Answered step by step

Verified Expert Solution

Question

1 Approved Answer

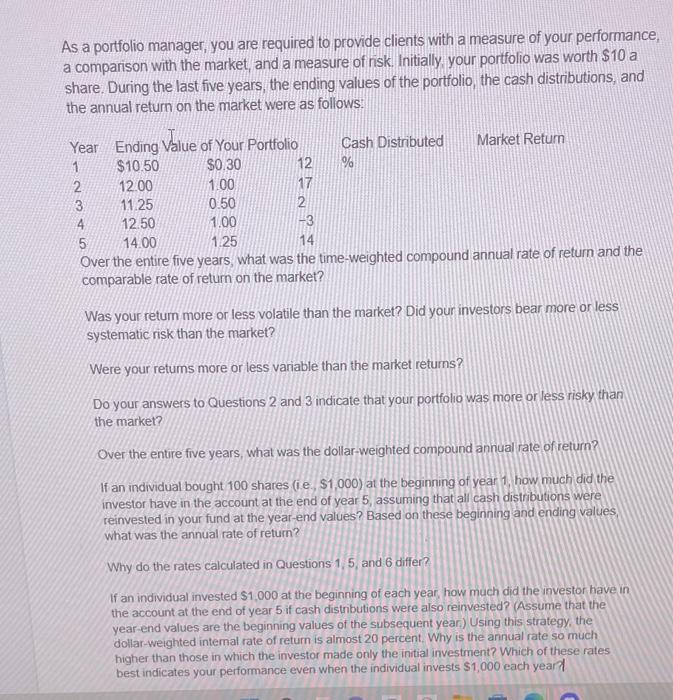

As a portfolio manager, you are required to provide clients with a measure of your performance, a comparison with the market and a measure of

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Environment And Business Development Proceedings Of The 16th Eurasia Business And Economics Society Conference

Authors: Mehmet Huseyin Bilgin , Hakan Danis , Ender Demir , Ugur Can

1st Edition

3319399187,3319399195