Question

Assume an asset's price changes follow a log-normal diffusion process with initial price S0 = 100, mean drift rate = 0.075, volatility = 0.25, risk

-

Assume an asset's price changes follow a log-normal diffusion process with initial price S0 = 100, mean drift rate = 0.075, volatility = 0.25, risk free rate r = 0.03, and dT = 1.5 i.e. 18 months. A European call option is purchased on day 0 with a strike price of K = $110. Do not use simulations to answer the following questions. You can use R programming language for calculations if needed. (please do all parts listed in picture below, thank you :))

-

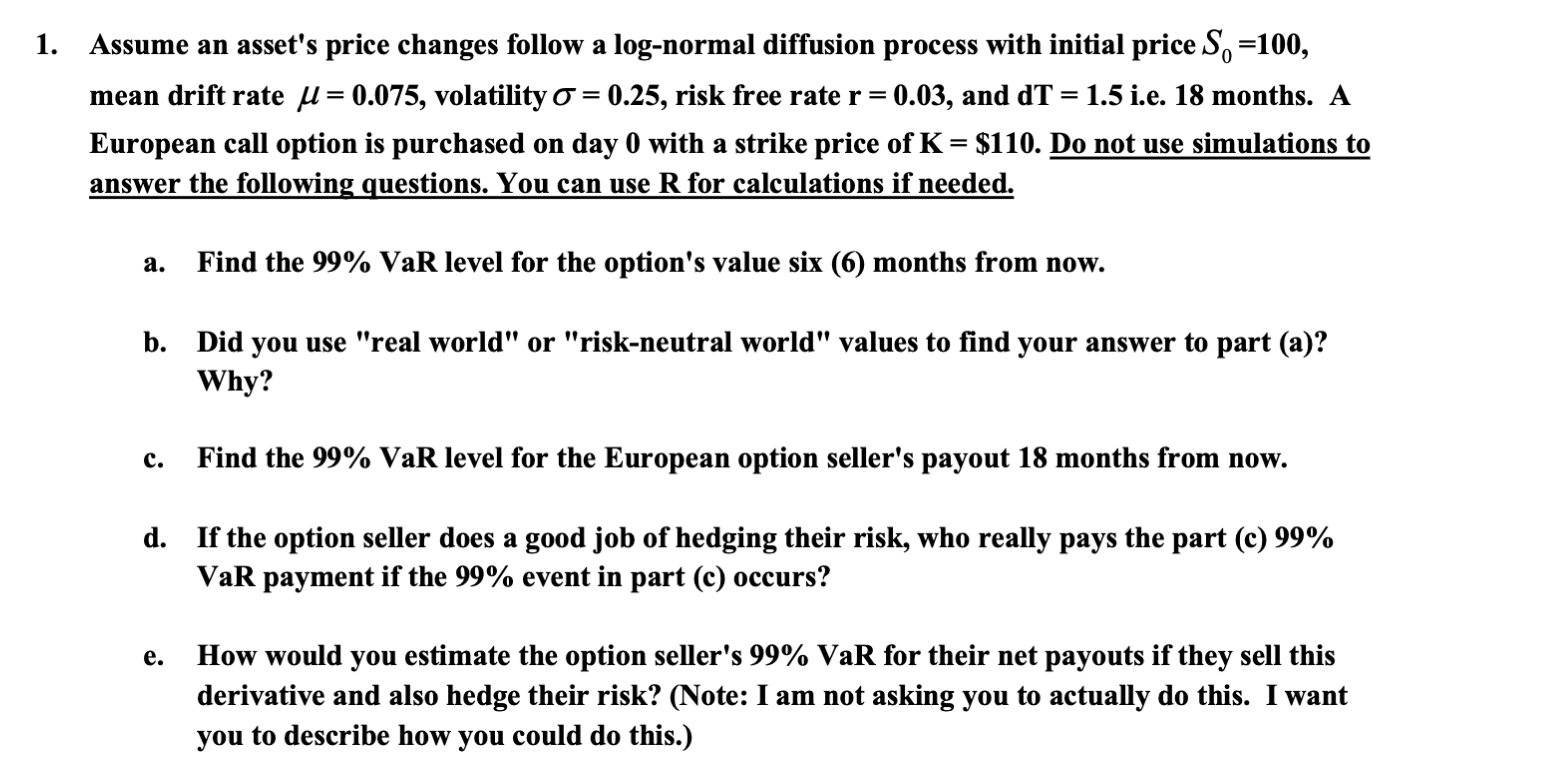

1. Assume an asset's price changes follow a log-normal diffusion process with initial price So =100, mean drift rate u = 0.075, volatility O = 0.25, risk free rate r=0.03, and dT = 1.5 i.e. 18 months. A European call option is purchased on day 0 with a strike price of K = $110. Do not use simulations to answer the following questions. You can use R for calculations if needed. a. Find the 99% VaR level for the option's value six (6) months from now. b. Did you use "real world" or "risk-neutral world" values to find your answer to part (a)? Why? c. Find the 99% VaR level for the European option seller's payout 18 months from now. d. If the option seller does a good job of hedging their risk, who really pays the part (c) 99% VaR payment if the 99% event in part (c) occurs? e. How would you estimate the option seller's 99% VaR for their net payouts if they sell this derivative and also hedge their risk? (Note: I am not asking you to actually do this. I want you to describe how you could do this.) 1. Assume an asset's price changes follow a log-normal diffusion process with initial price So =100, mean drift rate u = 0.075, volatility O = 0.25, risk free rate r=0.03, and dT = 1.5 i.e. 18 months. A European call option is purchased on day 0 with a strike price of K = $110. Do not use simulations to answer the following questions. You can use R for calculations if needed. a. Find the 99% VaR level for the option's value six (6) months from now. b. Did you use "real world" or "risk-neutral world" values to find your answer to part (a)? Why? c. Find the 99% VaR level for the European option seller's payout 18 months from now. d. If the option seller does a good job of hedging their risk, who really pays the part (c) 99% VaR payment if the 99% event in part (c) occurs? e. How would you estimate the option seller's 99% VaR for their net payouts if they sell this derivative and also hedge their risk? (Note: I am not asking you to actually do this. I want you to describe how you could do this.)

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Islamic FinanceA Practical Perspective

Authors: Nafis Alam, Lokesh Gupta, Bala Shanmugam

1st Edition

3319665588, 9783319665580