Question

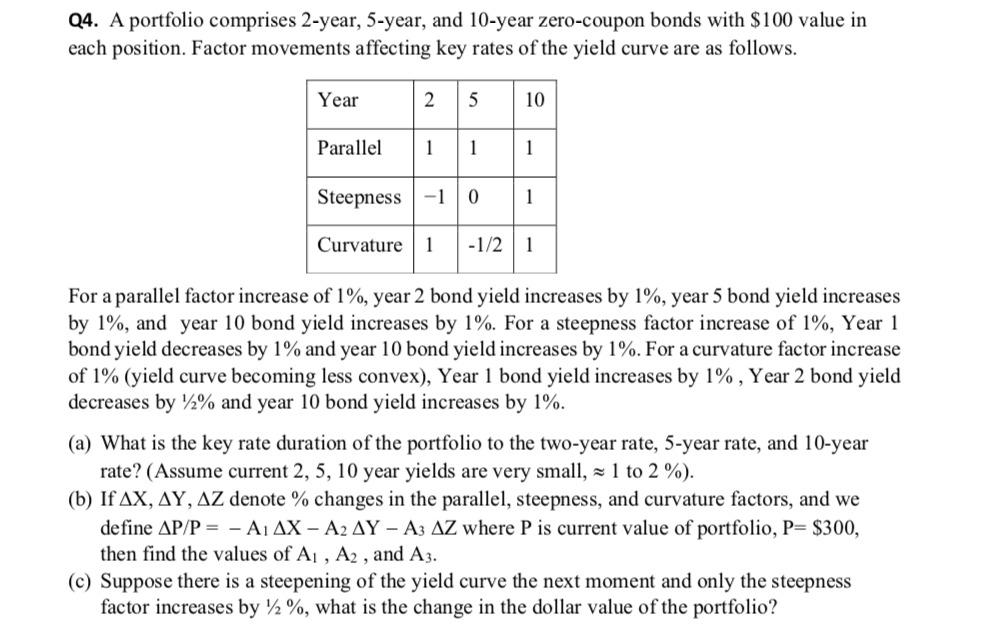

ASAP Q4. A portfolio comprises 2-year, 5-year, and 10-year zero-coupon bonds with $ 100 value in each position. Factor movements affecting key rates of the

ASAP Q4. A portfolio comprises 2-year, 5-year, and 10-year zero-coupon bonds with $ 100 value in each position. Factor movements affecting key rates of the yield curve are as follows. Year 2 5 10 5 Parallel 1 1 1 Steepness -1 0 1 Curvature 1 -1/21 For a parallel factor increase of 1%, year 2 bond yield increases by 1%, year 5 bond yield increases by 1%, and year 10 bond yield increases by 1%. For a steepness factor increase of 1%, Year 1 bond yield decreases by 1% and year 10 bond yield increases by 1%. For a curvature factor increase of 1% (yield curve becoming less convex), Year 1 bond yield increases by 1% , Year 2 bond yield decreases by 12% and year 10 bond yield increases by 1%. (a) What is the key rate duration of the portfolio to the two-year rate, 5-year rate, and 10-year rate? (Assume current 2, 5, 10 year yields are very small, = 1 to 2 %). (b) If AX, AY, AZ denote % changes in the parallel, steepness, and curvature factors, and we define AP/P = - AJAX - A2 AY - A3 AZ where P is current value of portfolio, P= $300, then find the values of Al , A2 , and A3. (C) Suppose there is a steepening of the yield curve the next moment and only the steepness factor increases by 12%, what is the change in the dollar value of the portfolio? Q4. A portfolio comprises 2-year, 5-year, and 10-year zero-coupon bonds with $ 100 value in each position. Factor movements affecting key rates of the yield curve are as follows. Year 2 5 10 5 Parallel 1 1 1 Steepness -1 0 1 Curvature 1 -1/21 For a parallel factor increase of 1%, year 2 bond yield increases by 1%, year 5 bond yield increases by 1%, and year 10 bond yield increases by 1%. For a steepness factor increase of 1%, Year 1 bond yield decreases by 1% and year 10 bond yield increases by 1%. For a curvature factor increase of 1% (yield curve becoming less convex), Year 1 bond yield increases by 1% , Year 2 bond yield decreases by 12% and year 10 bond yield increases by 1%. (a) What is the key rate duration of the portfolio to the two-year rate, 5-year rate, and 10-year rate? (Assume current 2, 5, 10 year yields are very small, = 1 to 2 %). (b) If AX, AY, AZ denote % changes in the parallel, steepness, and curvature factors, and we define AP/P = - AJAX - A2 AY - A3 AZ where P is current value of portfolio, P= $300, then find the values of Al , A2 , and A3. (C) Suppose there is a steepening of the yield curve the next moment and only the steepness factor increases by 12%, what is the change in the dollar value of the portfolio

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Understanding ETF Options Profitable Strategies For Diversified Low Risk Investing

Authors: Kenneth R. Trester

1st Edition

007176030X, 0071760431, 9780071760430