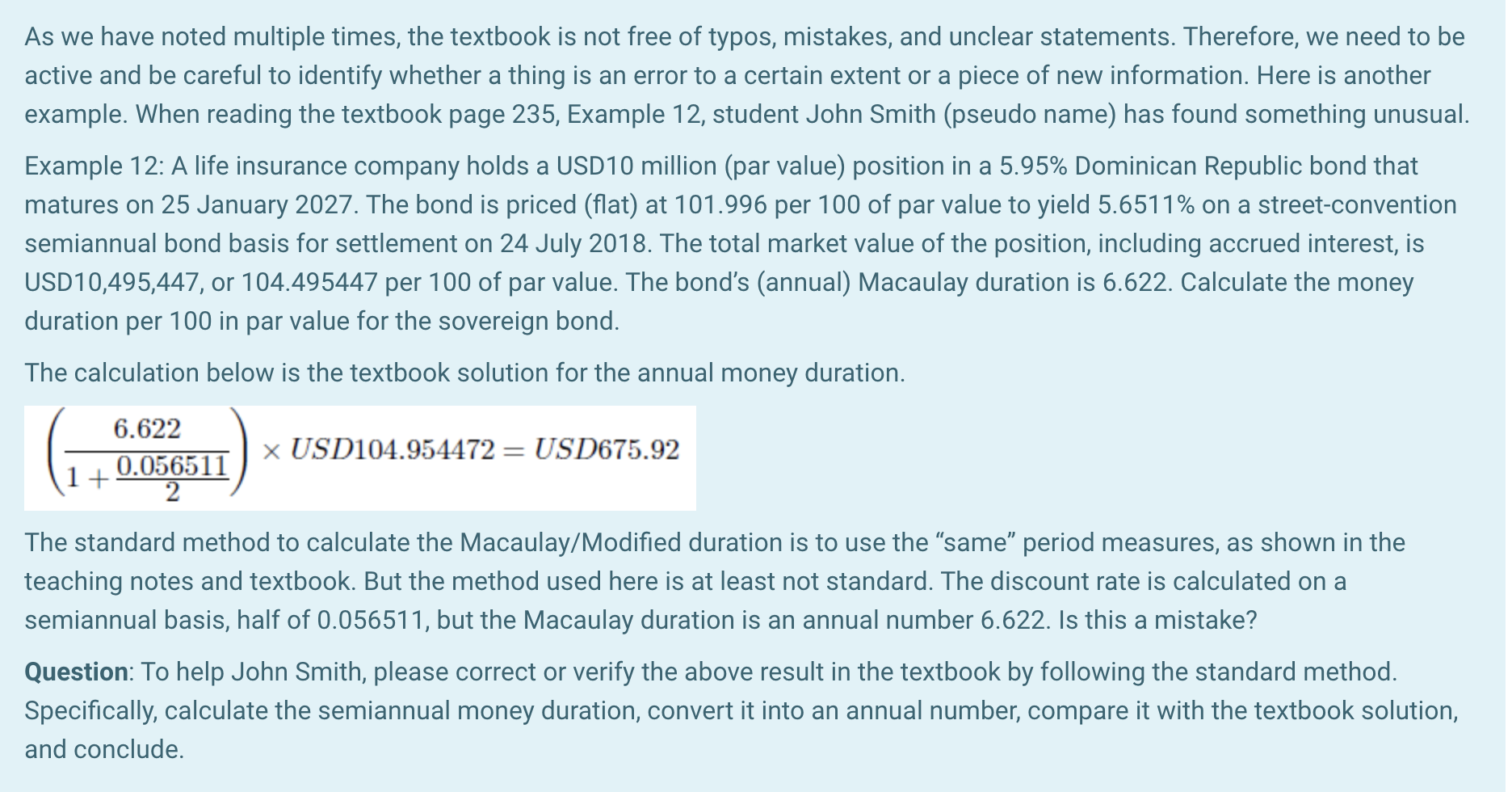

As we have noted multiple times, the textbook is not free of typos, mistakes, and unclear statements. Therefore, we need to be active and be careful to identify whether a thing is an error to a certain extent or a piece of new information. Here is another example. When reading the textbook page 235, Example 12, student John Smith (pseudo name) has found something unusual. Example 12: A life insurance company holds a USD10 million (par value) position in a 5.95% Dominican Republic bond that matures on 25 January 2027. The bond is priced (flat) at 101.996 per 100 of par value to yield 5.6511% on a street-convention semiannual bond basis for settlement on 24 July 2018. The total market value of the position, including accrued interest, is USD10,495,447, or 104.495447 per 100 of par value. The bond's (annual) Macaulay duration is 6.622. Calculate the money duration per 100 in par value for the sovereign bond. The calculation below is the textbook solution for the annual money duration. 6.622 1+ 0.056511 2 X USD104.954472 = USD675.92 The standard method to calculate the Macaulay/Modified duration is to use the same period measures, as shown in the teaching notes and textbook. But the method used here is at least not standard. The discount rate is calculated on a semiannual basis, half of 0.056511, but the Macaulay duration is an annual number 6.622. Is this a mistake? Question: To help John Smith, please correct or verify the above result in the textbook by following the standard method. Specifically, calculate the semiannual money duration, convert it into an annual number, compare it with the textbook solution, and conclude. As we have noted multiple times, the textbook is not free of typos, mistakes, and unclear statements. Therefore, we need to be active and be careful to identify whether a thing is an error to a certain extent or a piece of new information. Here is another example. When reading the textbook page 235, Example 12, student John Smith (pseudo name) has found something unusual. Example 12: A life insurance company holds a USD10 million (par value) position in a 5.95% Dominican Republic bond that matures on 25 January 2027. The bond is priced (flat) at 101.996 per 100 of par value to yield 5.6511% on a street-convention semiannual bond basis for settlement on 24 July 2018. The total market value of the position, including accrued interest, is USD10,495,447, or 104.495447 per 100 of par value. The bond's (annual) Macaulay duration is 6.622. Calculate the money duration per 100 in par value for the sovereign bond. The calculation below is the textbook solution for the annual money duration. 6.622 1+ 0.056511 2 X USD104.954472 = USD675.92 The standard method to calculate the Macaulay/Modified duration is to use the same period measures, as shown in the teaching notes and textbook. But the method used here is at least not standard. The discount rate is calculated on a semiannual basis, half of 0.056511, but the Macaulay duration is an annual number 6.622. Is this a mistake? Question: To help John Smith, please correct or verify the above result in the textbook by following the standard method. Specifically, calculate the semiannual money duration, convert it into an annual number, compare it with the textbook solution, and conclude