Question

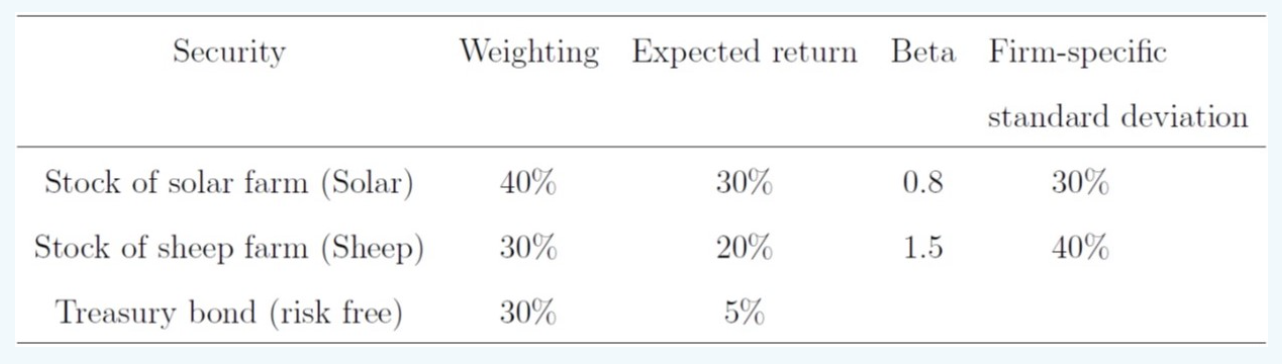

Assume an active fund has decided to exploit the great potential in the solar panel industries. The fund invested in the following three securities with

Assume an active fund has decided to exploit the great potential in the solar panel industries. The fund invested in the following three securities with given weightings

The standard deviation of the stock market index is 20%. Please compute the expected return and standard deviation of this active fund's portfolio.

Security Stock of solar farm (Solar) Stock of sheep farm (Sheep) Treasury bond (risk free) Weighting Expected return 40% 30% 30% 20% 30% 5% Beta Firm-specific 0.8 1.5 standard deviation 30% 40%Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Infrastructure Planning And Finance

Authors: Vicki Elmer, Adam Leigland

1st Edition

0415693187, 978-0415693189