Assess DPC's fit within DuPont. What are its prospects going forward as a division within DuPont...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

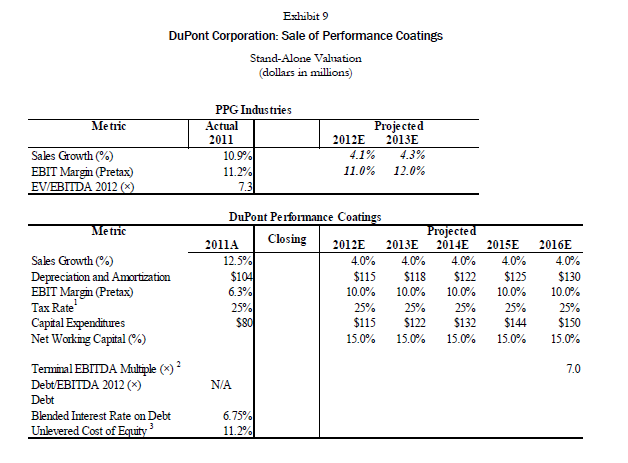

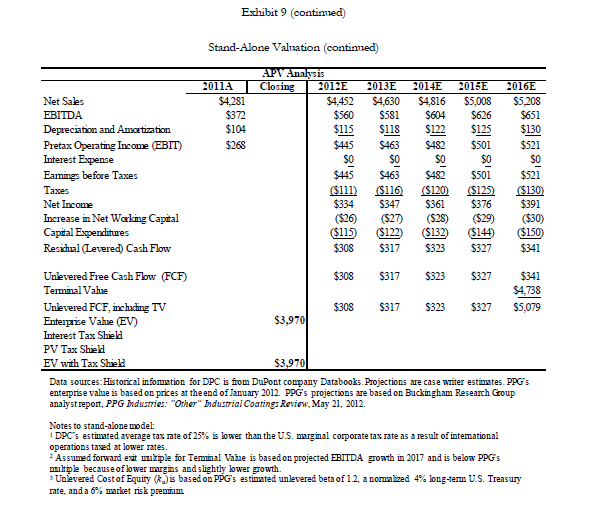

Assess DPC's fit within DuPont. What are its prospects going forward as a division within DuPont versus its potential value to an outside party? 2. How attractive is DPC as an acquisition from a strategic buyer's or PE firm's perspective? What are the potential risks to such a deal? What are some of the important features of APV, and why is it a useful approach for valuing an LBO? 3. Working from case Exhibit 9. relative to the stand-alone value, estimate the dollar increase in DPC's value if a PE fund can obtain: a. 5% revenue growth per annum (versus 4% growth) in each of the next five years and improve the operating margin to 12% (versus 10%). b. Assume part a and that the division can be sold at 7.5x EBITDA in five years. c. Assume part a and part b and that debt financing equal to 6.0x forward EBITDA can be obtained. Assume that all cash available to pay debt each year (i.e., residual cash flow) is used to pay down the LBO debt and that, after five years, the firm will revert to an all-equity firm. d. What are some of the advantages and risks of using leverage to finance the investment? 4. If a PE sponsor has a target return of 20% on its funds (equity contribution), what is the maximum enterprise value it can offer for DPC under parts b and c above? What minimum bid should Ellen Kullman set if she chooses to sell DPC? Exhibit 9 DuPont Corporation: Sale of Performance Coatings Stand-Alone Valuation (dollars in millions) PPG Industries Metric Actual 2011 Sales Growth (%) 10.9% EBIT Margin (Pretax) EV/EBITDA 2012 (x) 11.2% 7.3 2012E Projected 2013E 4.1% 4.3% 11.0% 12.0% DuPont Performance Coatings Metric Projected 2011A Closing 2012E 2013E 2014E 2015E 2016E Sales Growth (%) 12.5% 4.0% 4.0% 4.0% 4.0% 4.0% Depreciation and Amortization $104 $115 $118 $122 $125 $130 EBIT Margin (Pretax) 6.3% 10.0% 10.0% 10.0% 10.0% 10.0% Tax Rate 25% 25% 25% 25% 25% 25% Capital Expenditures $80 $115 $122 $132 $144 $150 Net Working Capital (%) 15.0% 15.0% 15.0% 15.0% 15.0% Terminal EBITDA Multiple (*) 2 7.0 Debt/EBITDA 2012 (*) N/A Debt Blended Interest Rate on Debt 6.75% Unlevered Cost of Equity³ 11.2% Exhibit 9 (continued) Stand-Alone Valuation (continued) APV Analysis 2011A Closing 2012E 2013E 2014E 2015E 2016E Net Sales $4,281 $4,452 $4,630 $4,816 $5,008 $5,208 EBITDA $372 $560 $581 $604 $626 $651 Depreciation and Amortization $104 $115 $118 $122 $125 $130 Pretax Operating Income (EBIT) $268 $445 $463 $482 $501 $521 Interest Expense $0 $0 $0 Eamings before Taxes $445 $463 $482 $501 $521 Taxes ($111) ($116) ($120) ($125) ($130) Net Income $334 $347 $361 $376 $391 Increase in Net Working Capital ($26) ($27) ($28) ($29) ($30) Capital Expenditures ($115) ($122) ($132) ($144) ($150) Residual (Levered) Cash Flow $308 $317 $323 $327 $341 Unlevered Free Cash Flow (FCF) $308 $317 $323 $327 $341 Terminal Value $4,738 Unlevered FCF, including TV $308 $317 $323 $327 $5,079 Enterprise Value (EV) $3,970 Interest Tax Shield PV Tax Shield EV with Tax Shield $3,970 Data sources: Historical information for DPC is from DuPont company Databooks. Projections are case writer estimates. PPG's enterprise value is based on prices at the end of January 2012. PPG's projections are based on Buckingham Research Group analyst report, PPG Industries: "Other" Industrial Coatings Review, May 21, 2012. Notes to stand-alone model DPC's estimated average tax rate of 25% is lower than the US. marginal corporate tax rate as a result of international operations taxed at lower rates. * Assumed forward exit multiple for Terminal Value is based on projected EBITDA growth in 2017 and is below PPG's multiple because of lower margins and slightly lower growth. 3 Unlevered Cost of Equity (*) is based on PPG's estimated unlevered beta of 1.2, a normalized 4% long-term U.S. Treasury rate, and a 6% market risk premium Assess DPC's fit within DuPont. What are its prospects going forward as a division within DuPont versus its potential value to an outside party? 2. How attractive is DPC as an acquisition from a strategic buyer's or PE firm's perspective? What are the potential risks to such a deal? What are some of the important features of APV, and why is it a useful approach for valuing an LBO? 3. Working from case Exhibit 9. relative to the stand-alone value, estimate the dollar increase in DPC's value if a PE fund can obtain: a. 5% revenue growth per annum (versus 4% growth) in each of the next five years and improve the operating margin to 12% (versus 10%). b. Assume part a and that the division can be sold at 7.5x EBITDA in five years. c. Assume part a and part b and that debt financing equal to 6.0x forward EBITDA can be obtained. Assume that all cash available to pay debt each year (i.e., residual cash flow) is used to pay down the LBO debt and that, after five years, the firm will revert to an all-equity firm. d. What are some of the advantages and risks of using leverage to finance the investment? 4. If a PE sponsor has a target return of 20% on its funds (equity contribution), what is the maximum enterprise value it can offer for DPC under parts b and c above? What minimum bid should Ellen Kullman set if she chooses to sell DPC? Exhibit 9 DuPont Corporation: Sale of Performance Coatings Stand-Alone Valuation (dollars in millions) PPG Industries Metric Actual 2011 Sales Growth (%) 10.9% EBIT Margin (Pretax) EV/EBITDA 2012 (x) 11.2% 7.3 2012E Projected 2013E 4.1% 4.3% 11.0% 12.0% DuPont Performance Coatings Metric Projected 2011A Closing 2012E 2013E 2014E 2015E 2016E Sales Growth (%) 12.5% 4.0% 4.0% 4.0% 4.0% 4.0% Depreciation and Amortization $104 $115 $118 $122 $125 $130 EBIT Margin (Pretax) 6.3% 10.0% 10.0% 10.0% 10.0% 10.0% Tax Rate 25% 25% 25% 25% 25% 25% Capital Expenditures $80 $115 $122 $132 $144 $150 Net Working Capital (%) 15.0% 15.0% 15.0% 15.0% 15.0% Terminal EBITDA Multiple (*) 2 7.0 Debt/EBITDA 2012 (*) N/A Debt Blended Interest Rate on Debt 6.75% Unlevered Cost of Equity³ 11.2% Exhibit 9 (continued) Stand-Alone Valuation (continued) APV Analysis 2011A Closing 2012E 2013E 2014E 2015E 2016E Net Sales $4,281 $4,452 $4,630 $4,816 $5,008 $5,208 EBITDA $372 $560 $581 $604 $626 $651 Depreciation and Amortization $104 $115 $118 $122 $125 $130 Pretax Operating Income (EBIT) $268 $445 $463 $482 $501 $521 Interest Expense $0 $0 $0 Eamings before Taxes $445 $463 $482 $501 $521 Taxes ($111) ($116) ($120) ($125) ($130) Net Income $334 $347 $361 $376 $391 Increase in Net Working Capital ($26) ($27) ($28) ($29) ($30) Capital Expenditures ($115) ($122) ($132) ($144) ($150) Residual (Levered) Cash Flow $308 $317 $323 $327 $341 Unlevered Free Cash Flow (FCF) $308 $317 $323 $327 $341 Terminal Value $4,738 Unlevered FCF, including TV $308 $317 $323 $327 $5,079 Enterprise Value (EV) $3,970 Interest Tax Shield PV Tax Shield EV with Tax Shield $3,970 Data sources: Historical information for DPC is from DuPont company Databooks. Projections are case writer estimates. PPG's enterprise value is based on prices at the end of January 2012. PPG's projections are based on Buckingham Research Group analyst report, PPG Industries: "Other" Industrial Coatings Review, May 21, 2012. Notes to stand-alone model DPC's estimated average tax rate of 25% is lower than the US. marginal corporate tax rate as a result of international operations taxed at lower rates. * Assumed forward exit multiple for Terminal Value is based on projected EBITDA growth in 2017 and is below PPG's multiple because of lower margins and slightly lower growth. 3 Unlevered Cost of Equity (*) is based on PPG's estimated unlevered beta of 1.2, a normalized 4% long-term U.S. Treasury rate, and a 6% market risk premium

Expert Answer:

Answer rating: 100% (QA)

Assessing DPCs fit within DuPont and its prospects as a division within DuPont versus its potential value to an outside party To assess DPCs fit within DuPont you would need to consider factors such a... View the full answer

Related Book For

Advanced Financial Accounting

ISBN: 978-0137030385

6th edition

Authors: Thomas Beechy, Umashanker Trivedi, Kenneth MacAulay

Posted Date:

Students also viewed these finance questions

-

2. Reference the figure of a rectangular plate with forces applied at corners A and C. y 1 151bl a) (10 points) Determine the magnitude and the direction of the moment due to the applied force...

-

E For each of the cases below, draw the band edge diagram at equilibrium, label it an appropriate name, and sketch the current-voltage response. A vacuum level is drawn for reference, as well as a...

-

Managing Scope Changes Case Study Scope changes on a project can occur regardless of how well the project is planned or executed. Scope changes can be the result of something that was omitted during...

-

Avid Corporation manufactures a sophisticated controller that is compatible with a variety of gaming consoles. Excluding rework costs, the cost of manufacturing one controller is $ 220. This consists...

-

According to Noam Chomsky what potential problem did Aristotle and James Madison see with a "perfect democracy" if there were great extremes between the poor and rich? What solution did each favor?

-

Under Armour, Inc., was founded in 1996 by Kevin Plank, a 23-year-old former University of Maryland football player. The company specializes in manufacturing and selling athletic and casual apparel...

-

What difference is there between a big dividend payout and a share buyback of the same amount (a) for the company? (b) for the shareholders?

-

Strudler Real Estate, Inc., a construction firm financed by both debt and equity, is undertaking a new project. If the project is successful, the value of the firm in one year will be $280 million,...

-

Independence may be impaired when a partner leaves an audit firm and is subsequently employed by the client if Multiple Choice ( ) amounts due the former partner are not material to the firm. ( )...

-

Alexander Smith and his wife Allison are married and file a joint tax return for 2021. The Smiths live at 1234 Buena Vista Drive, Orlando, FL 32830. Alexander is a commuter airline pilot but took 6...

-

Below shown binary phase diagram describes the system Sn-Bi. T (C) 300- 250- 200- 150- 100- 50- 0+ 0 Sn B X 3 N Y 10 20 30 40 50 60 70 80 90 100 Mass % Bi Bi a) Which phases are present in areas W,...

-

Topic: Continuous Readiness Risks Describe the risks to individual employees and organizations that do not participate in continuous readiness efforts. Include one real-world example of a risk from...

-

How can educators recognise and use opportunities throughout the day to encourage children to share their thoughts and ideas about environmental responsibility? Consider spontaneous teaching...

-

Explain the concept of equity in financial accounting, detailing its significance within the broader framework of a company's financial structure and its relation to ownership and claims on assets....

-

What are the actions that California has taken towards energy transition (to achieve 100% clean energy) as well as the incumbents, challengers, major policy they intend to enact, etc. Propose a...

-

difference in access controls among private industries, such as retail, banking, and manufacturing?

-

Bond P is a premium bond with a coupon of 6.4 percent, a YTM of 5.15 percent, and 15 years to maturity. Bond D is a discount bond with a coupon of 6.4 percent and a YTM of 8.15 percent, and also has...

-

Evaluate the line integral, where C is the given curve. C x 2 dx + y 2 dy, C consists of the arc of the circle x 2 + y 2 = 4 from (2, 0) to (0, 2) followed by the line segment from (0, 2) to (4, 3)

-

When a fair-valued asset is sold by a subsidiary to its parent, how does the amount of the fair-value increment affect the unrealized profit elimination?

-

South Ltd. acquired 100% of the voting shares of North Ltd. In exchange, South Ltd. issued 50,000 common shares, with a market value of $ 10 per share, to the common shareholders of North Ltd. Both...

-

On January 1, 20X2, Porter Inc. purchased 80% of the outstanding voting shares of Sloan Ltd. for $ 3,000,000 in cash. On this date, Sloan had common shares outstanding in the amount of $ 2,200,000...

-

Kayjay Inc., which produces a single product, has prepared the following standard cost sheet for one unit of the product. Direct materials (8 pounds at \($2.50\) per pound) \($20.00\) Direct labor (3...

-

Kimiko Company's standard labor cost per unit of output is $ 1 8 (2 hours X \($9.00\) per hour). During August, the company incurs 1,850 hours of direct labor at an hourly cost of \($9.60\) per hour...

-

The standard cost of Product B manufactured by Lopez Company includes three units of direct materials at $5.00 per unit. During June, 30,000 units of direct materials are purchased at a cost of $4.80...

Study smarter with the SolutionInn App