Answered step by step

Verified Expert Solution

Question

1 Approved Answer

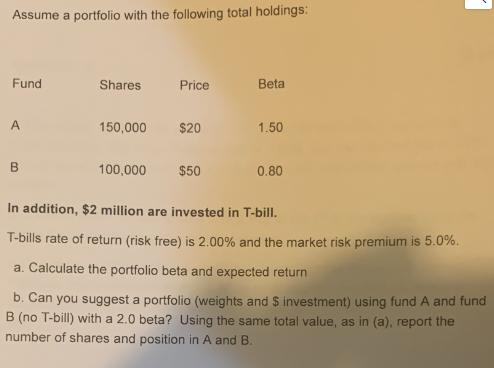

Assume a portfolio with the following total holdings: Fund A B Shares 150,000 100,000 Price $20 $50 Beta 1.50 0.80 In addition, $2 million

Assume a portfolio with the following total holdings: Fund A B Shares 150,000 100,000 Price $20 $50 Beta 1.50 0.80 In addition, $2 million are invested in T-bill. T-bills rate of return (risk free) is 2.00% and the market risk premium is 5.0%. a. Calculate the portfolio beta and expected return b. Can you suggest a portfolio (weights and $ investment) using fund A and fund B (no T-bill) with a 2.0 beta? Using the same total value, as in (a), report the number of shares and position in A and B.

Step by Step Solution

★★★★★

3.44 Rating (154 Votes )

There are 3 Steps involved in it

Step: 1

To calculate the portfolio beta and expected return we need to use the following formulas Portfolio Beta p wA A wB B Expected Return Expected Return R...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

International Financial Reporting and Analysis

Authors: David Alexander, Anne Britton, Ann Jorissen

5th edition

978-1408032282, 1408032287, 978-1408075012