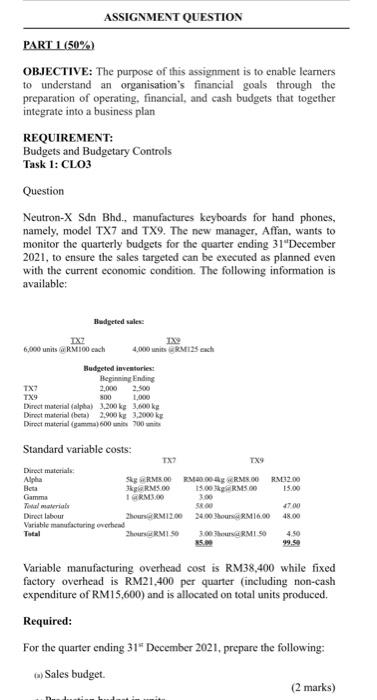

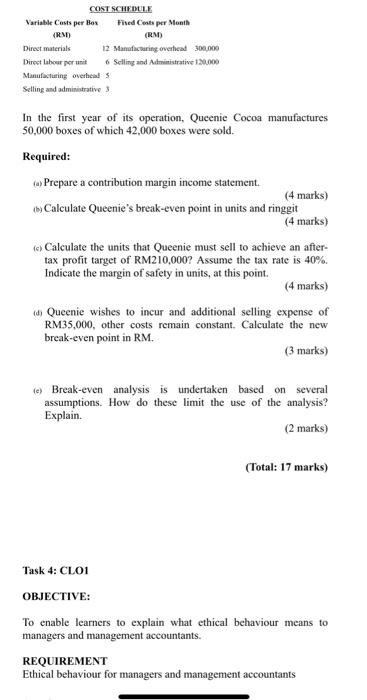

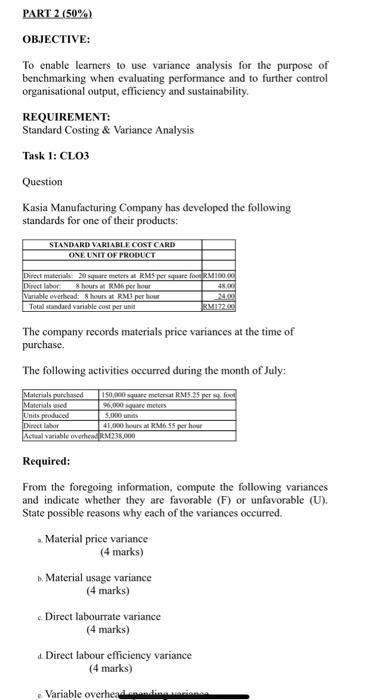

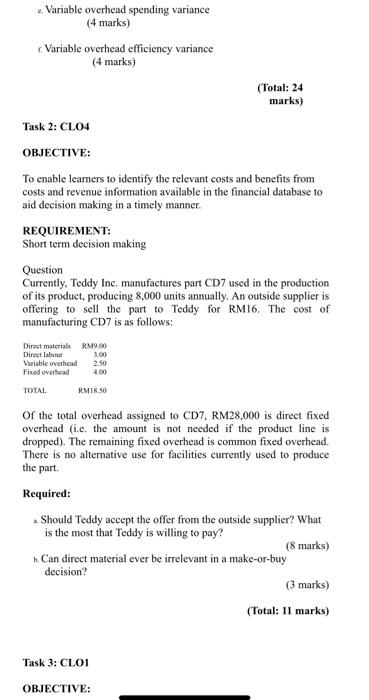

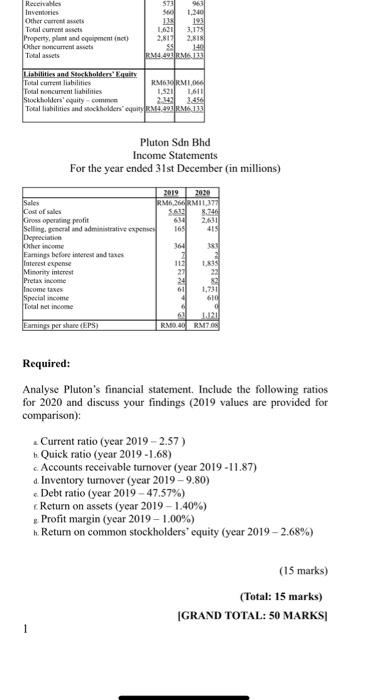

ASSIGNMENT QUESTION PART 1 (50%) OBJECTIVE: The purpose of this assignment is to enable learners to understand an organisation's financial goals through the preparation of operating, financial, and cash budgets that together integrate into a business plan REQUIREMENT: Budgets and Budgetary Controls Task 1: CLO3 Question Neutron-X Sdn Bhd. manufactures keyboards for hand phones, namely, model TX7 and TX9. The new manager, Affan, wants to monitor the quarterly budgets for the quarter ending 31"December 2021, to ensure the sales targeted can be executed as planned even with the current economic condition. The following information is available: Hudgeted sales TX IX 6,000 units RM100 each 4.000 units ERMIS cach Budgeted investeriet Beginning Ending TX 2,000 TX9 800,000 Direct material (alpha) 3.200 kg 300 kg Direct material (beta) 2.900 kg 3.2000 kg Direct material (gamma) 600 units 700 ni IN Standard variable costs: TX9 Direct materials Alpha SERMO RM20.00 RMS 00 RM32.00 Besa 3kg RMS 00 13.00 RM500 15.00 Gamma 1 RM3.00 Tovallole 4700 Direct labour Variable manufacturing the Zhours RM12.00 24.00 hours RM16,00 48.00 Total Thours RM150 3.00 RMIS 450 99.5 Variable manufacturing overhead cost is RM38.400 while fixed factory overhead is RM21,400 per quarter (including non-cash expenditure of RM15,600) and is allocated on total units produced. Required: For the quarter ending 31" December 2021, prepare the following: Sales budget (2 marks) (2 marks) cs, Production budget in units. (5 marks) teDirect materials usage and purchase budget Alpha, Beta, Gama (12 marks) (Direct labor budget. (2 marks) Task 2: CLO3 Financial information pertaining to Neutron-X Sdn Bhd above follows: - Beginning cash balance is RM180,000 Sales are on credit and are collected 50 percent in the current period and the remainder in the next period. Last quarter's sales were RM840,000. There are no bad debts. Purchases of direct materials and labor costs are paid for in the quarter acquired Manufacturing overhead expenses are paid in the quarter incurred. Selling and administrative expenses are all fixed and are paid in the quarter incurred. They are budgeted at RM34,000 per quarter, including RM9,000 of depreciation Required: Refer to the sales budget prepared in Task 1. Construct a cash budget for Neutron-X Sdn Bhd for the quarter ending 31" December 2021. (7 marks) (Total: 28 marks) OBJECTIVE: To enable learners to utilise the Cost Volume Profit analysis in making informed decisions and cost effective actions related to the products or services the business sells. REQUIREMENT: Cost Volume profit analysis Task 3 (CLO2) Question Queenie Cocoa manufactures nutritious cocoa powder packaged for local market. The product is sold in boxes at RM40 per unit. The cost incurred to manufacture and market the product follows: COST SCHEDULE Variable Costs per les COST SCHEDULE Variable Costs per Box Fired Cesta per Month (RMD (RM) Direct materials 12 Manufacturing overhead 300,000 Direct labour per unit Selling and Administrative 120.000 Manufacturing overheads Selling and administrative In the first year of its operation, Queenie Cocoa manufactures 50,000 boxes of which 42,000 boxes were sold. Required: (wPrepare a contribution margin income statement (4 marks) Calculate Queenie's break-even point in units and ringgit (4 marks) to Calculate the units that Queenie must sell to achieve an after- tax profit target of RM210,000? Assume the tax rate is 40%. Indicate the margin of safety in units, at this point (4 marks) Queenie wishes to incur and additional selling expense of RM35,000, other costs remain constant. Calculate the new break-even point in RM (3 marks) le) Break-even analysis is undertaken based on several assumptions. How do these limit the use of the analysis? Explain. (2 marks) (Total: 17 marks) Task 4: CLOI OBJECTIVE: To enable learners to explain what ethical behaviour means to managers and management accountants. REQUIREMENT Ethical behaviour for managers and management accountants Task 4: CLOI OBJECTIVE: To enable learners to explain what ethical behaviour means to managers and management accountants. REQUIREMENT Ethical behaviour for managers and management accountants Question Asri, the purchasing agent for Kota Manufacturing Division, was considering the possibility of purchasing a component from a new supplier. The price is RM0.70 which is below the standard price of RM0.90. The favourable price variance would help Asri to produce an impressive performance report and good enough to qualify him for annual bonus. More importantly, a good performance this year would secure him a position at the headquarters with significant salary increase However, there was doubt on his part knowing the background of the supplier. Reports were basically negative, indicating that the supplier was known to make two to three deliveries on time but unreliable there on. There was only questions regarding the quality of the parts delivered, with life of the components being 25 percent less than what normal sources would provide If the component was purchased, no problems would surface for several months. Asri would already be at the headquarters. Considering the minimum personal risk, Asri continues with the decision to purchase from the new supplier. Required: Do you think that the use of standards and practice of holding individual accountable for their achievement played major roles in Asri's decision? Was he being ethical? (Total: 5 marks) GRAND TOTAL: 50 MARKS PART 2 (50%) OBJECTIVE: To enable learners to use variance analysis for the purpose of benchmarking when evaluating performance and to further control organisational output, efficiency and sustainability REQUIREMENT: Standard Cortina PART 2 (50%) OBJECTIVE: To enable learners to use variance analysis for the purpose of benchmarking when evaluating performance and to further control organisational output, efficiency and sustainability. REQUIREMENT: Standard Costing & Variance Analysis Task 1: CLO3 Question Kasia Manufacturing Company has developed the following standards for one of their products: STANDARD VARIABLE COST CARD ONE UNIT OF PRODUCT Direct materiak 20 square meters RMS per square foc RM100,00 Direct labor hours at RM6 per bour 48.00 Variable overbead: Shours at RM per hour Total standard rible cost per unit M1722 The company records materials price variances at the time of purchase The following activities occurred during the month of July: Materials purchased 150,000 square metent RM5.35 per sq. for Materials used 96.000 meters Units produced Direct labor 41,000 hours at RMSS hour Actual variable overhead M238.000 5.000 Required: From the foregoing information, compute the following variances and indicate whether they are favorable (F) or unfavorable (U). State possible reasons why each of the variances occurred. - Material price variance (4 marks) b. Material usage variance (4 marks)