Answered step by step

Verified Expert Solution

Question

1 Approved Answer

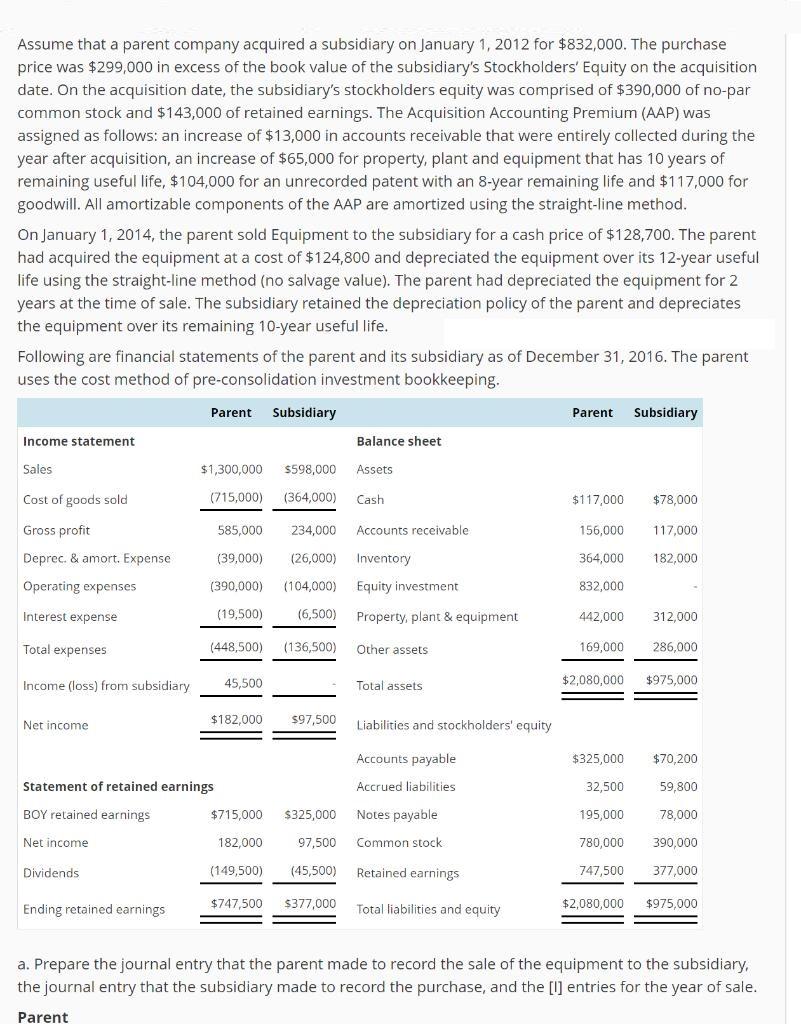

Assume that a parent company acquired a subsidiary on January 1, 2012 for $832,000. The purchase price was $299,000 in excess of the book

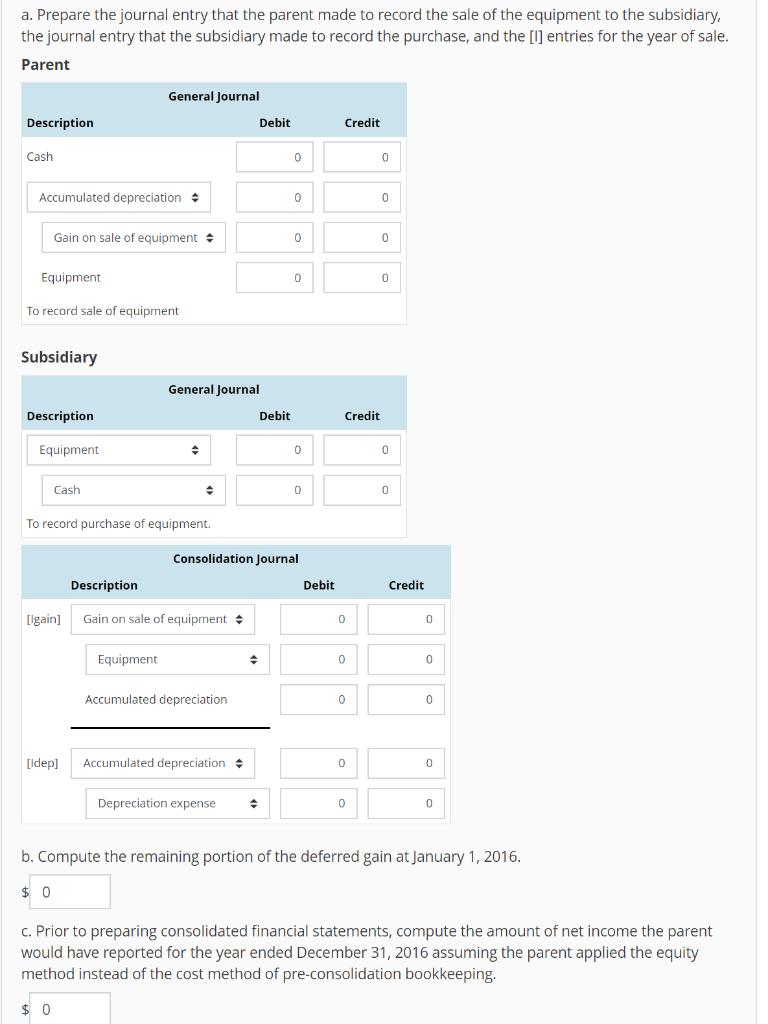

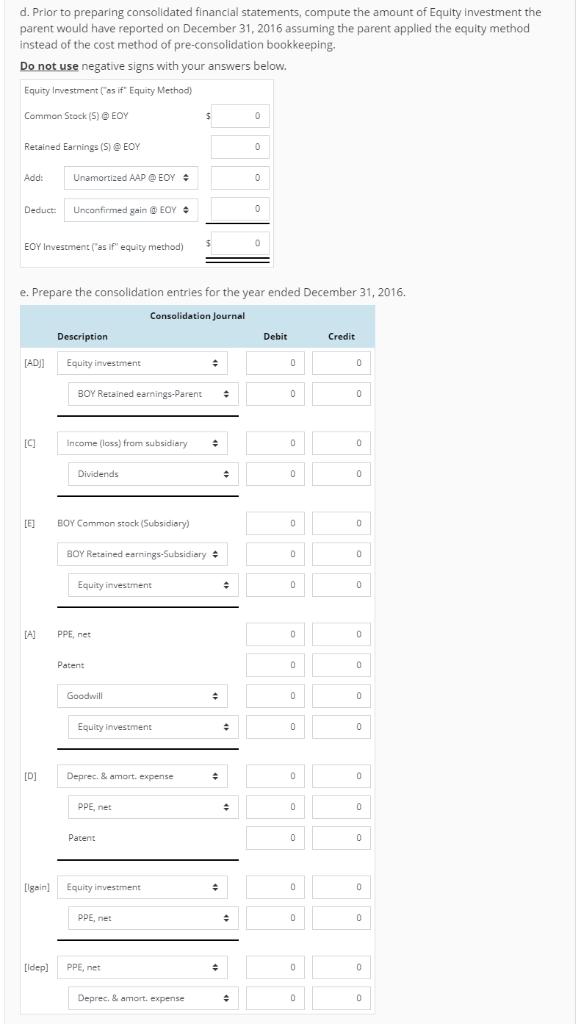

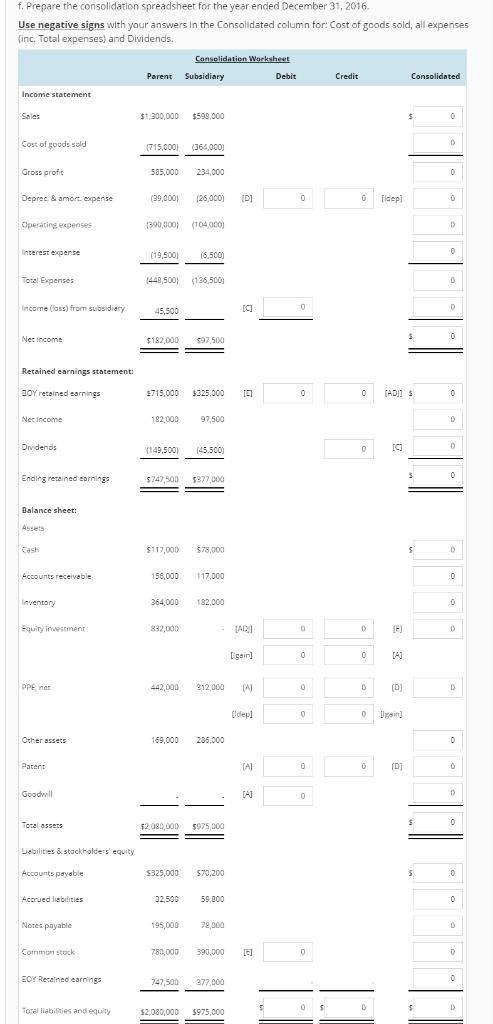

Assume that a parent company acquired a subsidiary on January 1, 2012 for $832,000. The purchase price was $299,000 in excess of the book value of the subsidiary's Stockholders' Equity on the acquisition date. On the acquisition date, the subsidiary's stockholders equity was comprised of $390,000 of no-par common stock and $143,000 of retained earnings. The Acquisition Accounting Premium (AAP) was assigned as follows: an increase of $13,000 in accounts receivable that were entirely collected during the year after acquisition, an increase of $65,000 for property, plant and equipment that has 10 years of remaining useful life, $104,000 for an unrecorded patent with an 8-year remaining life and $117,000 for goodwill. All amortizable components of the AAP are amortized using the straight-line method. On January 1, 2014, the parent sold Equipment to the subsidiary for a cash price of $128,700. The parent had acquired the equipment at a cost of $124,800 and depreciated the equipment over its 12-year useful life using the straight-line method (no salvage value). The parent had depreciated the equipment for 2 years at the time of sale. The subsidiary retained the depreciation policy of the parent and depreciates the equipment over its remaining 10-year useful life. Following are financial statements of the parent and its subsidiary as of December 31, 2016. The parent uses the cost method of pre-consolidation investment bookkeeping. Parent Subsidiary Parent Subsidiary Income statement Balance sheet Sales $1,300,000 $598,000 Assets Cost of goods sold (715,000) (364,000) Cash $117,000 $78,000 Gross profit 585,000 234,000 Accounts receivable 156,000 117,000 Deprec. & amort. Expense (39,000) (26,000) Inventory 364,000 182,000 Operating expenses (390,000) (104,000) Equity investment 832,000 Interest expense (19,500) (6,500) Property, plant & equipment 442,000 312,000 Total expenses (448,500) (136,500) Other assets 169,000 286,000 Income (loss) from subsidiary 45,500 Total assets $2,080,000 $975,000 $182,000 $97,500 Liabilities and stockholders' equity Net income Accounts payable $325,000 $70,200 Statement of retained earnings Accrued liabilities 32,500 59,800 BOY retained earnings $715,000 $325,000 Notes payable 195,000 78,000 Net income 182,000 97,500 Common stock 780,000 390,000 Dividends (149,500) (45,500) Retained earnings 747,500 377,000 Ending retained earnings $747,500 $377,000 Total liabilities and equity $2,080,000 $975,000 a. Prepare the journal entry that the parent made to record the sale of the equipment to the subsidiary, the journal entry that the subsidiary made to record the purchase, and the [1] entries for the year of sale. Parent a. Prepare the journal entry that the parent made to record the sale of the equipment to the subsidiary. the journal entry that the subsidiary made to record the purchase, and the [I] entries for the year of sale. Parent General Journal Description Debit Credit Cash Accumulated depreciation + Gain on sale of equipment Equipment To record sale of equipment Subsidiary General Journal Description Debit Credit Equipment Cash To record purchase of equipment. Consolidation Journal Description Debit Credit [igain] Gain on sale of equipment Equipment Accumulated depreciation [Idep] Accumulated depreciation + Depreciation expense b. Compute the remaining portion of the deferred gain at January 1, 2016. $ 0 c. Prior to preparing consolidated financial statements, compute the amount of net income the parent would have reported for the year ended December 31, 2016 assuming the parent applied the equity method instead of the cost method of pre-consolidation bookkeeping. $ 0 d. Prior to preparing consolidated financial statements, compute the amount of Equity investment the parent would have reported on December 31, 2016 assuming the parent applied the equity method instead of the cost method of pre-consolidation bookkeeping. Do not use negative signs with your answers below. Equity Investment Cas if" Equity Methad) Common Stock (5) EOY Retained Earnings (S) e EOY Add: Unamortized AAP @ EOY : Deduct: Unconfirmed gain EOY EOY Investment ("as if" equity method) e. Prepare the consolidation entries for the year ended December 31, 2016. Consolidation Journal Description Debit Credit [ADJ] Equity investment BOY Retained earnings-Parent income (loss) from subsidiary Dividends [E] BOY Common stock (Subsidiary) BOY Retained earnings-Subsidiary Equity investment [A] PPE, net Patent Goodwill Equity investment [D] Deprec. & amort. expense PPE, net Patent llgain] Equity investment PPE, net [idep) PPE, net Deprec. & amort. expense f. Prepare the consolidation spreadsheet for the year ended December 31, 2016. Use negative signs with your answers in the Consolidated column for: Cost of goods sold, all expenses (inc. Total expenses) and Dividends. Conselidation Warksheet Perent Subsidiary Debit Credit Consolidated Income statement Sales $1.300.000 $599,000 Cost of goods sold (715,000) (364,000) Gross profit 585,000 234.000 Deprec. & amort. expense (39,000) (26,000) (D] fldep) Operating expenses (390,000) (104,000) Interest expense (19,500) (6,500) Total Expenses (448,500) (136,500) Income (loss) from subsidiery 45,500 Ne: income $182,000 S97,500 Retained earnings statement: DOY retained earnings $715.000 $325,000 (ADII S Net income 182,000 97,500 Drvidends (149,500) (45,500) Ending retained earnings $747,500 $377,000 Balance sheet: Assets Cash S117,000 S78,000 Accounts receiveble 156,000 117,000 Inventory 364,000 182,000 Equity investment 832,000 - LAC) (F) Iigair) PPE, met 442,000 312,000 (A) (D) [ldep] Dgsin) Other assetS 169,000 205,000 Patent TAI (D] Goodwll Total assets $2,080,000 5975,000 Liebilities & stackholders' equity Accounts payeble $325,000 S70,200 Accrued liabilities 32,500 59,000 Notes payable 195,000 78,000 Common stock 780.000 390,000 EOY Recained earnings 747,500 277,000 Total liabilities and equity $2,080,000 $975,000

Step by Step Solution

★★★★★

3.55 Rating (162 Votes )

There are 3 Steps involved in it

Step: 1

Part A parent debit credit cash 128700 Accumulated 20800 dep...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Intermediate Accounting Reporting and Analysis

Authors: James M. Wahlen, Jefferson P. Jones, Donald Pagach

3rd edition

9781337909402, 978-1337788281