Answered step by step

Verified Expert Solution

Question

1 Approved Answer

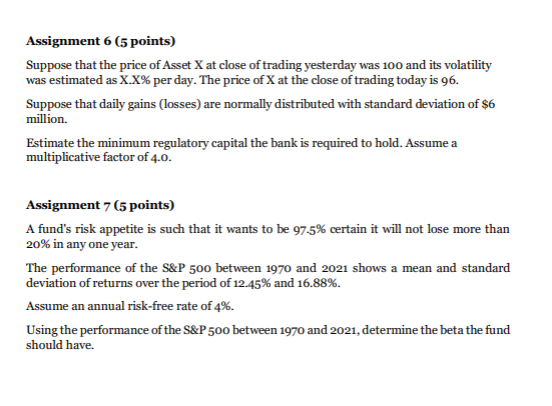

Assignment 6 ( 5 points ) Suppose that the price of Asset X at close of trading yesterday was 1 0 0 and its volatility

Assignment points

Suppose that the price of Asset X at close of trading yesterday was and its volatility

was estimated as XX per day. The price of X at the close of trading today is

Suppose that daily gains losses are normally distributed with standard deviation of $

million.

Estimate the minimum regulatory capital the bank is required to hold. Assume a

multiplicative factor of

Assignment points

A fund's risk appetite is such that it wants to be certain it will not lose more than

in any one year.

The performance of the S&P between and shows a mean and standard

deviation of returns over the period of and

Assume an annual riskfree rate of

Using the performance of the S&P between and determine the beta the fund

should have.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Finance For Real Estate Development

Authors: Charles Long

1st Edition

0874204305, 978-0874204308