Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Arbor Systems and Gencore stocks both have a volatility of 41% Compute the volatility of a portfolio with 50% invested in each stock if the

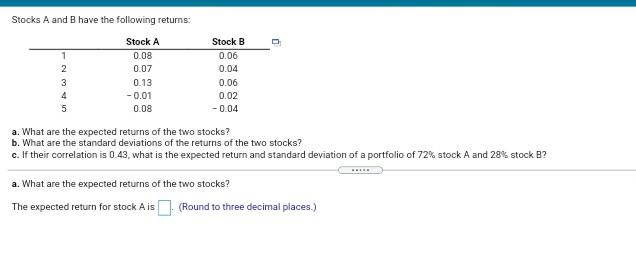

Arbor Systems and Gencore stocks both have a volatility of 41% Compute the volatility of a portfolio with 50% invested in each stock if the correlation between the stocks is (a) +1.00,(b) 0.50. (C) 0.00,(d) - 0.50, and (e) - 1.00. In which of the cases is the volatility lower than that of the original stocks? If the correlation is +1.00, the volatility of the portfolio is (Round to one decimal place.) Stocks A and B have the following returns Stock A 1 0.08 2 0.07 3 0.13 4 -0.01 5 0.08 Stock B 0.06 0.04 0.06 0.02 -0.04 a. What are the expected returns of the two stocks? b. What are the standard deviations of the returns of the two stocks? c. If their correlation is 0.43, what is the expected return and standard deviation of a portfolio of 72% stock A and 28% stock B? a. What are the expected returns of the two stocks? The expected return for stock Ais - (Round to three decimal places.)

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Geography Of Finance

Authors: Gordon L. Clark, Darius Wójcik

1st Edition

0199213364, 978-0199213368