capital Days 2005 > 2005 Assets Based on: Days Days Accounts Receivable Sales Revenue 90 90 Raw Materials Raw Materials Costs 45 45 Finished Goods Raw Materials + Labor Costs 45 45 Minimum Cash Balance Sales Revenue 30 30 Liabilities Wages Payable Direct Labor + Admin Costs 15 15 Other Accounts Payable Raw Materials + Sales and Marketing 45 45 2005 2006 2007 2008 2009 2010 18,148 26,017 1,960 2,556 20,834 2,091 4,607 6,945 4,216 23,301 2,314 5,178 7,767 38,560 5,812 8,672 Working Capital ($ 000) Assets Accounts Receivable Raw Materials Finished Goods Minimum Cash Balance Total Current Assets Labilities Wages Payable Other Accounts Payable Total Current Liabilities Net Working Capital Increase in Net Working Capital 29,006 2,819 6,515 9,669 48,009 32,292 3,104 7,294 10,764 53,454 6,049 30,373 34,477 43,057 1,340 1,363 1,542 1,697 1,866 3,350 4,690 25,683 3,837 5,200 29,277 3,594 4,453 5,995 32,565 5,152 6,849 36,208 3,643 5,801 7,667 40,342 2,102 6,424 8,526 44,928 4,586 3,288 4,134 2005 2006 2007 2008 2009 2010 8,516 4,290 Free Cash Flow ($ 000) Net Income Plus: After-tax Interest Expense Unlevered Net Income Plus: Depreciation Less: Increase in NWC Less: Capital Expenditures Free Cash Flow of Firm Plus: Net Borrowing Less: After-tax Interest Expense Free Cash Flow to Equity 5,171 4,290 9,461 5,640 (3,594) (5,050) 6,457 5,645 4,290 9,935 5,581 (3,288) (5,050) 7,178 6,692 4,290 10,982 5,527 (3,643) (5,050) 7,816 12,806 5,480 (4,134) (5,050) 9,102 9,229 4,290 13,519 6,907 (4,586) (19,750) (3,910) 14,700 (4,290) 6,500 (4,290) 2,167 (4,290) 2,888 (4,290) 3,526 (4,290) 3,526 Continuation Value: Multiples Approach ($ 000) EBITDA in 2010 27,706 EBITDA Multiple 9.1 x Continuation Enterprise Value 252,125 Debt (113,200) Continuation Equity Value 138,925 Common Multiples EV/Sales P/E (levered) P/E (unlevered) 1.9 x 15.1 x 18.6 x