Answered step by step

Verified Expert Solution

Question

1 Approved Answer

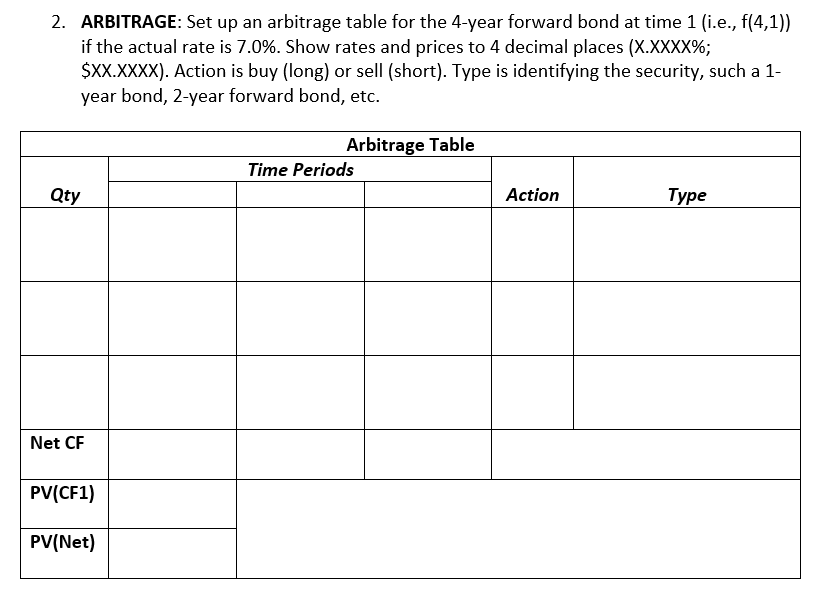

ARBITRAGE: Set up an arbitrage table for the 4 - year forward bond at time 1 ( i . e . , f ( 4

ARBITRAGE: Set up an arbitrage table for the year forward bond at time ie

if the actual rate is Show rates and prices to decimal places ;

$ Action is buy long or sell short Type is identifying the security, such a

year bond, year forward bond, etc.

Please show how to fill out each section of table with equations

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

AS Accounting For AQA

Authors: David Cox,Michael Fardon

2nd Edition

1905777140, 978-1905777143