Answered step by step

Verified Expert Solution

Question

1 Approved Answer

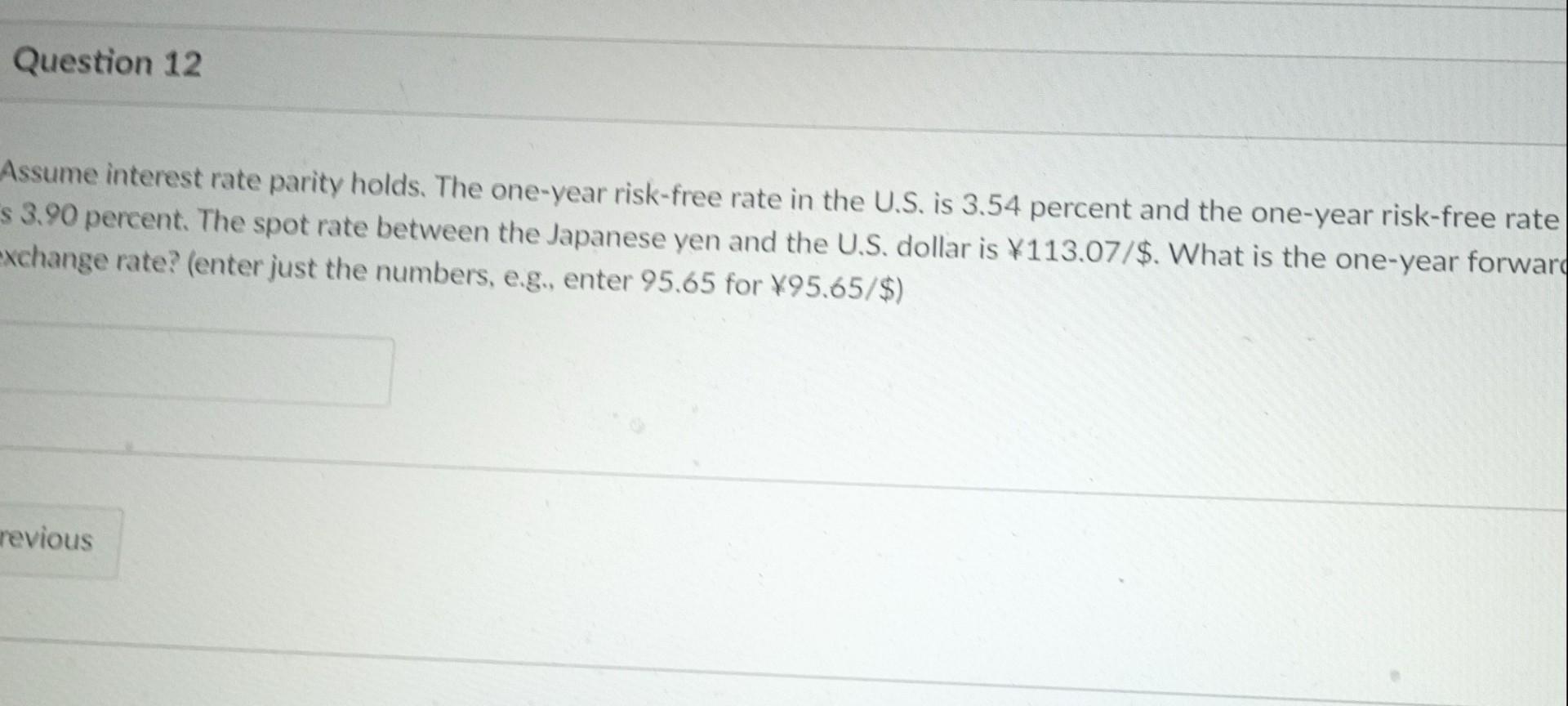

Assume interest rate parity holds. The one-year risk-free rate in the U.S. is 3.54 percent and the one-year risk-free rate s 3.90 percent. The spot

Assume interest rate parity holds. The one-year risk-free rate in the U.S. is 3.54 percent and the one-year risk-free rate s 3.90 percent. The spot rate between the Japanese yen and the U.S. dollar is 113.07/$. What is the one-year forwar xchange rate? (enter just the numbers, e.g., enter 95.65 for 95.65/$ )

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Auditor 1 A Person Who Conducts An Audit. 2 Someone Who Arrives After The Battle And Bayonets The Wounded.

Authors: Day By J.

1st Edition

B09NHD98BP, 979-8781611843