Answered step by step

Verified Expert Solution

Question

1 Approved Answer

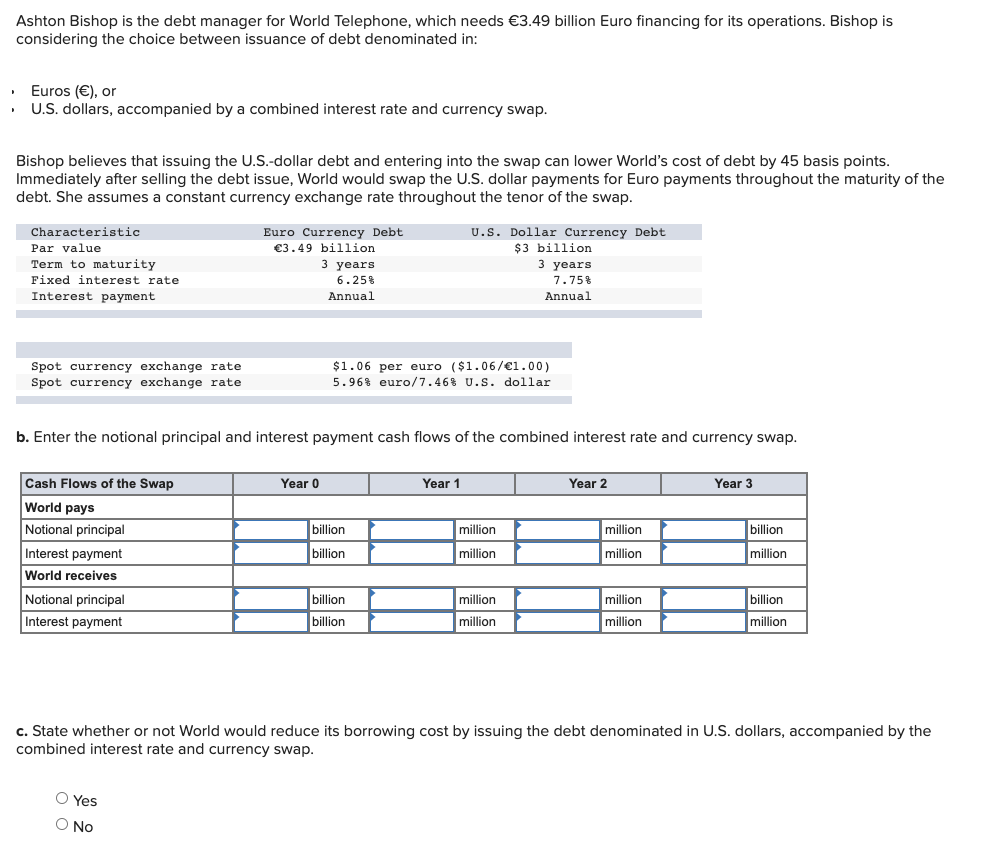

Ashton Bishop is the debt manager for World Telephone, which needs 3.49 billion Euro financing for its operations. Bishop is considering the choice between issuance

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Public Private Partnership Handbook

Authors: Malcolm Morley

1st Edition

0749474262, 978-0749474263