Question

Assume that of your $40,000 portfolio, you invest $15,000 in asset A and $25,000 in asset B. (a) Write down the probability distribution of your

Assume that of your $40,000 portfolio, you invest $15,000 in asset A and $25,000 in asset B.

(a) Write down the probability distribution of your future portfolio value.

(b) Find the correlation between the return on the two assets.

(c) Find

(i) the expected rate of return of your portfolio, and

(ii) the volatility of your portfolio.

(d) (i) Determine the minimum variance portfolio consisting of asset A and asset B. Explain

how you can construct a $40,000 portfolio with the two assets.

(ii) Compare the minimum variance portfolio with your portfolio in terms of expected

rate of return and volatility.

(e) Suppose now you want to construct a $40,000 portfolio with dierent targets. Determine

all the possibilities of constructing such a portfolio (with exact amounts stated for the two

assets) that you can achieve the following targets:

(i) The expected return (in dollar term) is $4,800.

(ii) The portfolio variance is 0.0175.

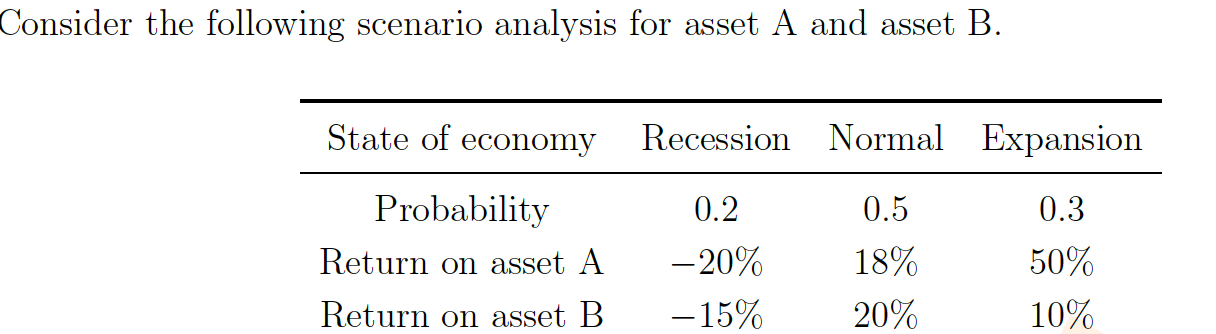

Consider the following scenario analysis for asset A and asset B. State of economy Recession Normal Expansion Probability Return on asset A Return on asset B 0.2 -20% -15% 0.5 18% 20% 0.3 50% 10% Consider the following scenario analysis for asset A and asset B. State of economy Recession Normal Expansion Probability Return on asset A Return on asset B 0.2 -20% -15% 0.5 18% 20% 0.3 50% 10%Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Guide To Finance Theory And Application Portfolio Mathematics

Authors: Professional Risk Managers' International Association (PRMIA)

1st Edition

0071731814