assap tutors help me solve this question

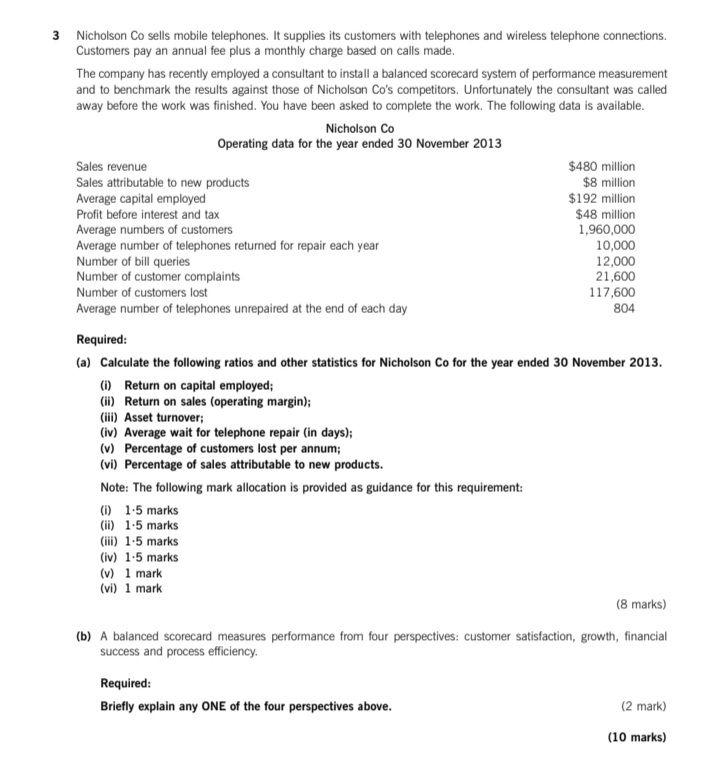

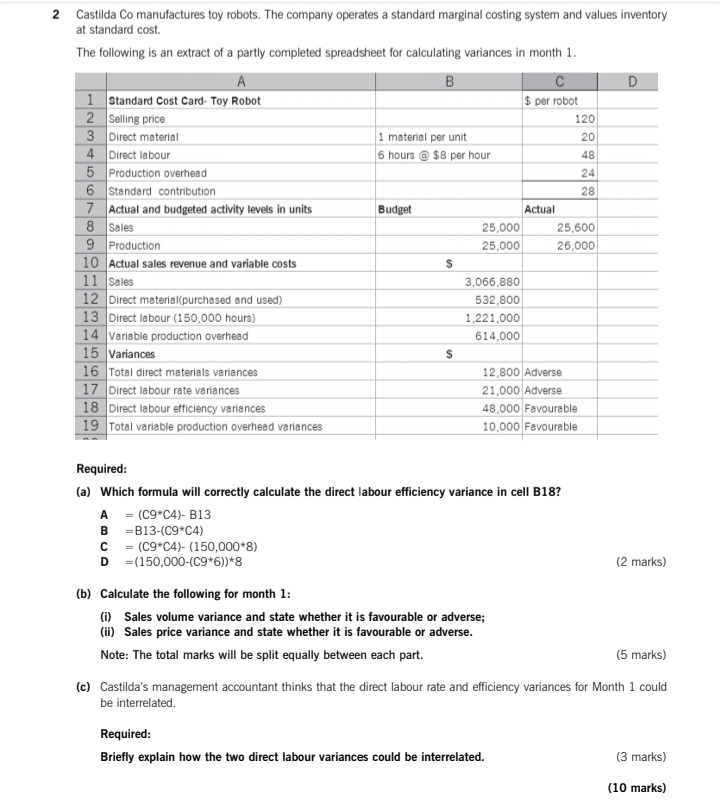

3 Nicholson Co sells mobile telephones. It supplies its customers with telephones and wireless telephone connections. Customers pay an annual fee plus a monthly charge based on calls made. The company has recently employed a consultant to install a balanced scorecard system of performance measurement and to benchmark the results against those of Nicholson Co's competitors. Unfortunately the consultant was called away before the work was finished. You have been asked to complete the work. The following data is available. Nicholson Co Operating data for the year ended 30 November 2013 Sales revenue $480 million Sales attributable to new products $8 million Average capital employed $192 million Profit before interest and tax $48 million Average numbers of customers 1,960,000 Average number of telephones returned for repair each year 10,000 Number of bill queries 12,000 Number of customer complaints 21,600 Number of customers lost 117,600 Average number of telephones unrepaired at the end of each day 804 Required: (a) Calculate the following ratios and other statistics for Nicholson Co for the year ended 30 November 2013. (i) Return on capital employed (ii) Return on sales (operating margin); (iii) Asset turnover; (iv) Average wait for telephone repair (in days); (v) Percentage of customers lost per annum; (vi) Percentage of sales attributable to new products. Note: The following mark allocation is provided as guidance for this requirement: (i) 1.5 marks (ii) 1.5 marks (ili) 1.5 marks (iv) 1.5 marks (v) 1 mark (vi) 1 mark (8 marks) (b) A balanced scorecard measures performance from four perspectives: customer satisfaction, growth, financial success and process efficiency. Required: Briefly explain any ONE of the four perspectives above. (2 mark) (10 marks)2 Castilda Co manufactures toy robots. The company operates a standard marginal costing system and values inventory at standard cost. The following is an extract of a partly completed spreadsheet for calculating variances in month 1. B C D Standard Cost Card- Toy Robot $ per robot 2 Selling price 120 3 Direct material 1 material per unit 20 4 Direct labour 6 hours @ $8 per hour 48 5 Production overhead 24 6 Standard contribution 28 7 Actual and budgeted activity levels in units Budget Actual 8 Sales 25,000 25,600 Production 25,000 26,000 10 Actual sales revenue and variable costs S 1 1 Sales 3,066,880 12 Direct material(purchased and used) 532,800 13 Direct labour (150,000 hours) 1,221,000 14 Variable production overhead 614,000 15 Variances S 16 Total direct materials variances 12,800 Adverse 17 Direct labour rate variances 21,000 Adverse 18 Direct labour efficiency variances 48,000 Favourable 19 Total variable production overhead variances 10,000 Favourable Required: (a) Which formula will correctly calculate the direct labour efficiency variance in cell B18? = (C9*C4)- B13 =B13-(C9*C4) = (C9*C4)- (150,000*8) D =(150,000-(C9*6))*8 (2 marks) (b) Calculate the following for month 1: Sales volume variance and state whether it is favourable or adverse; (ii) Sales price variance and state whether it is favourable or adverse. Note: The total marks will be split equally between each part. (5 marks) (c) Castilda's management accountant thinks that the direct labour rate and efficiency variances for Month 1 could be interrelated. Required: Briefly explain how the two direct labour variances could be interrelated. (3 marks) (10 marks)