Answered step by step

Verified Expert Solution

Question

1 Approved Answer

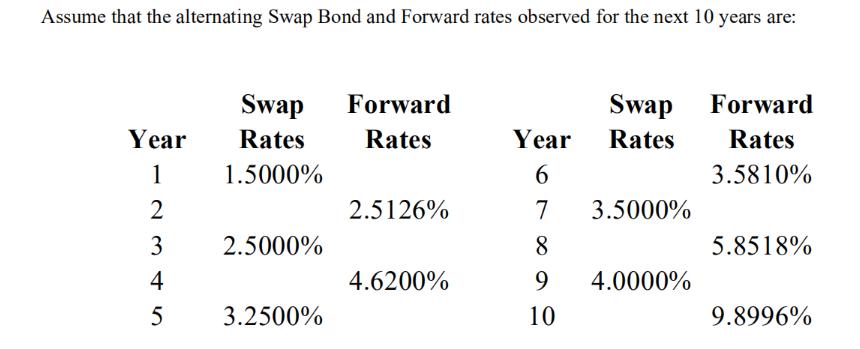

Assume that the alternating Swap Bond and Forward rates observed for the next 10 years are: Year 1 2345 2 4 Swap Rates 1.5000%

Assume that the alternating Swap Bond and Forward rates observed for the next 10 years are: Year 1 2345 2 4 Swap Rates 1.5000% 2.5000% 3.2500% Forward Rates 2.5126% 4.6200% Swap Forward Rates 3.5810% Year Rates 6 7 8 9 10 3.5000% 4.0000% 5.8518% 9.8996% Compute the fixed rate on a $100 million two year forward starting swap that matures in 10 years?

Step by Step Solution

★★★★★

3.32 Rating (143 Votes )

There are 3 Steps involved in it

Step: 1

To calculate the fixed rate on a 100 million twoyear forwardstarting swap that matures in 10 years we can use the concept of the present value of cash ...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Reporting Financial Statement Analysis And Valuation A Strategic Perspective

Authors: James M Wahlen, Stephen P Baginskl, Mark T Bradshaw

7th Edition

9780324789423, 324789416, 978-0324789416