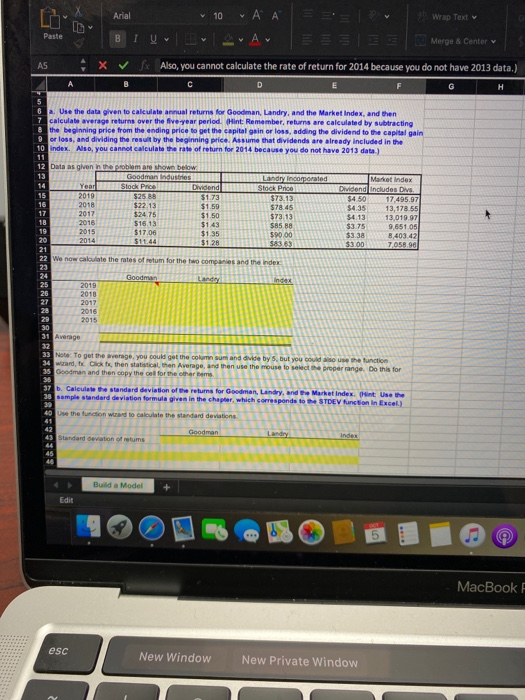

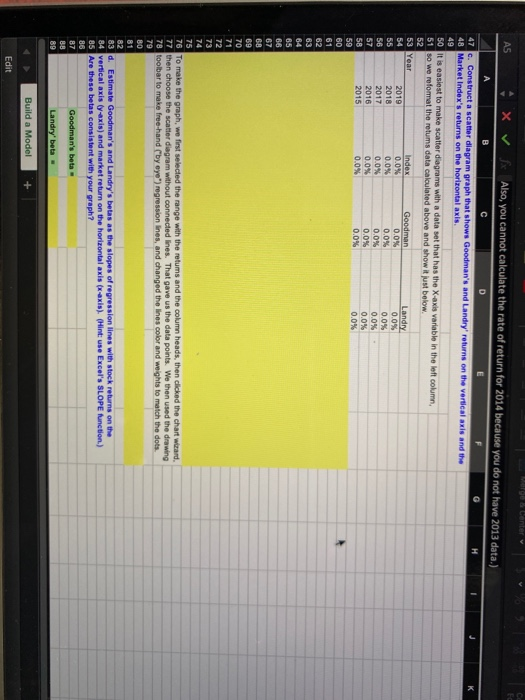

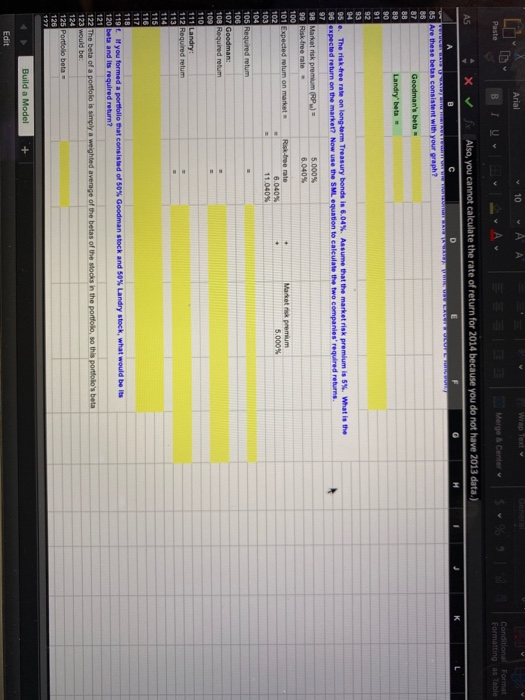

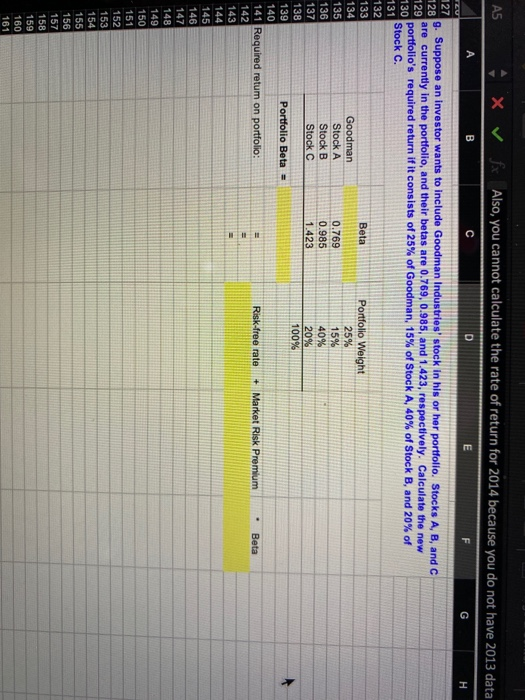

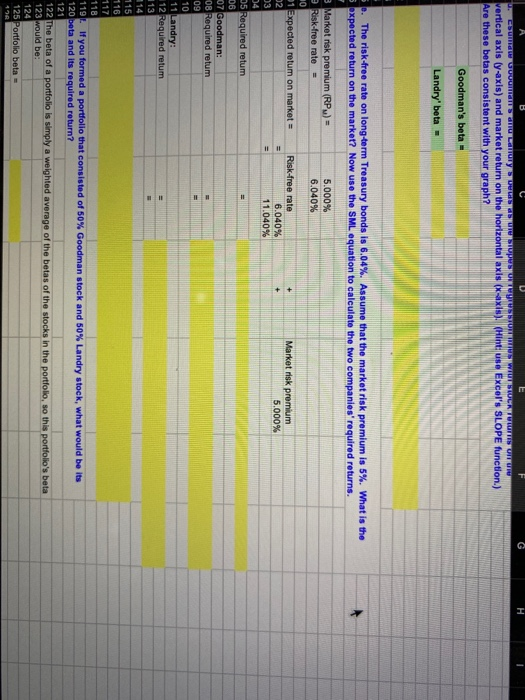

Arial 10 Wrap Text I USA Paste B EE EEE Merge & Center AS X Also, you cannot calculate the rate of return for 2014 because you do not have 2013 data.) D F G H 5 6. Use the data given to calculate annual returns for Goodman, Landry, and the Market Index, and then 7 calculate average returns over the five year period. Mint Remember, returns are calculated by subtracting 8 the beginning price from the ending price to get the capital gain or loss, adding the dividend to the capital gain 9 or loss, and dividing the result by the beginning price. Assume that dividends are already included in the 10 Index. Also, you cannot calculate the rate of return for 2014 because you do not have 2013 data.) 12 Data as given in the problem are shown below 13 Goodman Industries Landry Incorporated Market Index Yearl Stock Price Dividend | Stock Price Dividend includes Divs 15 2019 $25 88 $1.73 $73.13 $4.50 16 17.495.97 2018 $22.13 $1.59 $78.45 $4.35 17 2017 13,178.55 $24.75 $1.50 $73.13 $4.13 13,019.97 18 2018 $16.13 $85 88 $3.75 9,651.05 19 2015 $17.06 $1,35 $90.00 $3.38 20 2014 8.403.42 $11.44 $1.28 $83.63 $3.00 7058.90 21 22 We now calculate the rates of retum for the two companies and the Index 23 24 Goodman 25 Index 2019 26 2018 27 2017 28 2016 29 2015 30 31 Average 32 1.43 33 Note: To get the average, you could get the column sumand divide by 5, but you could use the function 34 wirard, 1x Click then statistical, then Average, and then use the mouse to the proper range. Do this for 35 Goodman and then copy the col for the other bem 37 b. Calculate the standard deviation of the returns for Goodman, Landry, and the Market Index. Mint Use the 38 sample standard deviation formula given in the chapter, which corresponds to the STDEV Hunction in Excel) 40 Use the function wizard to calculate the standard deviations Goodman 43 Standard deviation of retums Index 45 46 Build a Model Edit 5 MacBook F esc New Window New Private Window wage & Center w AS x Fx Also, you cannot calculate the rate of return for 2014 because you do not have 2013 data.) C 47 c. Construct a scatter diagram graph that shows Goodman's and Landry returns on the vertical axis and the 48 Market Index's returns on the horizontal axis. 49 50 it is easiest to make scatter diagrams with a data set that has the X-axis variable in the left column 51 so we reformat the retums data calculated above and show it just below. 52 53 Year Index Goodman Landry 54 2019 0.0% 0.0% 0.0% 55 2018 0.0% 0.0% 0.0% 56 2017 0.0% 0.0% 0.0% 57 2016 0.0% 0.0% 0.0% 58 2015 0.0% 0.0% 0.0% 59 60 61 62 63 64 65 66 67 68 69 70 71 72 73 74 75 76 To make the graph, we first selected the range with the retums and the column heads, then clicked the chart wizard 77 then choose the scatter diagram without connected lines. That gave us the data points. We then used the drawing 78 toolbar to make free hand by eye") regression lines, and changed the lines color and weights to match the dots 79 80 81 82 83 d. Estimate Goodman's and Landry's betas as the slopes of regression lines with stock returns on the 84 vertical axis y-axis) and market return on the horizontal axis (x-axis). (Hint: use Excel's SLOPE function) 85 Are these betas consistent with your graph? 86 87 Goodman's beta- 88 89 Landry' beta- Build a Model Edit 10 Wrap Text v Uw w MA Paste I Conditional Format Formatting as Table EEEEE Merge al Center K AS X Also, you cannot calculate the rate of return for 2014 because you do not have 2013 data.) D E H TUTUTRUSTNICTWU EROLO CORE 85 Are these betas consistent with your graph? 88 87 Goodman's beta- 89 89 Landry beta- 90 91 92 93 94 95. The risk tree rate on long-term Treasury bonds is 6.04%. Assume that the market risk premium is 5%. What is the 96 expected return on the market? Now use the SML equation to calculate the two companies' required returns 98 Market risk premium (RP) = 5.000% 99 Risk-tree rate 6.040% 100 101 Expected retum on market Risk-free rate Market is premium 102 6.040% 5,000% 103 11.040% 104 105 Required retum 106 107 Goodman: 108 Required retum 109 110 111 Landry 112 Required retum 113 114 115 116 117 118 119 If you formed a portfolio that consisted of 50% Goodman stock and 50% Landry stock, what would be its 120 beta and its required return? 121 122 The beta of a portfolio is simply a weighted average of the beas of the stocks in the portfolio, so this portfolo's beta 123 would be: 124 125 Portfolio beta- 126 197 Build a Model + Edit A5 X Vfx Also, you cannot calculate the rate of return for 2014 because you do not have 2013 data G H 129 - B D E F TCU 127 9. Suppose an investor wants to include Goodman Industries' stock in his or her portfolio. Stocks A, B, and C 128 are currently in the portfolio, and their betas are 0.769, 0.985, and 1.423, respectively. Calculate the new portfolio's required return if it consists of 25% of Goodman, 15% of Stock A, 40% of Stock B, and 20% of 130 Stock C. 131 132 133 Beta Portfolio Weight 134 Goodman 25% 135 Stock A 0.769 15% 136 Stock B 0.985 40% 137 Stock C 1.423 20% 138 100% 139 Portfolio Beta - 140 141 Required retum on portfolio: Risk-free rate + Market Risk Premium Beta 142 143 144 145 146 147 148 149 150 151 152 153 154 155 156 157 158 159 160 161 = G H B Esu una sau mury SUSITOUDUTOSWIUT STUCKTUUTTIS TU vertical axis ly-axis) and market return on the horizontal axis ( xxls). (Hint: Uso Excel's SLOPE function.) Are these betas consistent with your graph? Goodman's beta Landry' beta - D. The risk-free rate on long-term Treasury bonds is 6.04%. Assume that the market risk premium is 5%. What is the expected return on the market? Now use the SML equation to calculate the two companies' required returns. 3 Market risk premium (RP) = 5.000% Risk-free rate = 6.040% 10 1 Expected retum on market = Risk-free rate Market risk premium 02 6.040% 5.000% 03 11.040% 34 05 Required retum 06 07 Goodman: 0B Required retum 09 10 11 Landry: 112 Required retum 113 14 115 116 117 118 119. If you formed a portfolio that consisted of 50% Goodman stock and 50% Landry stock, what would be its 120 beta and its required return? 121 122 The beta of a portfolio is simply a weighted average of the betas of the stocks in the portfolio, so this portfolio's beta 123 would be: 124 125 Portfolio beta Arial 10 Wrap Text I USA Paste B EE EEE Merge & Center AS X Also, you cannot calculate the rate of return for 2014 because you do not have 2013 data.) D F G H 5 6. Use the data given to calculate annual returns for Goodman, Landry, and the Market Index, and then 7 calculate average returns over the five year period. Mint Remember, returns are calculated by subtracting 8 the beginning price from the ending price to get the capital gain or loss, adding the dividend to the capital gain 9 or loss, and dividing the result by the beginning price. Assume that dividends are already included in the 10 Index. Also, you cannot calculate the rate of return for 2014 because you do not have 2013 data.) 12 Data as given in the problem are shown below 13 Goodman Industries Landry Incorporated Market Index Yearl Stock Price Dividend | Stock Price Dividend includes Divs 15 2019 $25 88 $1.73 $73.13 $4.50 16 17.495.97 2018 $22.13 $1.59 $78.45 $4.35 17 2017 13,178.55 $24.75 $1.50 $73.13 $4.13 13,019.97 18 2018 $16.13 $85 88 $3.75 9,651.05 19 2015 $17.06 $1,35 $90.00 $3.38 20 2014 8.403.42 $11.44 $1.28 $83.63 $3.00 7058.90 21 22 We now calculate the rates of retum for the two companies and the Index 23 24 Goodman 25 Index 2019 26 2018 27 2017 28 2016 29 2015 30 31 Average 32 1.43 33 Note: To get the average, you could get the column sumand divide by 5, but you could use the function 34 wirard, 1x Click then statistical, then Average, and then use the mouse to the proper range. Do this for 35 Goodman and then copy the col for the other bem 37 b. Calculate the standard deviation of the returns for Goodman, Landry, and the Market Index. Mint Use the 38 sample standard deviation formula given in the chapter, which corresponds to the STDEV Hunction in Excel) 40 Use the function wizard to calculate the standard deviations Goodman 43 Standard deviation of retums Index 45 46 Build a Model Edit 5 MacBook F esc New Window New Private Window wage & Center w AS x Fx Also, you cannot calculate the rate of return for 2014 because you do not have 2013 data.) C 47 c. Construct a scatter diagram graph that shows Goodman's and Landry returns on the vertical axis and the 48 Market Index's returns on the horizontal axis. 49 50 it is easiest to make scatter diagrams with a data set that has the X-axis variable in the left column 51 so we reformat the retums data calculated above and show it just below. 52 53 Year Index Goodman Landry 54 2019 0.0% 0.0% 0.0% 55 2018 0.0% 0.0% 0.0% 56 2017 0.0% 0.0% 0.0% 57 2016 0.0% 0.0% 0.0% 58 2015 0.0% 0.0% 0.0% 59 60 61 62 63 64 65 66 67 68 69 70 71 72 73 74 75 76 To make the graph, we first selected the range with the retums and the column heads, then clicked the chart wizard 77 then choose the scatter diagram without connected lines. That gave us the data points. We then used the drawing 78 toolbar to make free hand by eye") regression lines, and changed the lines color and weights to match the dots 79 80 81 82 83 d. Estimate Goodman's and Landry's betas as the slopes of regression lines with stock returns on the 84 vertical axis y-axis) and market return on the horizontal axis (x-axis). (Hint: use Excel's SLOPE function) 85 Are these betas consistent with your graph? 86 87 Goodman's beta- 88 89 Landry' beta- Build a Model Edit 10 Wrap Text v Uw w MA Paste I Conditional Format Formatting as Table EEEEE Merge al Center K AS X Also, you cannot calculate the rate of return for 2014 because you do not have 2013 data.) D E H TUTUTRUSTNICTWU EROLO CORE 85 Are these betas consistent with your graph? 88 87 Goodman's beta- 89 89 Landry beta- 90 91 92 93 94 95. The risk tree rate on long-term Treasury bonds is 6.04%. Assume that the market risk premium is 5%. What is the 96 expected return on the market? Now use the SML equation to calculate the two companies' required returns 98 Market risk premium (RP) = 5.000% 99 Risk-tree rate 6.040% 100 101 Expected retum on market Risk-free rate Market is premium 102 6.040% 5,000% 103 11.040% 104 105 Required retum 106 107 Goodman: 108 Required retum 109 110 111 Landry 112 Required retum 113 114 115 116 117 118 119 If you formed a portfolio that consisted of 50% Goodman stock and 50% Landry stock, what would be its 120 beta and its required return? 121 122 The beta of a portfolio is simply a weighted average of the beas of the stocks in the portfolio, so this portfolo's beta 123 would be: 124 125 Portfolio beta- 126 197 Build a Model + Edit A5 X Vfx Also, you cannot calculate the rate of return for 2014 because you do not have 2013 data G H 129 - B D E F TCU 127 9. Suppose an investor wants to include Goodman Industries' stock in his or her portfolio. Stocks A, B, and C 128 are currently in the portfolio, and their betas are 0.769, 0.985, and 1.423, respectively. Calculate the new portfolio's required return if it consists of 25% of Goodman, 15% of Stock A, 40% of Stock B, and 20% of 130 Stock C. 131 132 133 Beta Portfolio Weight 134 Goodman 25% 135 Stock A 0.769 15% 136 Stock B 0.985 40% 137 Stock C 1.423 20% 138 100% 139 Portfolio Beta - 140 141 Required retum on portfolio: Risk-free rate + Market Risk Premium Beta 142 143 144 145 146 147 148 149 150 151 152 153 154 155 156 157 158 159 160 161 = G H B Esu una sau mury SUSITOUDUTOSWIUT STUCKTUUTTIS TU vertical axis ly-axis) and market return on the horizontal axis ( xxls). (Hint: Uso Excel's SLOPE function.) Are these betas consistent with your graph? Goodman's beta Landry' beta - D. The risk-free rate on long-term Treasury bonds is 6.04%. Assume that the market risk premium is 5%. What is the expected return on the market? Now use the SML equation to calculate the two companies' required returns. 3 Market risk premium (RP) = 5.000% Risk-free rate = 6.040% 10 1 Expected retum on market = Risk-free rate Market risk premium 02 6.040% 5.000% 03 11.040% 34 05 Required retum 06 07 Goodman: 0B Required retum 09 10 11 Landry: 112 Required retum 113 14 115 116 117 118 119. If you formed a portfolio that consisted of 50% Goodman stock and 50% Landry stock, what would be its 120 beta and its required return? 121 122 The beta of a portfolio is simply a weighted average of the betas of the stocks in the portfolio, so this portfolio's beta 123 would be: 124 125 Portfolio beta