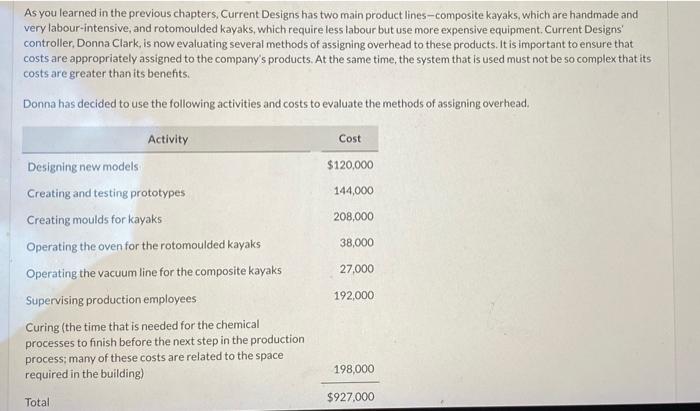

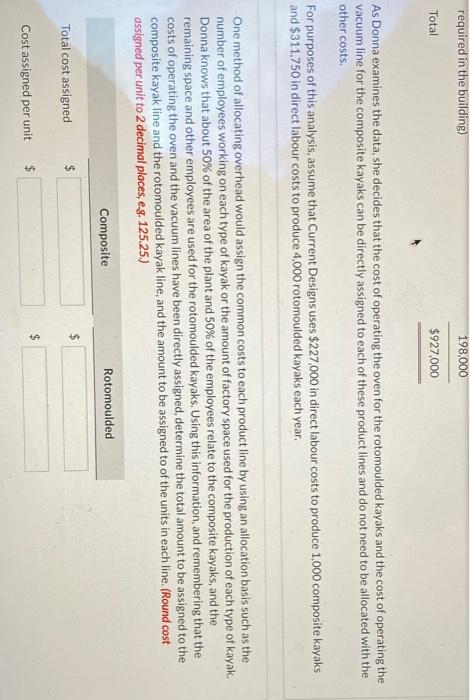

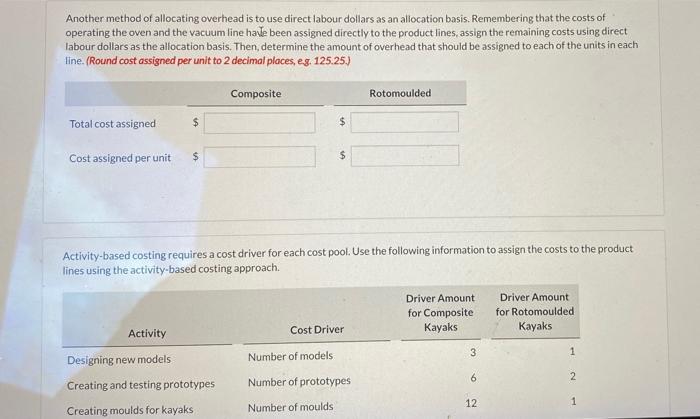

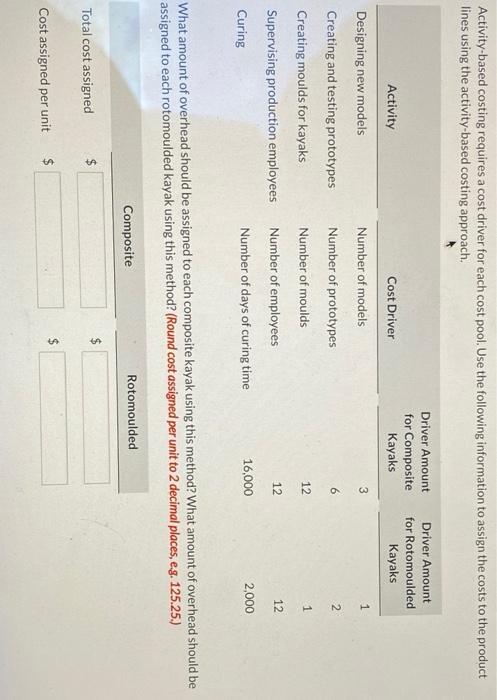

As you learned in the previous chapters, Current Designs has two main product lines-composite kayaks, which are handmade and very labour-intensive, and rotomoulded kayaks, which require less labour but use more expensive equipment Current Designs controller, Donna Clark, is now evaluating several methods of assigning overhead to these products. It is important to ensure that costs are appropriately assigned to the company's products. At the same time, the system that is used must not be so complex that its costs are greater than its benefits. Donna has decided to use the following activities and costs to evaluate the methods of assigning overhead. Cost $120,000 144,000 208,000 38,000 Activity Designing new models Creating and testing prototypes Creating moulds for kayaks Operating the oven for the rotomoulded kayaks Operating the vacuum line for the composite kayaks Supervising production employees Curing (the time that is needed for the chemical processes to finish before the next step in the production process; many of these costs are related to the space required in the building) 27.000 192,000 198,000 Total $927.000 required in the building) 198,000 Total $927,000 As Donna examines the data, she decides that the cost of operating the oven for the rotomoulded kayaks and the cost of operating the vacuum line for the composite kayaks can be directly assigned to each of these product lines and do not need to be allocated with the other costs. For purposes of this analysis, assume that Current Designs uses $227,000 in direct labour costs to produce 1,000 composite kayaks and $311,750 in direct labour costs to produce 4,000 rotomoulded kayaks each year, One method of allocating overhead would assign the common costs to each product line by using an allocation basis such as the number of employees working on each type of kayak or the amount of factory space used for the production of each type of kayak. Donna knows that about 50% of the area of the plant and 50% of the employees relate to the composite kayaks, and the remaining space and other employees are used for the rotomoulded kayaks. Using this information, and remembering that the costs of operating the oven and the vacuum lines have been directly assigned, determine the total amount to be assigned to the composite kayak line and the rotomoulded kayak line, and the amount to be assigned to of the units in each line. (Round cost assigned per unit to 2 decimal places, eg. 125.25.) Composite Rotomoulded $ $ Total cost assigned $ $ Cost assigned per unit Another method of allocating overhead is to use direct labour dollars as an allocation basis. Remembering that the costs of operating the oven and the vacuum line have been assigned directly to the product lines, assign the remaining costs using direct labour dollars as the allocation basis. Then, determine the amount of overhead that should be assigned to each of the units in each line. (Round cost assigned per unit to 2 decimal places, eg. 125.25.) Composite Rotomoulded Total cost assigned $ $ Cost assigned per unit $ $ Activity-based costing requires a cost driver for each cost pool. Use the following information to assign the costs to the product lines using the activity-based costing approach. Driver Amount for Composite Kayaks Driver Amount for Rotomoulded Kayaks Cost Driver 3 1 Number of models Activity Designing new models Creating and testing prototypes Creating moulds for kayaks 6 2 Number of prototypes 12 1 Number of moulds Activity-based costing requires a cost driver for each cost pool. Use the following information to assign the costs to the product lines using the activity-based costing approach. Driver Amount for Composite Kayaks Driver Amount for Rotomoulded Kayaks Activity Cost Driver Designing new models 3 1 Creating and testing prototypes Number of models Number of prototypes Number of moulds 6 2 12 1 Creating moulds for kayaks Supervising production employees 12 12 Number of employees Number of days of curing time Curing 16,000 2,000 What amount of overhead should be assigned to each composite kayak using this method? What amount of overhead should be assigned to each rotomoulded kayak using this method (Round cost assigned per unit to 2 decimal places, eg. 125.25.) Composite Rotomoulded $ Total cost assigned $ Cost assigned per unit $